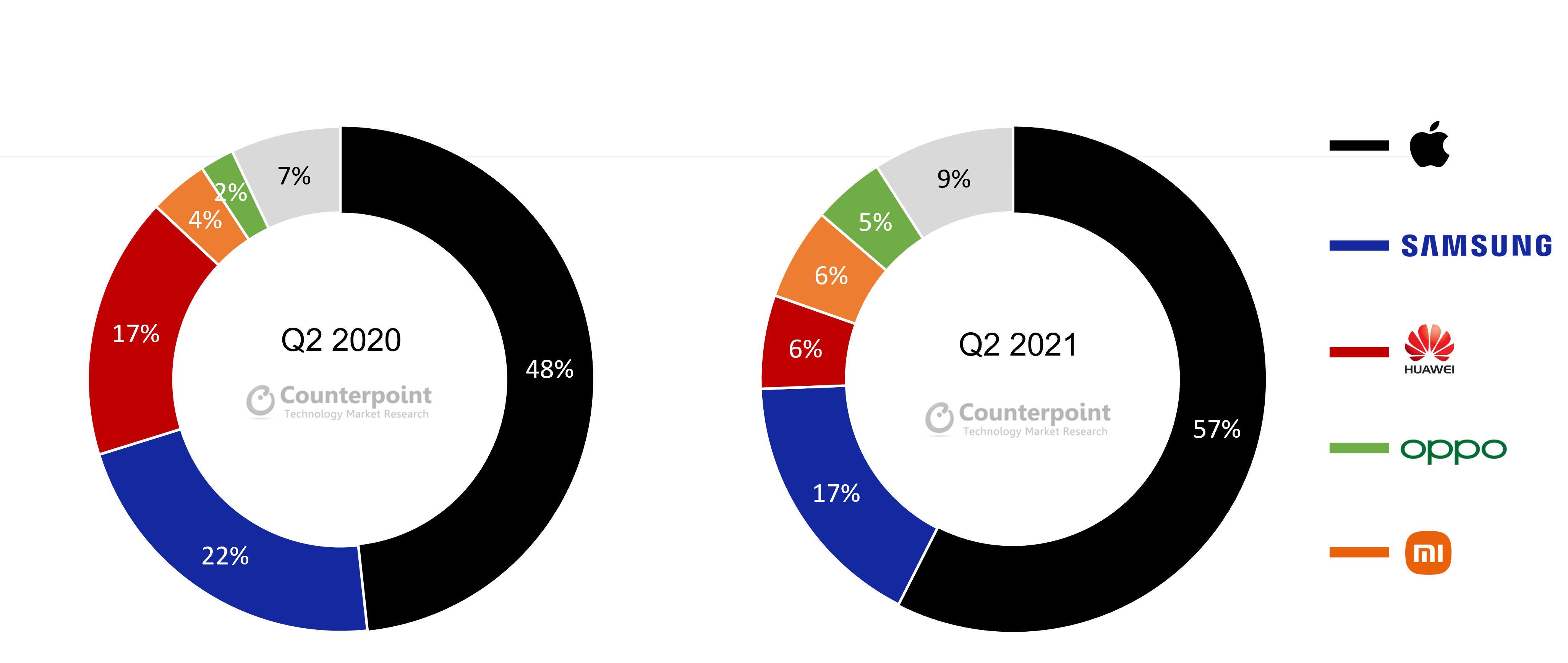

The global premium smartphone market (models priced $400* and above) recorded a 46% YoY sales growth in Q2 2021, according to Counterpoint Research’s Market Pulse Service. The growth in the premium segment outpaced the overall market growth of 26% YoY. Besides, the premium segment share in the global smartphone sales increased to 24% in Q2 2021, compared to 21% in Q2 2020. Apple continued to lead the segment, cornering over half of the sales during the quarter, followed by Samsung and Huawei. Since the launch of iPhone 12 series in Q4 2020, Apple has continued to account for over 50% share in the premium smartphone market.

Global Premium Smartphone (>$400) Sales Market Share, Q2 2020 vs Q2 2021

Source: Counterpoint Research Monthly Market Pulse

A large part of the premium market growth in Q2 2021 was driven by Apple, which reported a sales growth of 74% YoY in the premium segment on the strong momentum of the iPhone 12 series due to the iPhone users continuing to upgrade to 5G. Apple’s supply chain was also very resilient in managing component shortages and gained from the decline of Huawei in regions like China and Europe. Apple was the largest OEM in the premium segment across all regions.

Global Smartphone Premium Market Rankings, Q2 2021

Source: Counterpoint Research Monthly Market Pulse

Although Samsung’s sales in the premium segment grew 13% YoY, the brand lost its share in the segment due to production disruption at its Vietnam unit following a fresh COVID-19 outbreak. However, with the launch of the new Z fold 3 and Z flip 3 models at a lower price point compared to their predecessors, Samsung is likely to gain share in H2 2021.

Xiaomi and OPPO both gained share in the segment driven by their premium portfolio-focused expansion in regions like Europe and China. Xiaomi was among the Top 3 players in Europe in the premium segment driven by its Mi 11 series. The OEM has been making efforts to gain from Huawei’s decline, which is now paying off. OPPO also gained share driven by its Reno and Find series in China and Western Europe.

