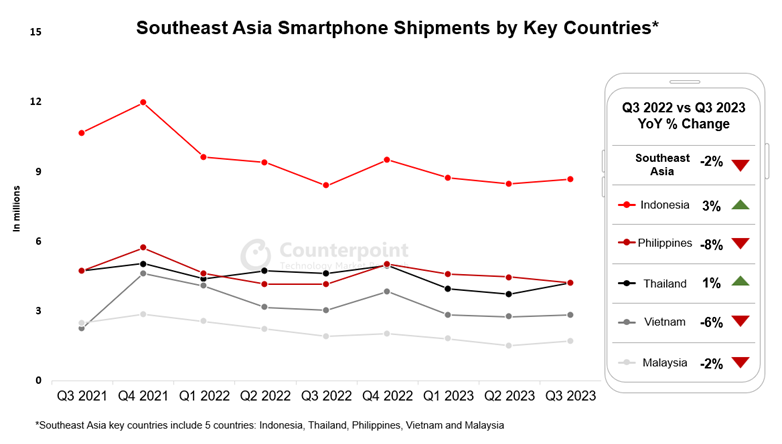

- Southeast Asia’s smartphone shipment volumes declined 2% YoY but increased 3% QoQ in Q3 2023, signaling a recovery in the region’s smartphone demand.

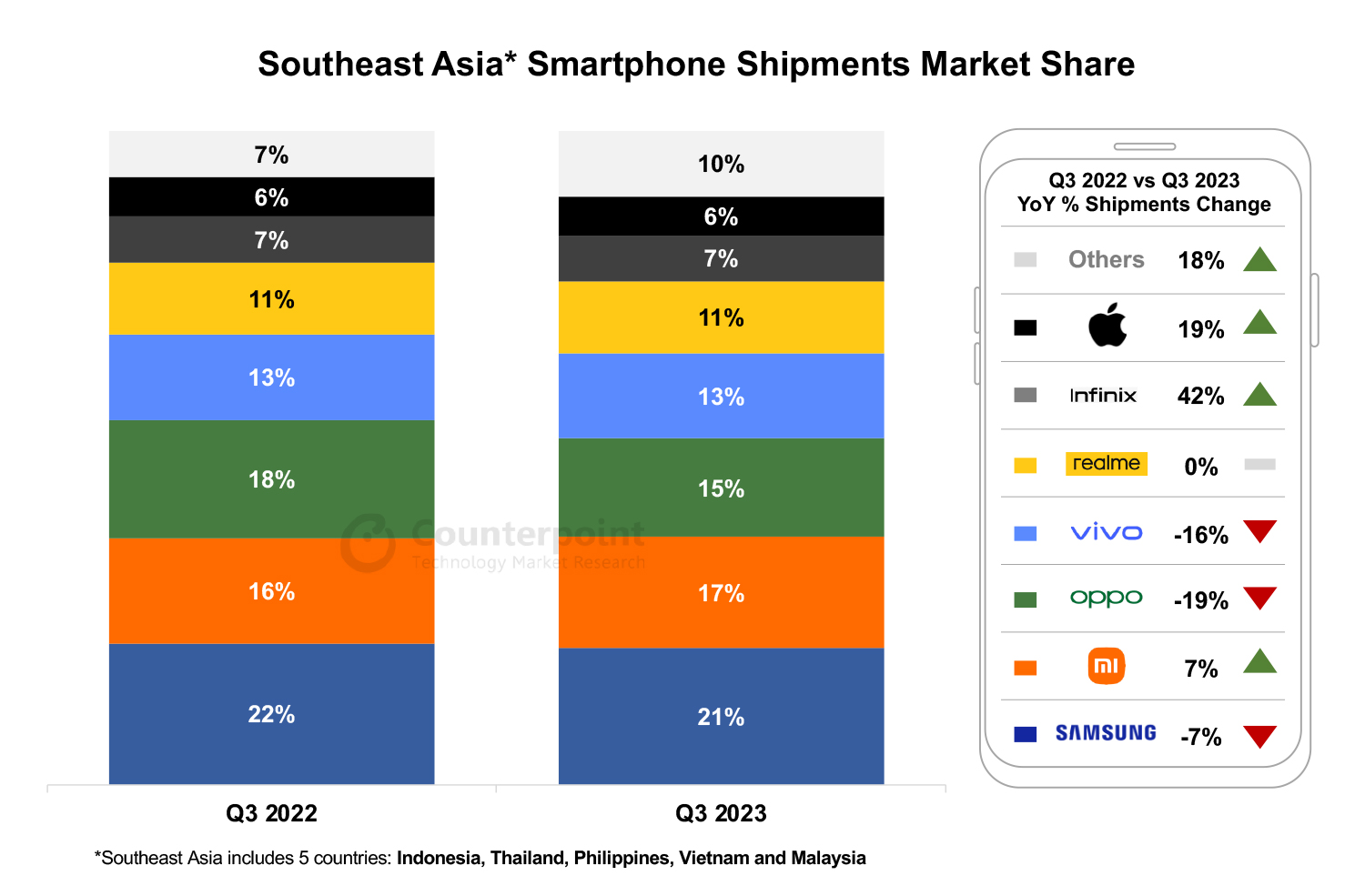

- The fastest-growing brands were TECNO (148%), Infinix (42%) and Apple (19%). All three Transsion brands collectively grew by 62% YoY in Q3 2023.

- Samsung led the market with a 21% share, followed by Xiaomi (17%) and OPPO (15%).

