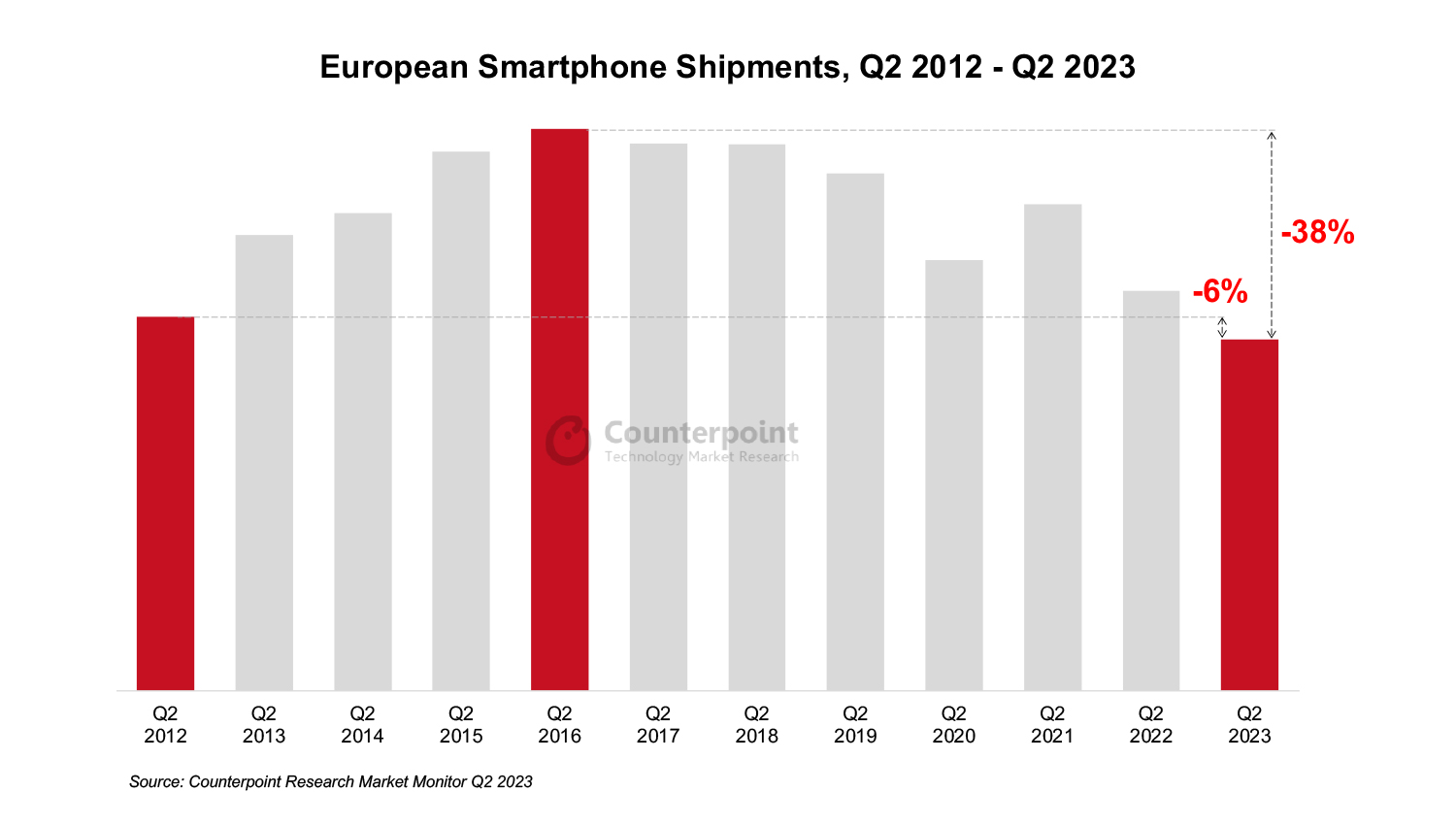

- Europe smartphone shipments fell 12% YoY in Q2 2023 to reach lowest since 2012.

- Russia only major market to register growth at 4% YoY.