OnePlus entered the Top 3 list for the premium segment in North America driven by its OnePlus 9 Series. The OEM gained both from LG’s exit and Samsung’s supply constraints.

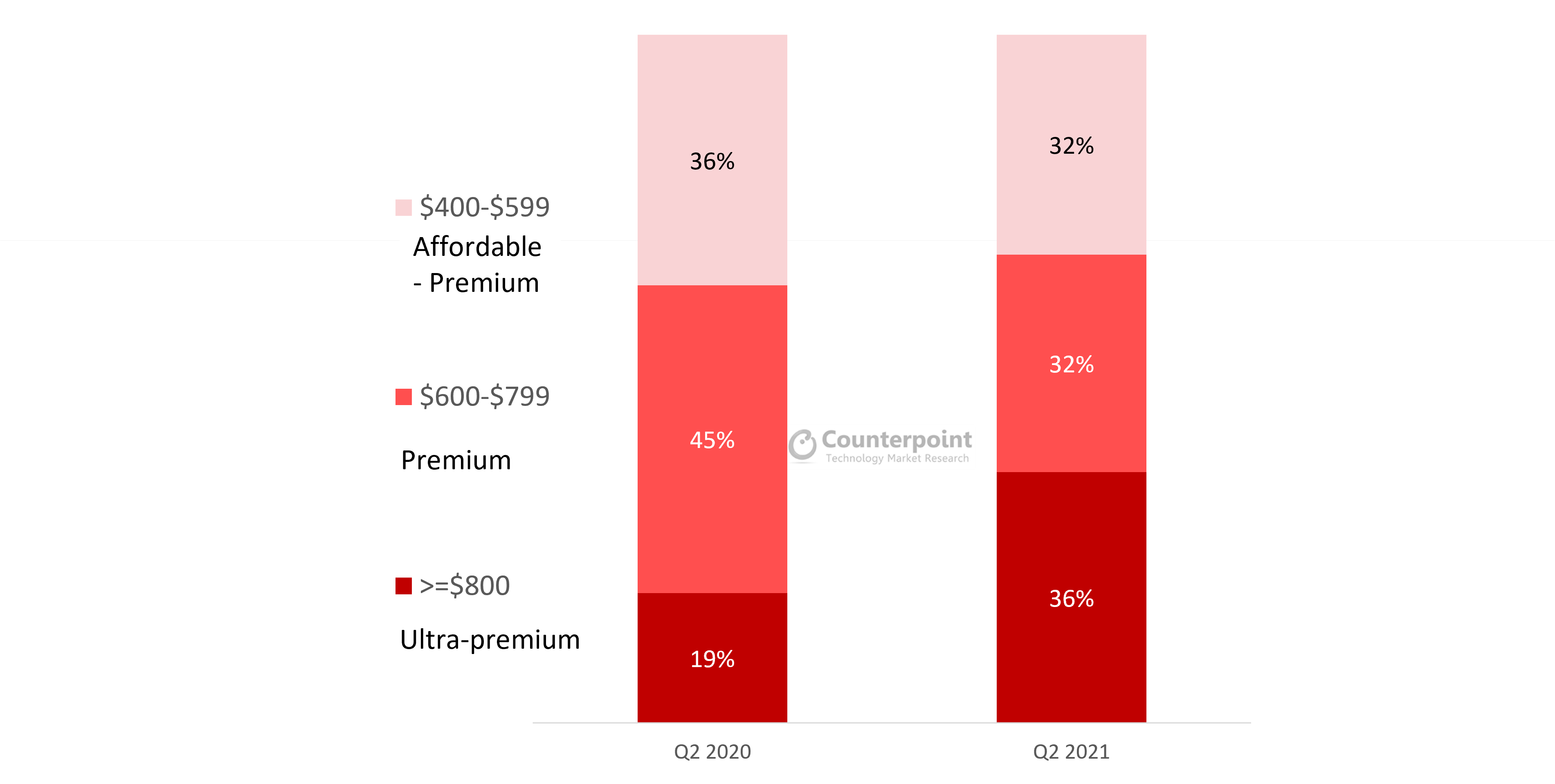

Within the premium segment, while all the price bands saw growth, the highest growth (182% YoY) was seen in the ultra-premium band (>$800). This was mainly due to the strong momentum of the iPhone 12 Pro Max and iPhone 12 Pro. The Pro versions were launched later than the usual September date, causing demand to spill over to the subsequent months. Apple captured close to 75% of the ultra-premium segment, compared to 54% a year ago. This shift also indicates that more consumers now prefer high-end devices after realizing the importance of smartphones to them during the COVID-19 lockdowns. A section of consumers also had extra savings while working from home, which they invested in devices like smartphones.

