To receive weekly updates on the COVID-19 situation and our latest research straight to your inbox, click this link to register

Click here for the latest weekly updates on the impact and implication of COVID-19 situation on the Automotive industry.

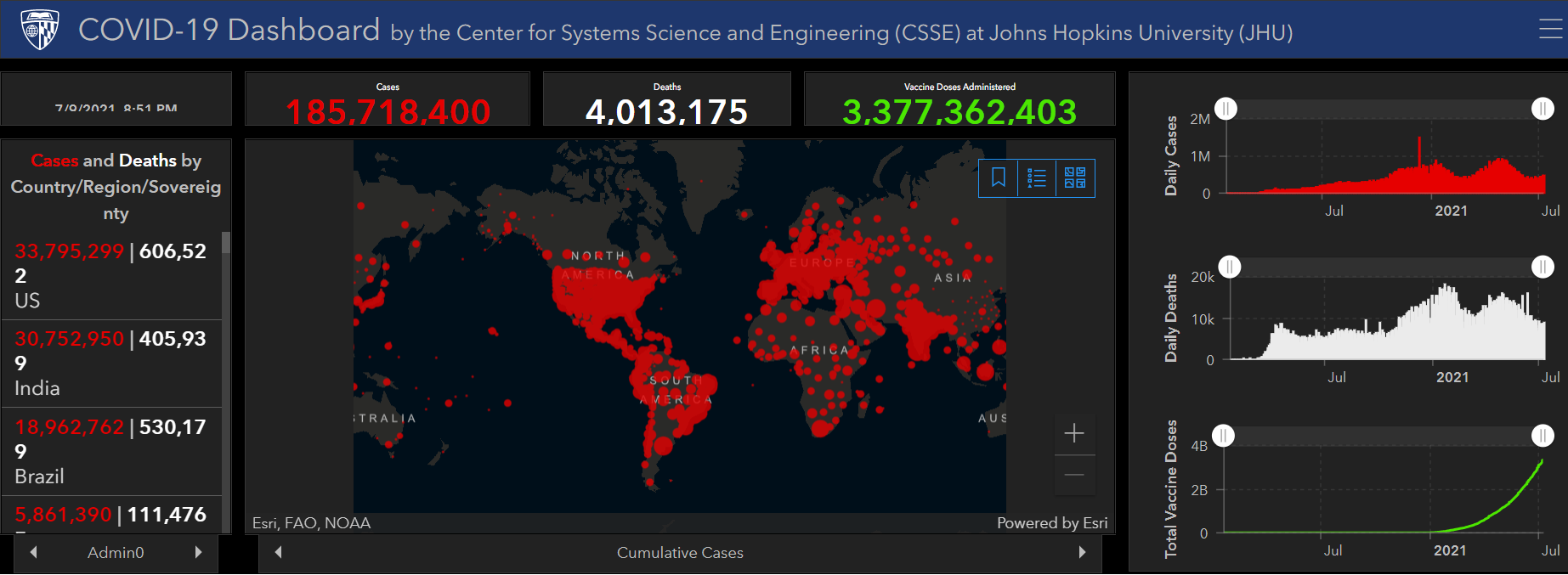