- Indonesia and Thailand saw flattish growth while other SEA countries like the Philippines, Malaysia and Vietnam declined YoY.

- 5G smartphones captured 36% of overall shipments in the region.

Jakarta, Hong Kong, London, Boston, Toronto, New Delhi, Beijing, Taipei, Seoul – November 9, 2023

Southeast Asia’s smartphone shipments declined 2% YoY but increased 3% QoQ in Q3 2023, signaling a recovery in the region’s smartphone demand, according to Counterpoint Research’s Southeast Asia Monthly Smartphone Channel Share Tracker. Stronger macroeconomic indicators, aggressive new OEM launches and aggressive promotions by OEMs and other platforms were the main growth contributors. Also, an uptick was seen in the replacement cycles of consumers opting for low-to-mid-tier smartphones. TECNO, Infinix and Apple emerged as the fastest-growing brands during the quarter.

Most key SEA countries like Indonesia, Malaysia, Philippines and Vietnam showed a double-digit decline in Q2 2023, but they improved in Q3 2023, hinting a relief for OEMs ahead of an important festive quarter. However, on an annual level, we foresee a YoY decline of about 8% for the region in 2023.

SEA remains an important market for the tech ecosystem due to its underpenetration in many areas, like online banking, e-wallet usage, online shopping and overall internet usage.

Key country insights

- Indonesia and Thailand saw flattish growth in smartphone shipments while other key SEA countries like the Philippines, Malaysia and Vietnam declined YoY.

- In Thailand, the new government launched several initiatives, such as delaying debt payments, lowering energy prices and offering cash handouts, to ease the citizen’s cost of living. This brought immediate effect on commodities. Besides, in September, the government announced visa-free entry for tourists from China and Kazakhstan, bringing much relief to the country’s COVID-hit tourism industry.

- In Indonesia, OEMs launched several new models in the middle and end of September. The new launches made up a big share of the overall shipments. During the quarter, Indonesians preferred to wait and watch when it came to spending money. The country is gearing up for its legislative and presidential election in February 2024. We expect Q4 2023 to see more smartphone sales due to aggressive offers.

- Vietnam’s economy has picked up with its exports coming back on track. GDP grew 5.33% in Q3 2023, beating expectations. Foreign investment is expected to rise with Vietnam entering strategic partnerships during the prime minister’s visit to the US in September.

- In the Philippines, the economy is showing signs of recovery. Consumer confidence has improved. Unemployment is a concern and essentials are still expensive for low-income families. Due to easing inflation, the coming months might see increased household spending. Overall, the household expenditure levels might take some time to recuperate, which might affect smartphone purchases.

- In Malaysia, industrial manufacturing is still slowing down due to weaker demand for electrical and electronic products. Weaker exports have added to the decline in GDP as well. Malaysia’s 5G connectivity and penetration are improving now but the overall industry is being affected by China’s economic headwinds.

Key OEM insights

- Beating the trend, Apple’s shipments increased by 19% YoY during the quarter. Apple is still seeing a strong demand for the iPhone 13 and 14 series, adding to the demand for the newly launched 15 series.

- Samsung led the market with a 21% share. Its A05 series has entered the market, adding to a strong overall A-series presence. Premium models like the Z Flip 5 and Z Fold 5 along with the S series are contributing as well. Promotions for the brand are centered around these premium models not only in countries like Thailand and Vietnam but also increasingly in countries like Indonesia and the Philippines. This is due to premium smartphone purchases by well-to-do consumers who are least affected by current headwinds. Samsung was the top brand in Indonesia, Thailand and Vietnam in Q3 2023.

- Xiaomi’s shipments grew 7%. Its Redmi 12 series has been doing quite well across all key SEA countries. Its promotions and new model launches were also better than most other brands during Q3 2023, which helped the brand increase shipments. Xiaomi was the top brand in Malaysia in Q3.

- Transsion witnessed the highest growth during the quarter. Infinix grew 42% YoY, TECNO 148% and itel witnessed a 17% growth. Infinix and TECNO are offering strong base specifications along with a varied model portfolio.

- realme saw flat growth during Q3 2023. It was the top brand in the Philippines.

Commenting on brand dynamics in Q3 2023, Senior Analyst Glen Cardoza said, “Samsung and Xiaomi have been able to market their models in a much better manner across all key SEA countries, while sustaining new launches across price ranges, compared to the limited options from brands like OPPO and vivo. Upcoming brands are making a mark as well. Among them, the Transsion brands lead. TECNO and Infinix have either sustained or increased their new model launches, all in the entry to mid-tier segments. The three Transsion brands collectively grew 62% YoY in Q3 2023.”

While 5G penetration still has some way to go in countries like Indonesia, Vietnam and Malaysia, 5G is increasingly becoming a key consideration for consumers. Many consumers want their phones to be 5G ready. During Q3 2023, 5G smartphones captured 36% of overall shipments in the region.

The region’s key macroeconomic parameters like China-ASEAN trade, startup funding and foreign direct investment continue to see YoY declines. Add to this a recovering tourism industry. This has led to low GDP levels across most SEA countries. Price-conscious consumers have waited all year for the situation to get better, spending the least on discretionary items. On the positive side, digital transformation continues even as the industry recuperates slowly. This means that we can expect a better Q4 of 2023.

* Key Southeast Asia countries/markets include Indonesia, Thailand, Philippines, Vietnam and Malaysia.

Feel free to contact us at press@counterpointresearch.com for questions regarding our latest research and insights.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

![]()