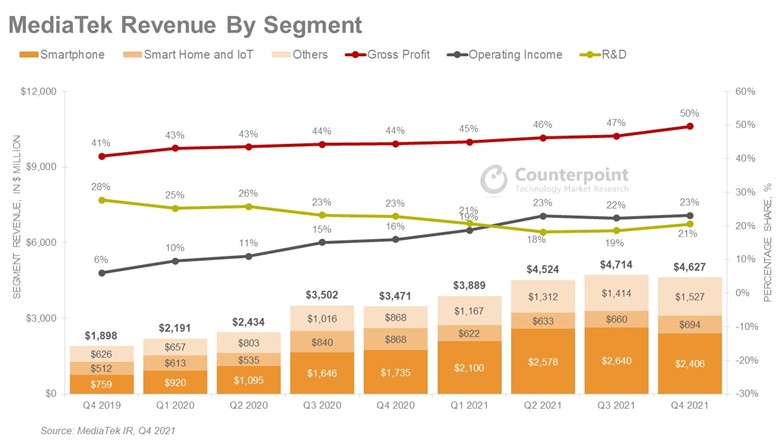

- 2021 saw record revenues of $17.6B, growing 53% annually (2020 $11.5B). and operating margin both increased for the fourth consecutive year, driven by investment in 5G, Wi-Fi 6 and low-power technology.

- 4Q 2021 revenues were down sequentially 2% and up 33.5% YoY. The sequential decline was due to a reduction in smartphones revenues (down 9% QoQ).

Exhibit 1: MediaTek Revenue, Sales to Gross Profit, R&D & Operating income

- Its smartphone chipset volumes declined this quarter due to the high shipments in the first half and inventory corrections from Chinese smartphone OEMs. Because of the supply chain constraints, many customers built chipset inventory to manage uncertainties in the supply situation. The chipset inventory increased again this quarter due to the market situation.

- Guidance for 1Q 2022, Revenue $4.7-$5.1B up 2-10% sequentially driven by flagship chipset (Dimensity 9000) for smartphones, and higher 5G penetration which will offset the lower seasonal demand. Also, the increase in the chipset pricing after TSMC’s hike in wafer price is reflected from Q4 2021 onwards.

- Growth Outlook: In 2022 revenue growth to exceed 20% with a gross margin target of 48% to 50%, owing to a better product mix and strong technology migration. 2022 is going to be another strong year as the foundry supply becomes more manageable. Mediatek already has the needed capacity with TSMC.

- It expects TAM to grow from $2.8B in 2021 to $5.1B in 2024. CAGR of mid-teen % for the next three years, with all revenue groups growing.

- Mobile to grow from $1B in 2021 to $1.8bn in 2024

- Smart Edge to grow from $1.4B in 2021 to $2.8B in 2024

- Power IC to grow from $0.3B in 2021 to $0.5B in 2024

- According to Counterpoint’s Smartphone Chipset Shipment forecast, we expect MediaTek to lead the smartphone chipset market with a 39% volume share in 1Q 2022 followed by Qualcomm with 29%.

- Mediatek has guided long term revenue growth, but most revenues will still be driven by smartphones. It will need to look for new growth areas either by investment or merger to remain competitive with Qualcomm, which is diversifying into Automotive, IoT, RF etc.

- MediaTek has secured major Dimensity 9000 design wins across multiple Chinese OEMs e.g., Oppo, Vivo, Xiaomi etc. The first model is scheduled to launch in March. We expect MediaTek’s flagship (3/4/5nm nodes) chipset to gain a 9%-10% market share in 2022.

- MediaTek’s 2022 blended chipset ASPs will be flat to slightly up due to the increasing mix of the 5G, flagship products. Further 4G chipset absolute revenues will be flat to a slight decline as the 5G chipset mix increases. According to Counterpoint’s Market Outlook service, 5G smartphone penetration is forecast to reach 54% of the total smartphone market, accounting for 800mn units.

- MediaTek has design wins in the Automotive segment, with infotainment applications. It also has the potential of adding 5G modems and IoT modules with companies such as Quectel, Fibocom, etc. Right now, these are not big revenue drivers, but a couple of years down the line will drive significant volumes.

- Notebooks/PC: With 5G modems, Wi-Fi 6/6E, Kompanio chipsets (for Chromebooks) it gained in the notebook segment in partnership with Intel and AMD.

- Another area for growth is Consumer Premises Equipment (CPE) for global operators using both 5G modem and Wi-Fi chipset in the applications like Fixed Wireless Access (FWA) etc.

- Extended Reality (XR) is a focus segment for MediaTek which will drive revenue. According to Counterpoint’s Extended Reality headset forecast, shipments are projected to grow about 10x from 11Mn units in 2021 to 105Mn in 2025.

- MediaTek is investing in the core technology to drive growth, like 5G modem with low latency, mmWave support, next-gen. Wi-Fi, 6G, security IP etc.