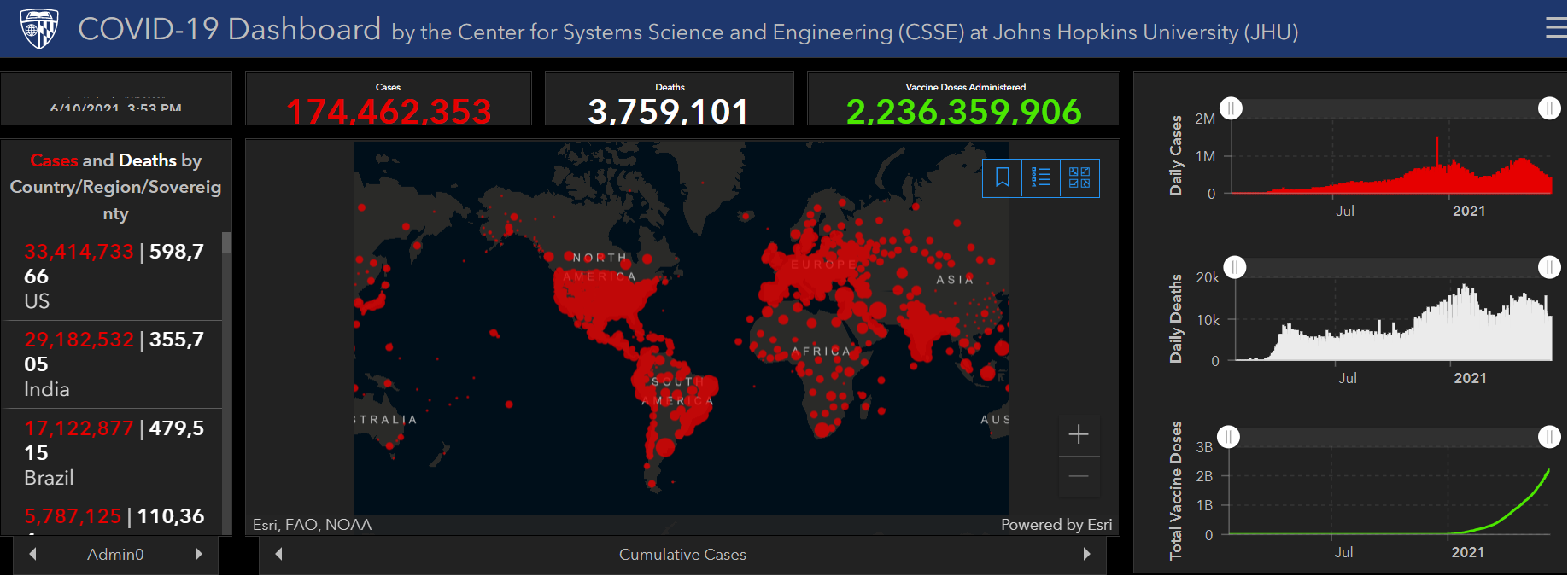

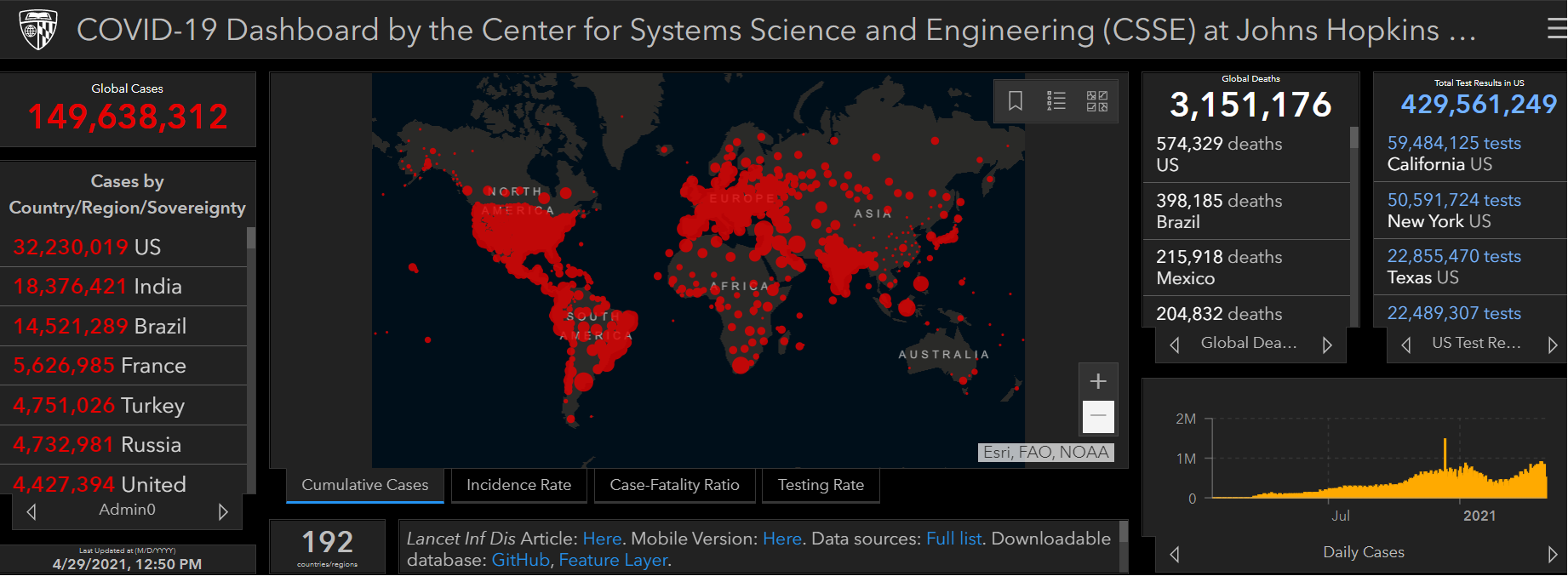

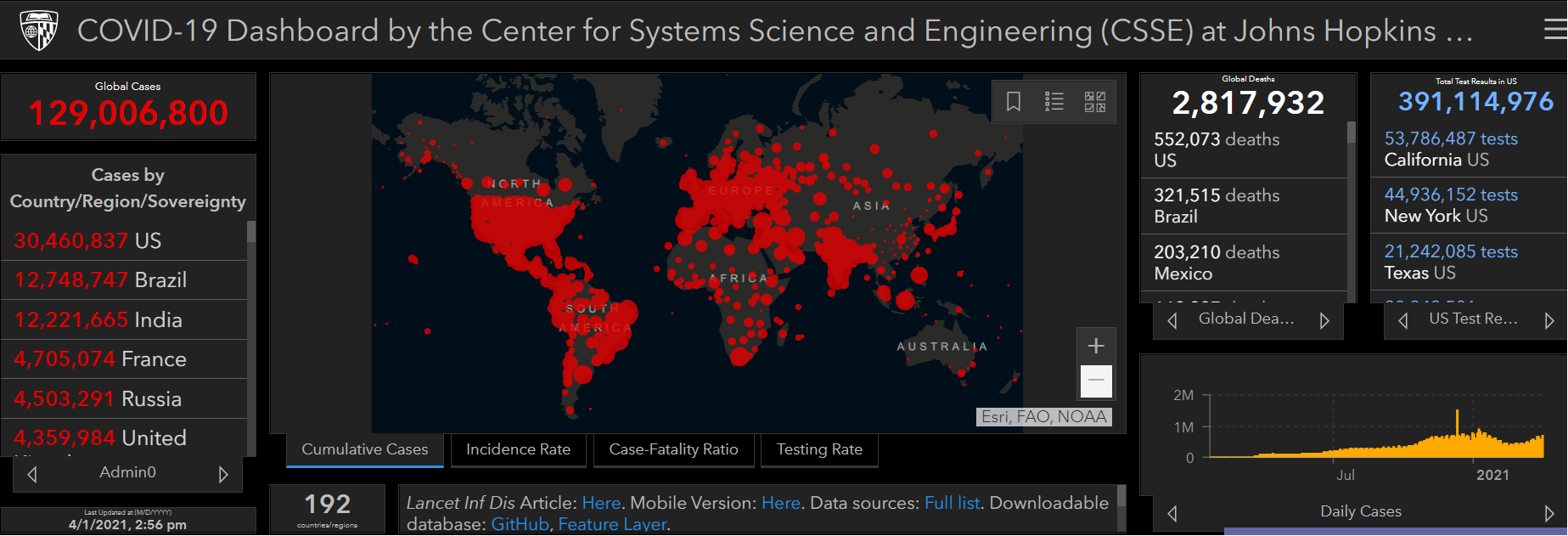

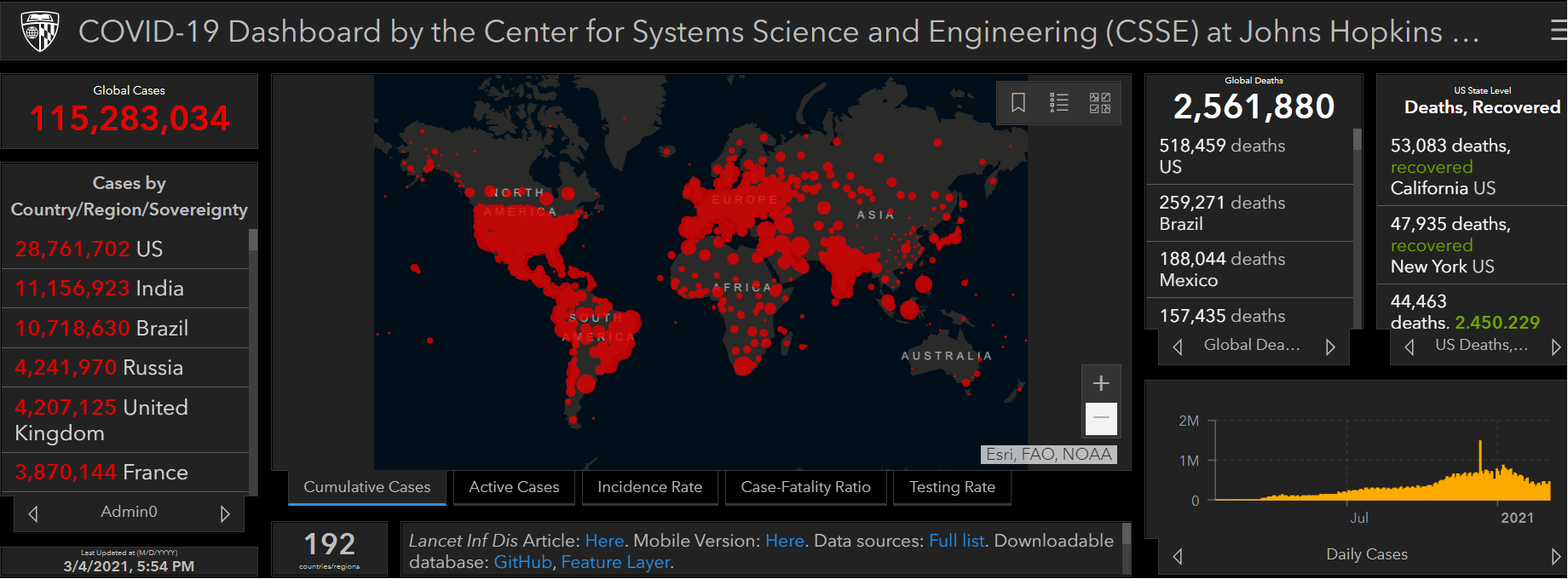