Sales Market Share by Price Band, Q2 2020 vs Q2 2021

Source: Counterpoint Research Monthly Market Pulse

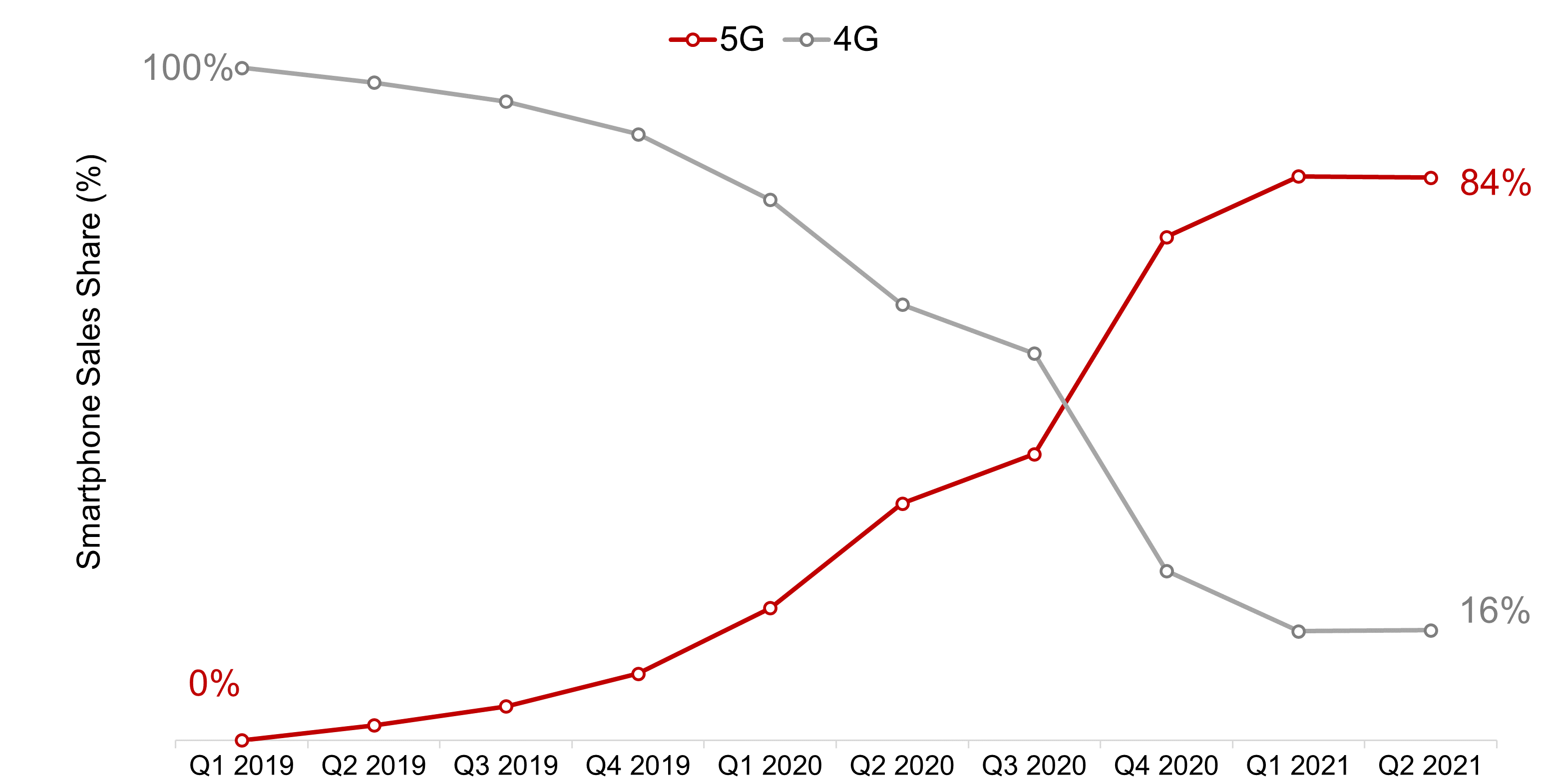

5G is also becoming a standard offering within the premium segment. The overall penetration of 5G within the premium segment reached 84% in Q2 2021, compared to 35% in Q2 2020. In the $600 and above price band, 95% of devices were 5G capable. The launch of the iPhone 12 series in Q4 2020 gave a boost to the sales of 5G capable devices in the segment.

4G, 5G Penetration in Premium Segment Smartphone Sales

Source: Counterpoint Research Monthly Market Pulse

Going forward, the premium segment is likely to continue its growth momentum. The sales of the iPhone 12 have been very stable in markets like the US even before the launch of the new iPhone series this month. Further, the launch of the Fold series from Samsung and the refresh of iPhones by Apple will also drive growth. With the replacement cycle for iPhone being closer to three years, there is also a significant potential of 5G upgrades in 2021 and beyond.

Xiaomi, OPPO, vivo and OnePlus will also continue to try to gain share in the premium segment. HONOR has also entered the segment in China with its Magic series. There is also the untapped segment of Huawei’s flagship users in China, which is a big opportunity. As the replacement cycle of these users approaches, other OEMs will gain share from Huawei.

*The analysis is based on wholesale ASP

You can also visit our Data Section (updated quarterly) to view the smartphone market share for World, USA, China and India.

Some of our other smartphone market analyses for Q2 2021