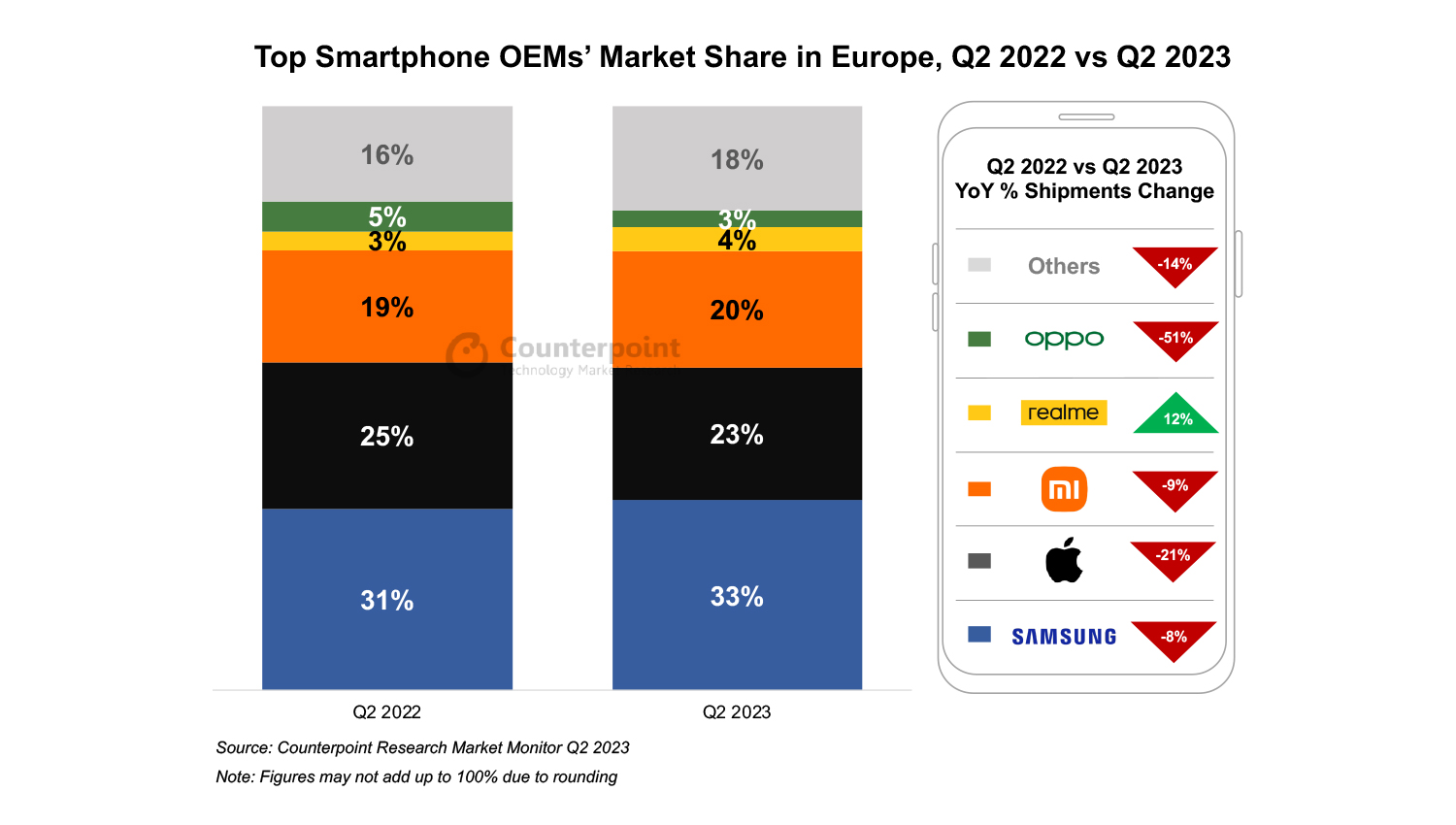

- OPPO’s shipments fell 51% YoY hurt by patent issues and difficult market conditions.

- 2023 smartphone shipments are set to be lower than in 2022.

London, Boston, Toronto, New Delhi, Jakarta, Beijing, Taipei, Seoul – September 1, 2023

European smartphone shipments declined 12% YoY in Q2 2023, marking the lowest quarterly shipment volume since Q1 2012, according to the latest report from Counterpoint Research’s Market Monitor Service.

Western Europe declined by 14% YoY during the quarter while Eastern Europe limited its fall to 8% YoY, despite being in an already battered state. All major European nations performed weakly in Q2 2023, except Russia, which conversely registered 4% YoY growth. However, this was primarily due to lower shipments in Q2 2022 – the first full quarter after Russia’s invasion of Ukraine and the resulting sanctions and market exits of prominent smartphone players.

OPPO had a difficult time in Q2 2023 with patent disputes and uncertainty in several countries, due to which the brand’s shipments dropped 51% YoY. The uncertainty is likely to persist which will result in further shipment declines in the coming quarters.

realme grew 12% YoY, driven primarily by Russia, which accounted for 55% of the brand’s shipments in the region. In Russia, realme benefitted from Samsung and Apple’s market exit, which allowed the company to fill the void left by these heavyweights. Additionally, realme has remained in the second position in Russia for five straight quarters and has been closing the gap with the market leader Xiaomi.

HONOR registered 9% YoY growth during the quarter due to the base effect and its ongoing expansion outside China.

Commenting on the current market dynamics, Research Analyst Harshit Rastogi said, “Despite falling shipment volumes, the higher price bands (wholesale prices exceeding $600) have been capturing a larger share of the market each year. They also have a longer replacement cycle compared to mid-segment and lower-price band smartphones, which further dampens demand. Consequently, OEMs are likely to focus on increasing their ASP and concentrate on services to drive revenue growth in the coming quarters.”

Commenting on market outlook, Associate Director Jan Stryjak commented, “The market is unlikely to make a full recovery `this year and 2023 smartphone shipments are set to be lower than in 2022, marking consecutive decade-low shipments in both 2022 and 2023. While the economic conditions are partly to blame, consumer buying behaviour is also changing, suggesting that a lower level of sales will set a new baseline. However, despite the low shipment volumes, upcoming iterations of Apple’s iPhone and Samsung’s foldables are likely to fare well, prompting a bump in sales volumes in the coming quarters.”

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media, and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.

Follow Counterpoint Research

press(at)counterpointresearch.com

![]()