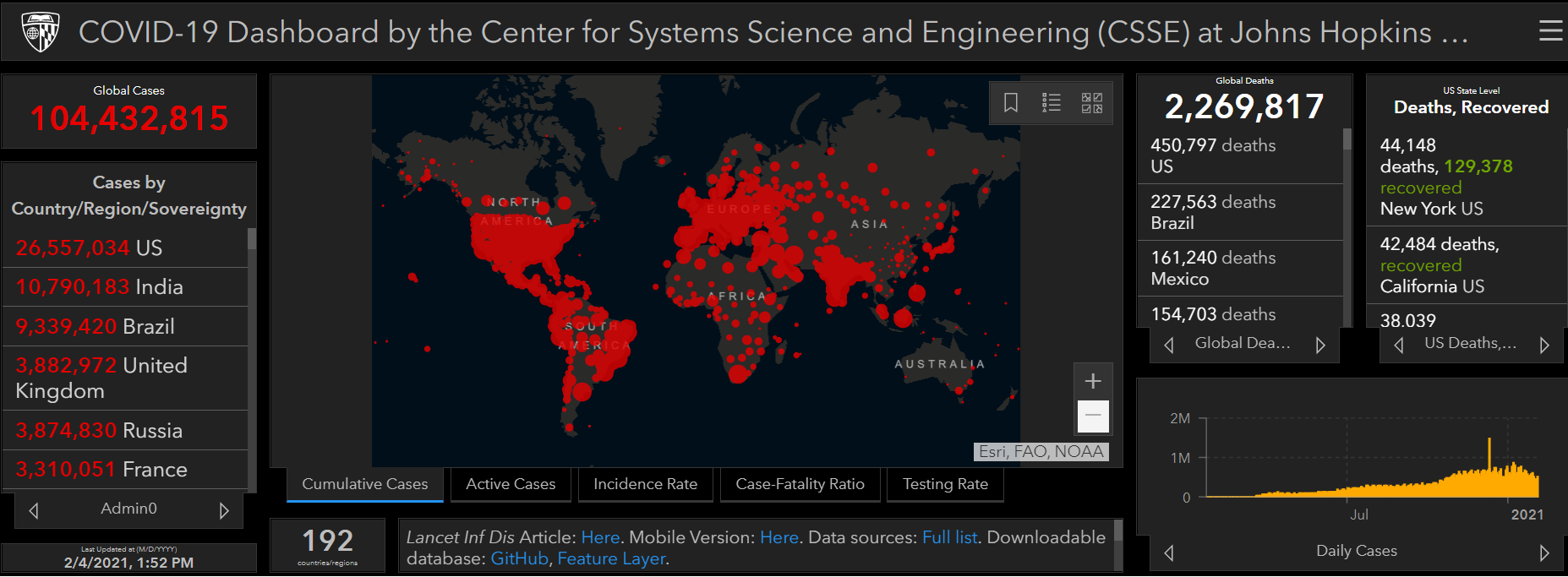

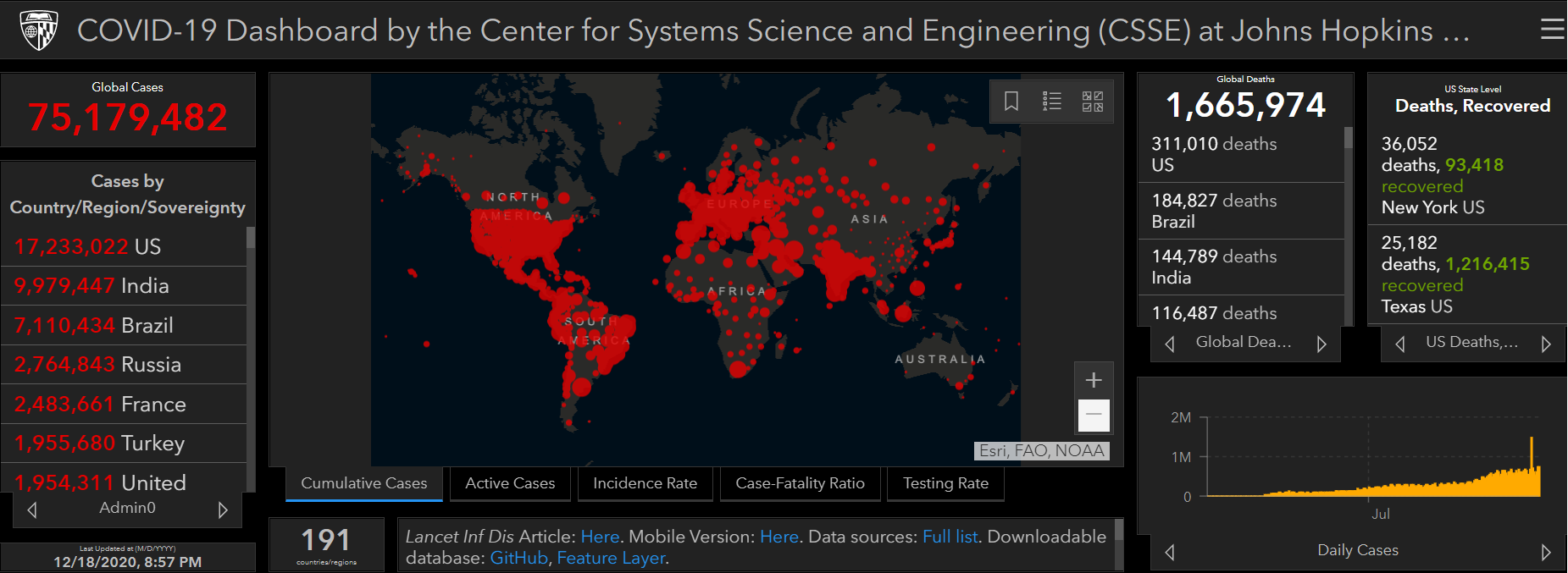

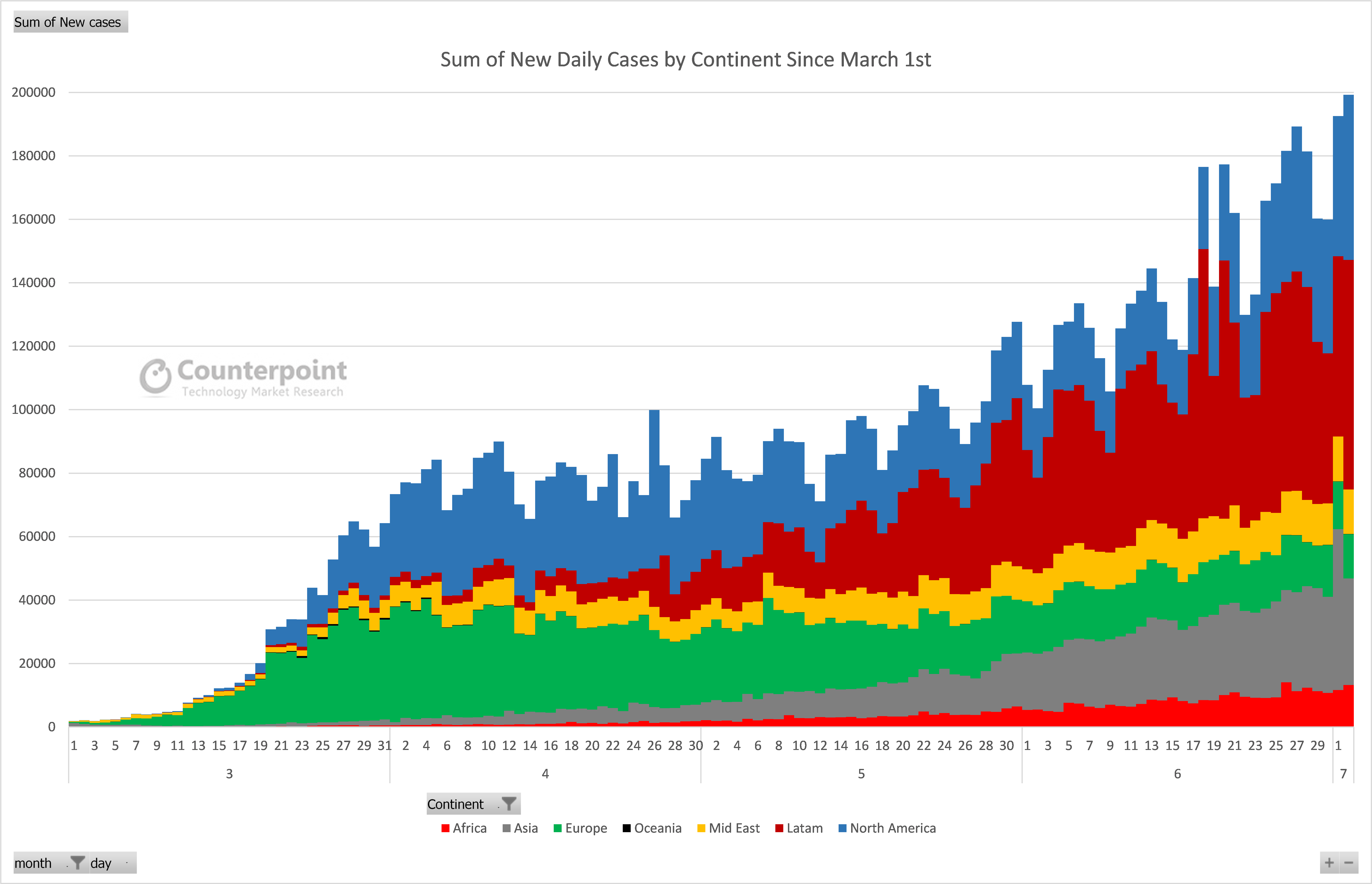

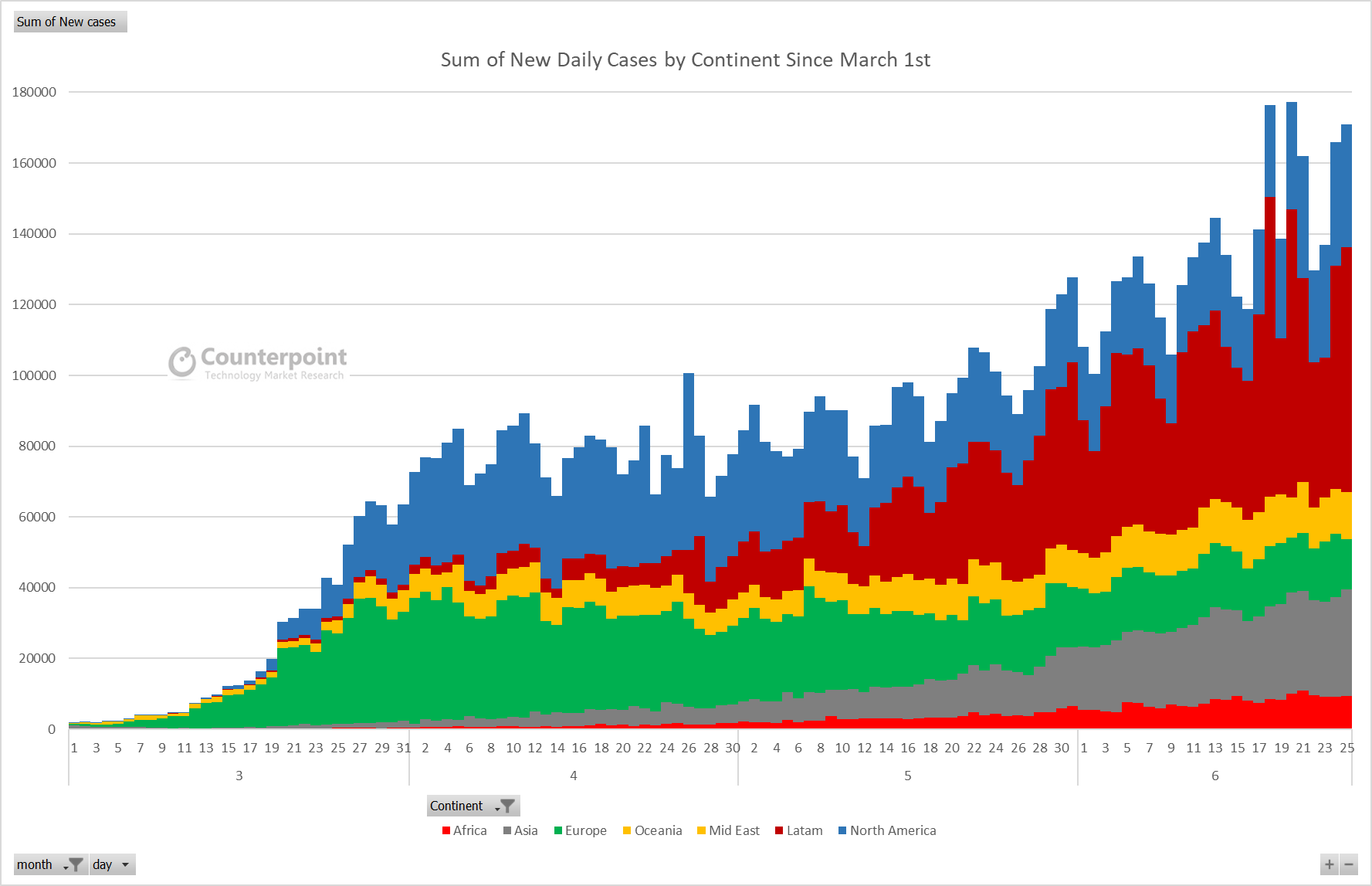

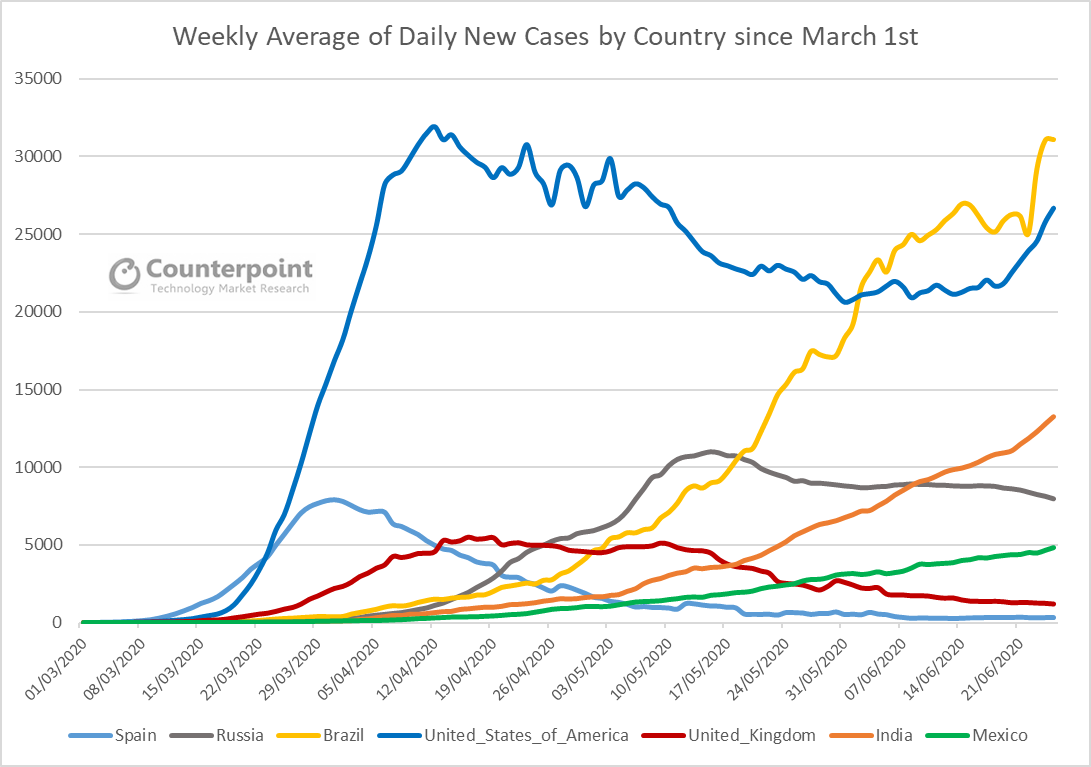

COVID-19 Week 80 Update

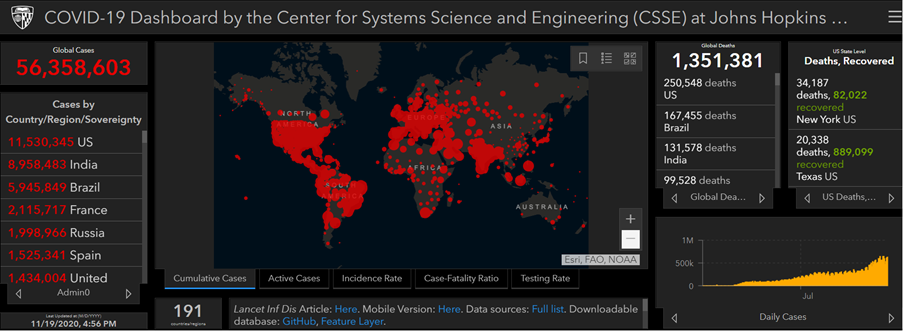

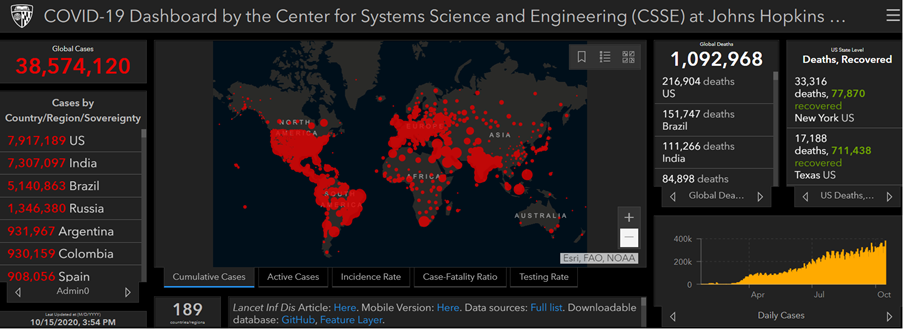

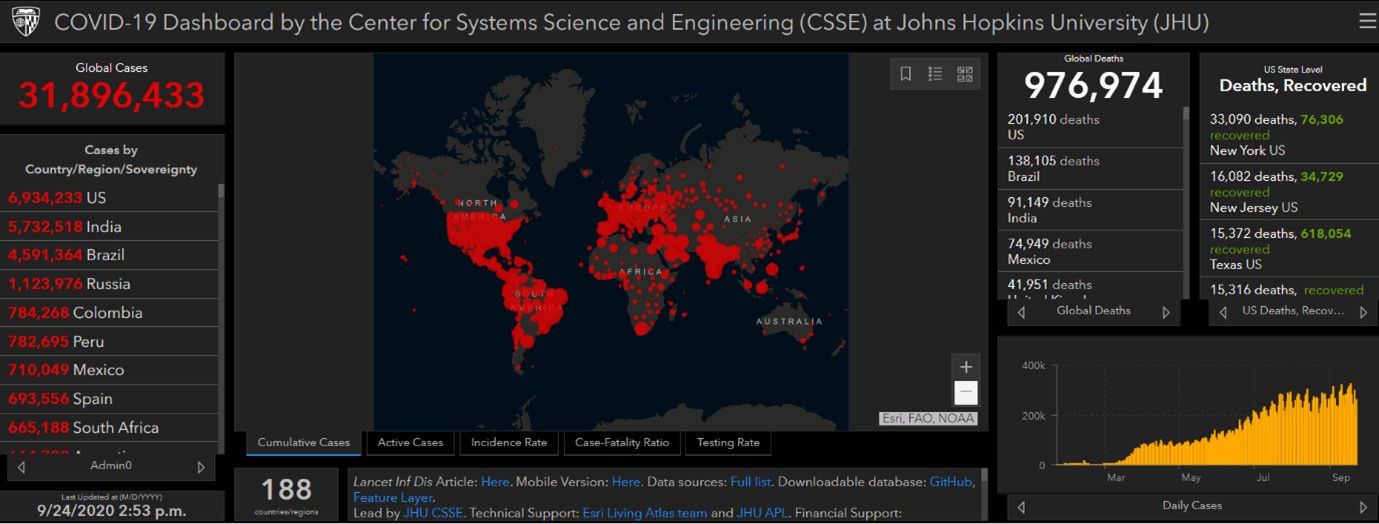

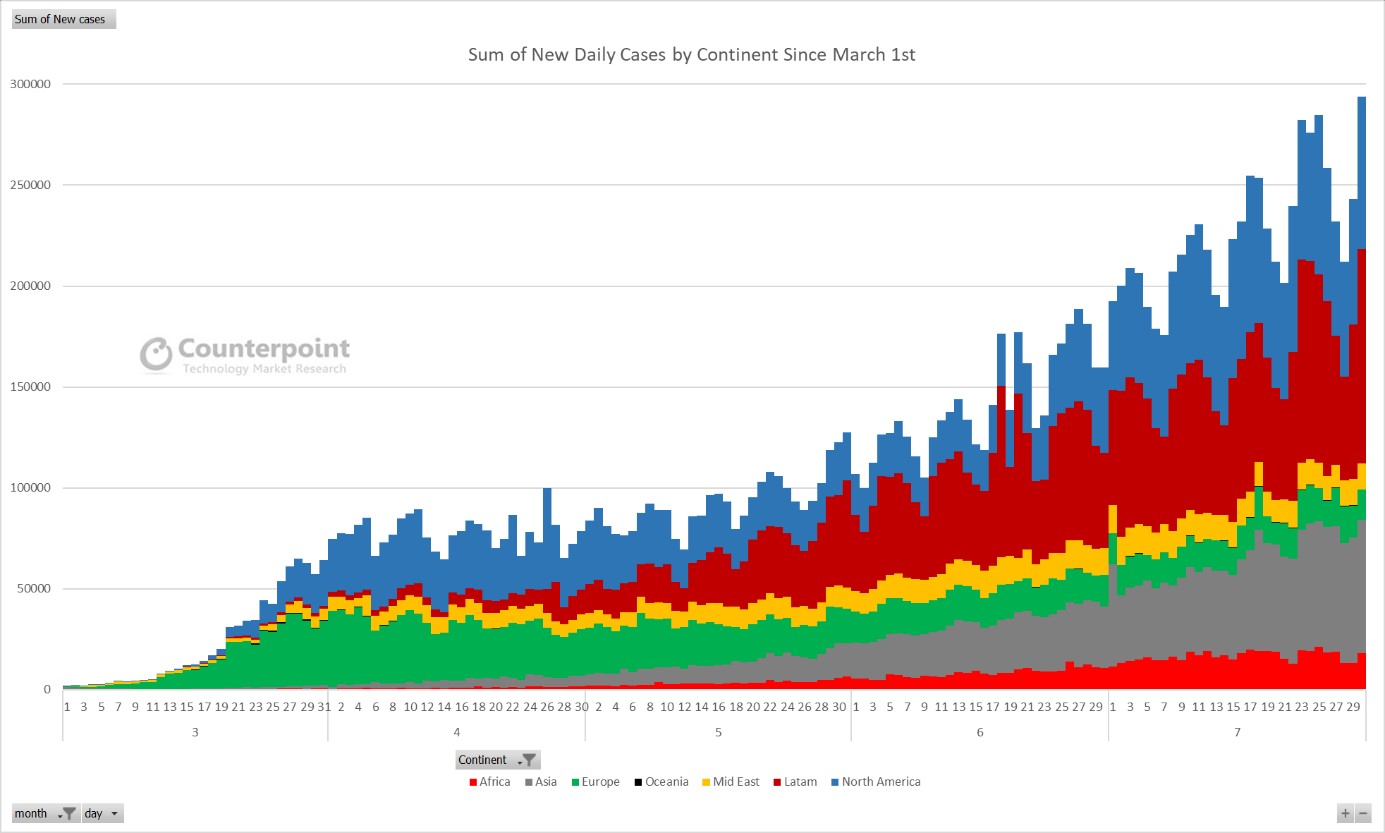

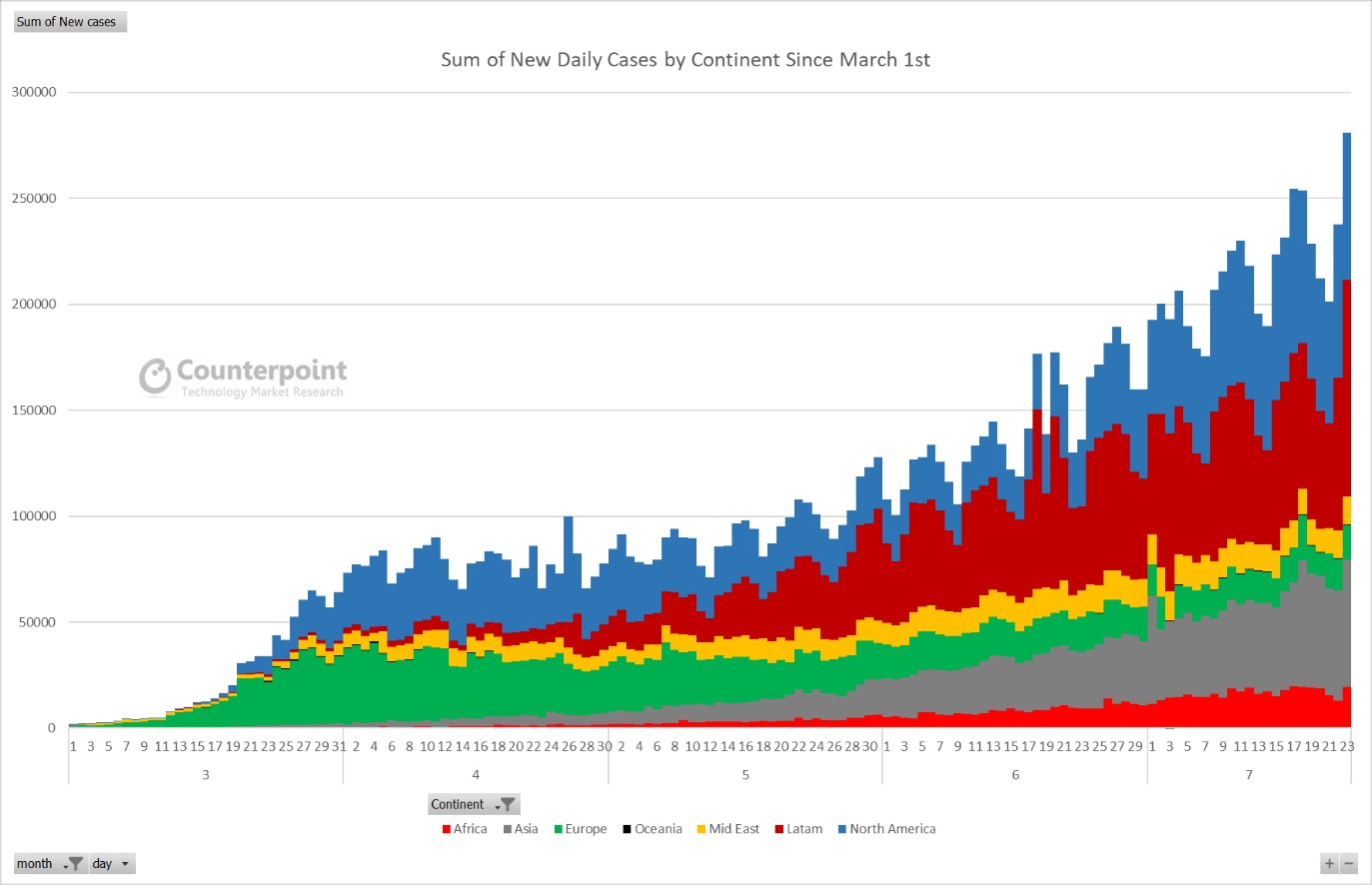

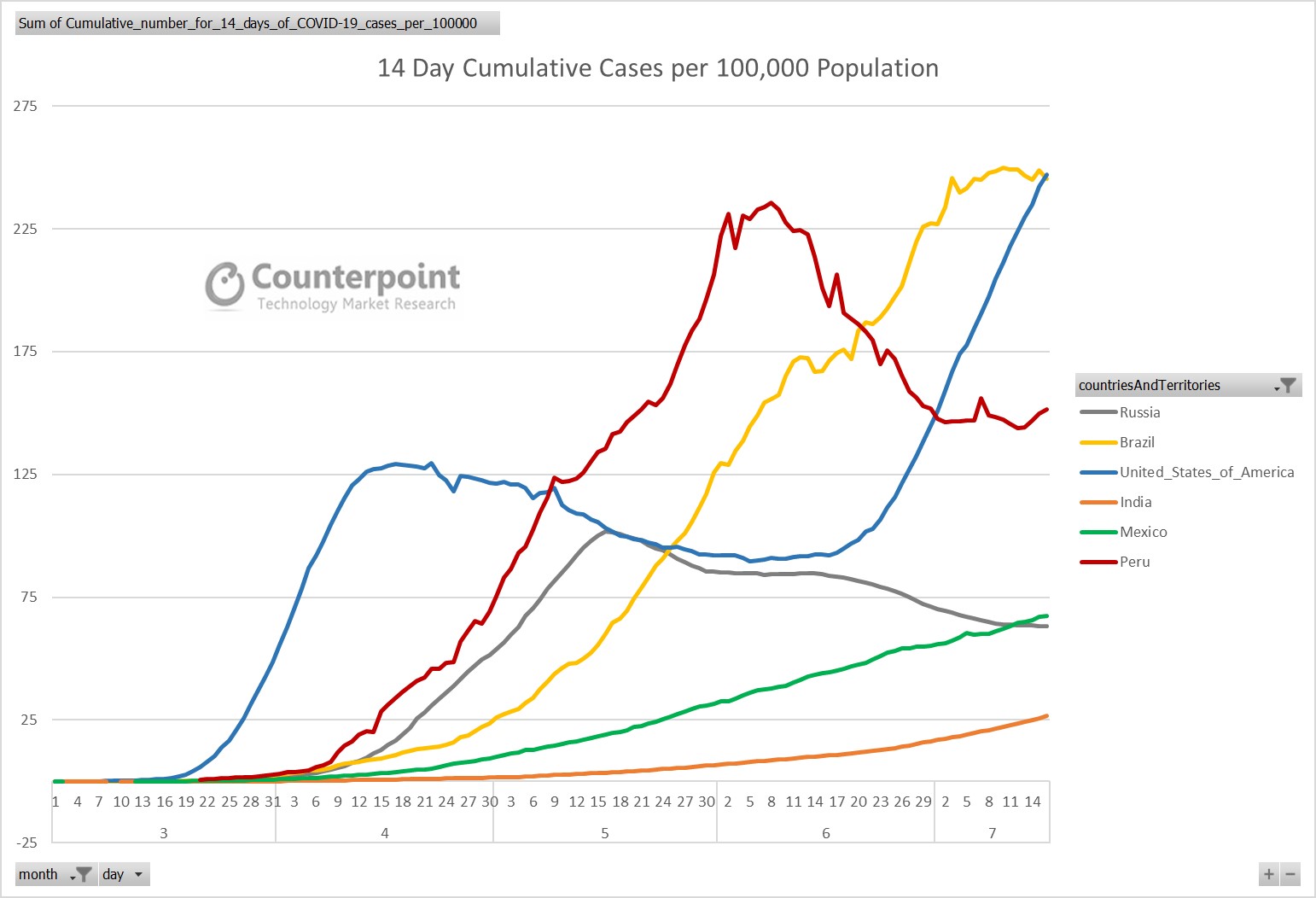

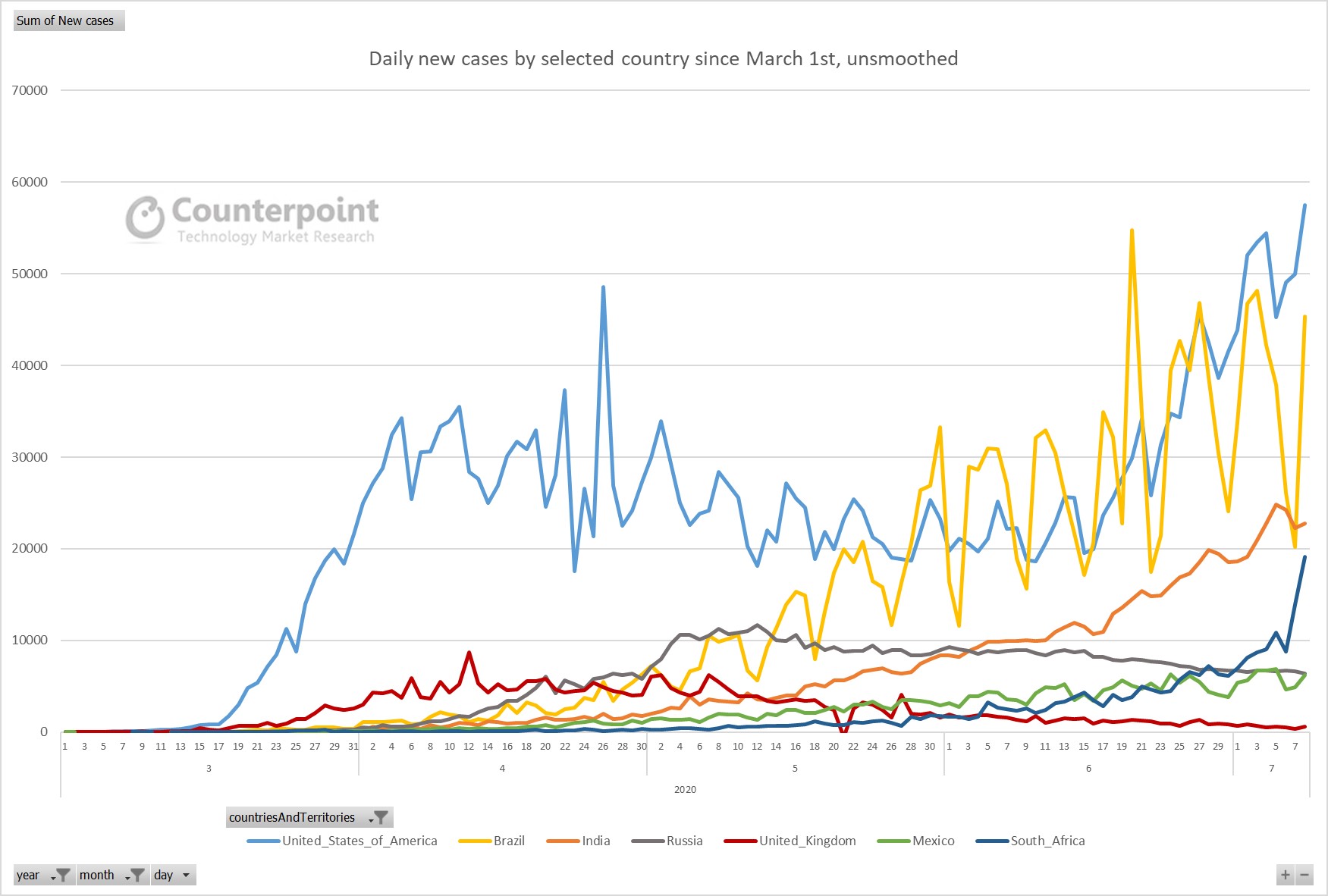

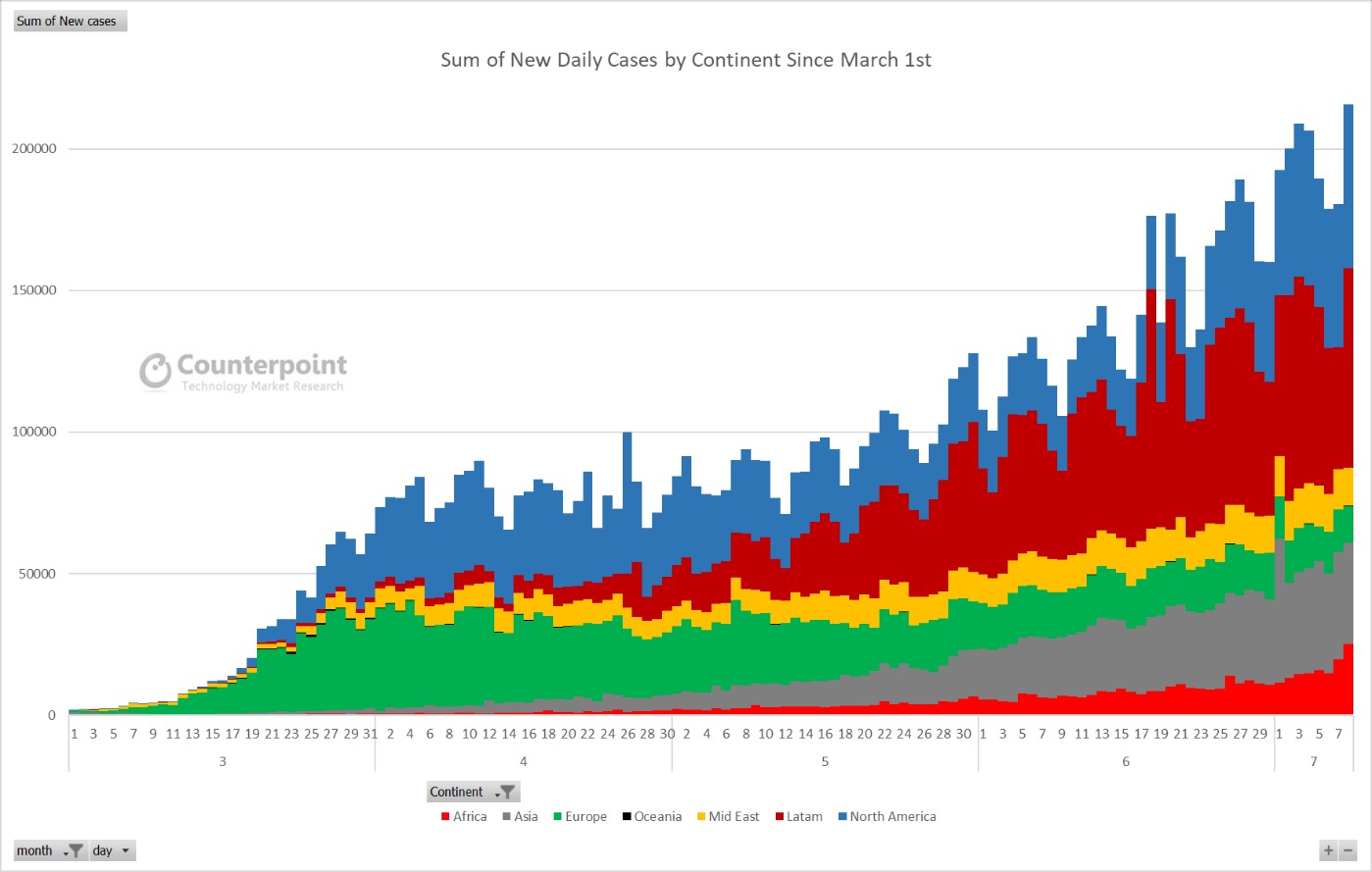

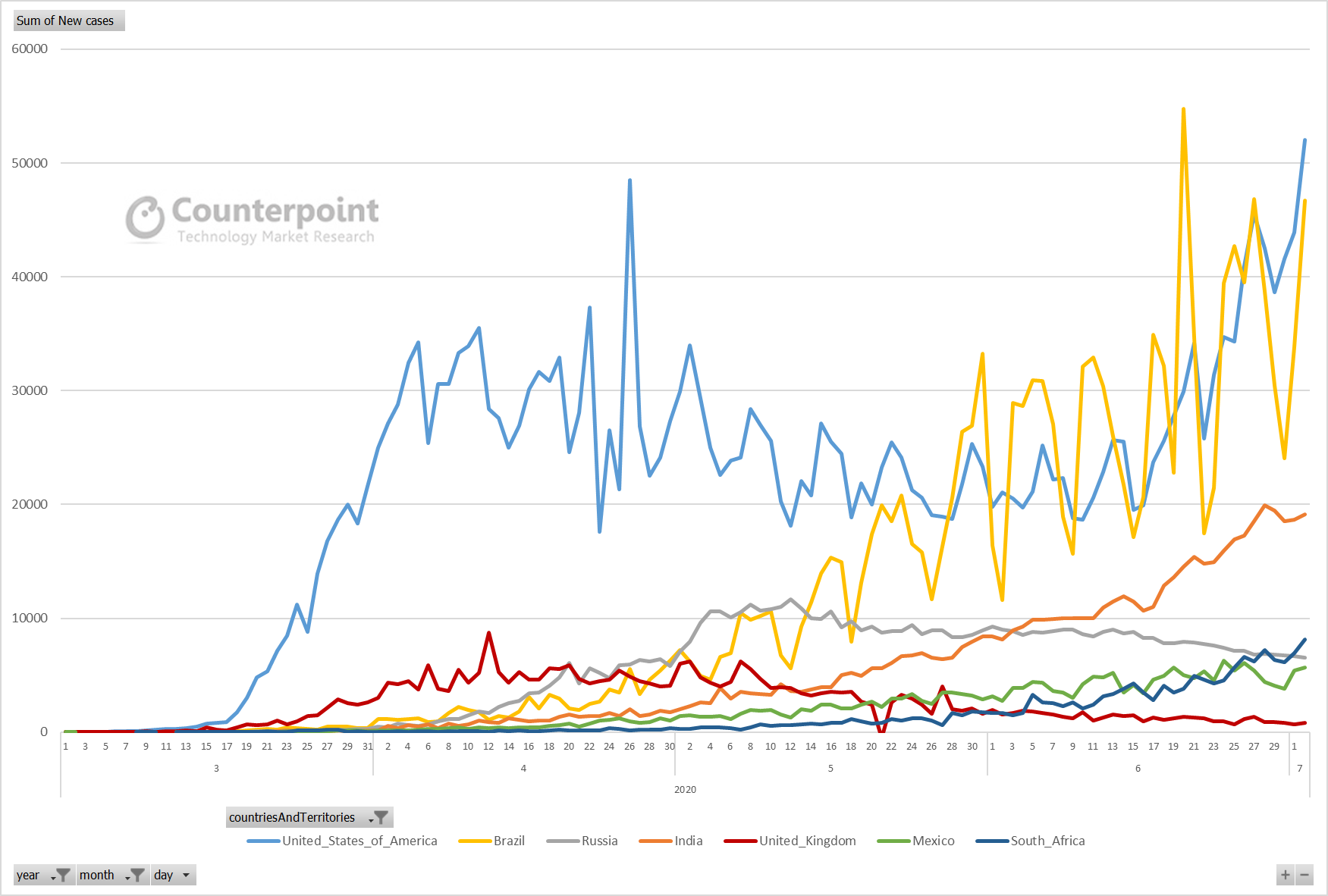

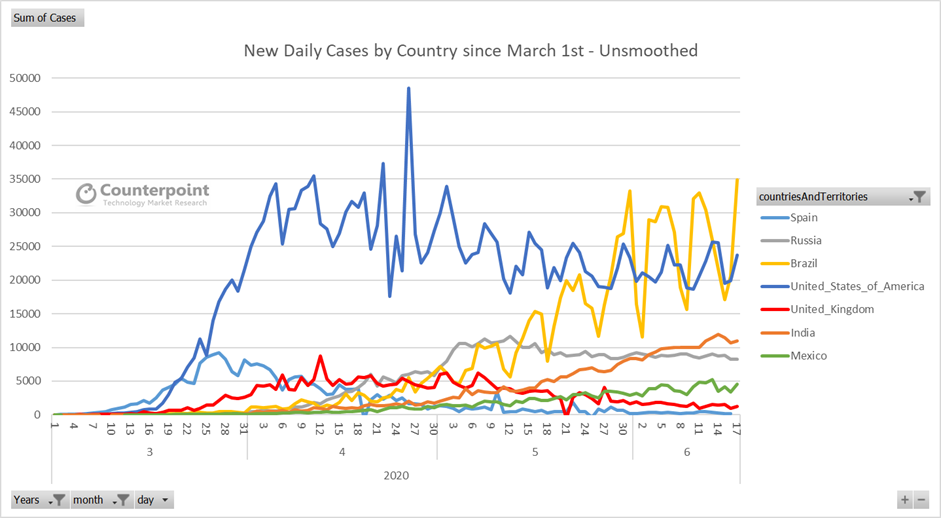

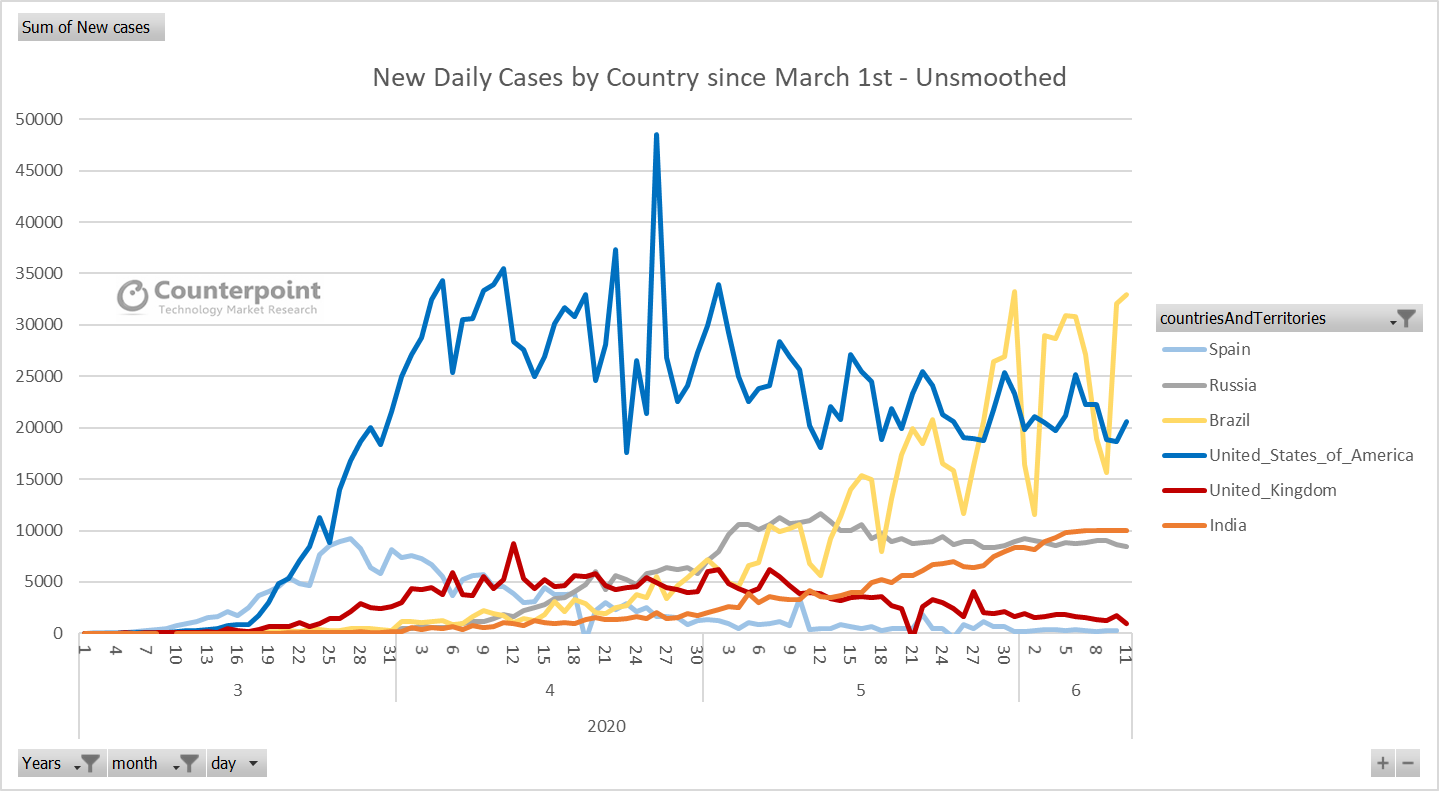

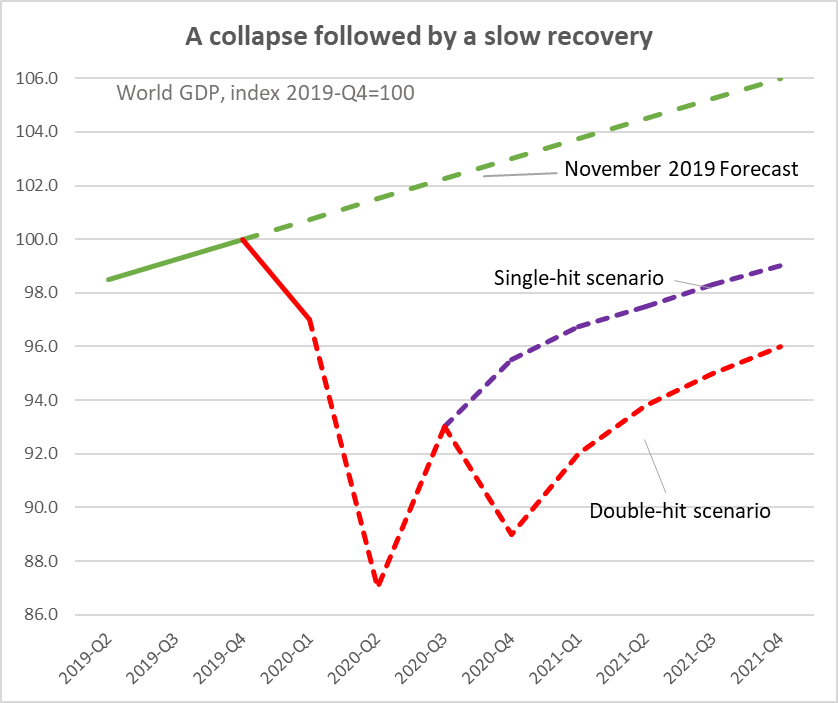

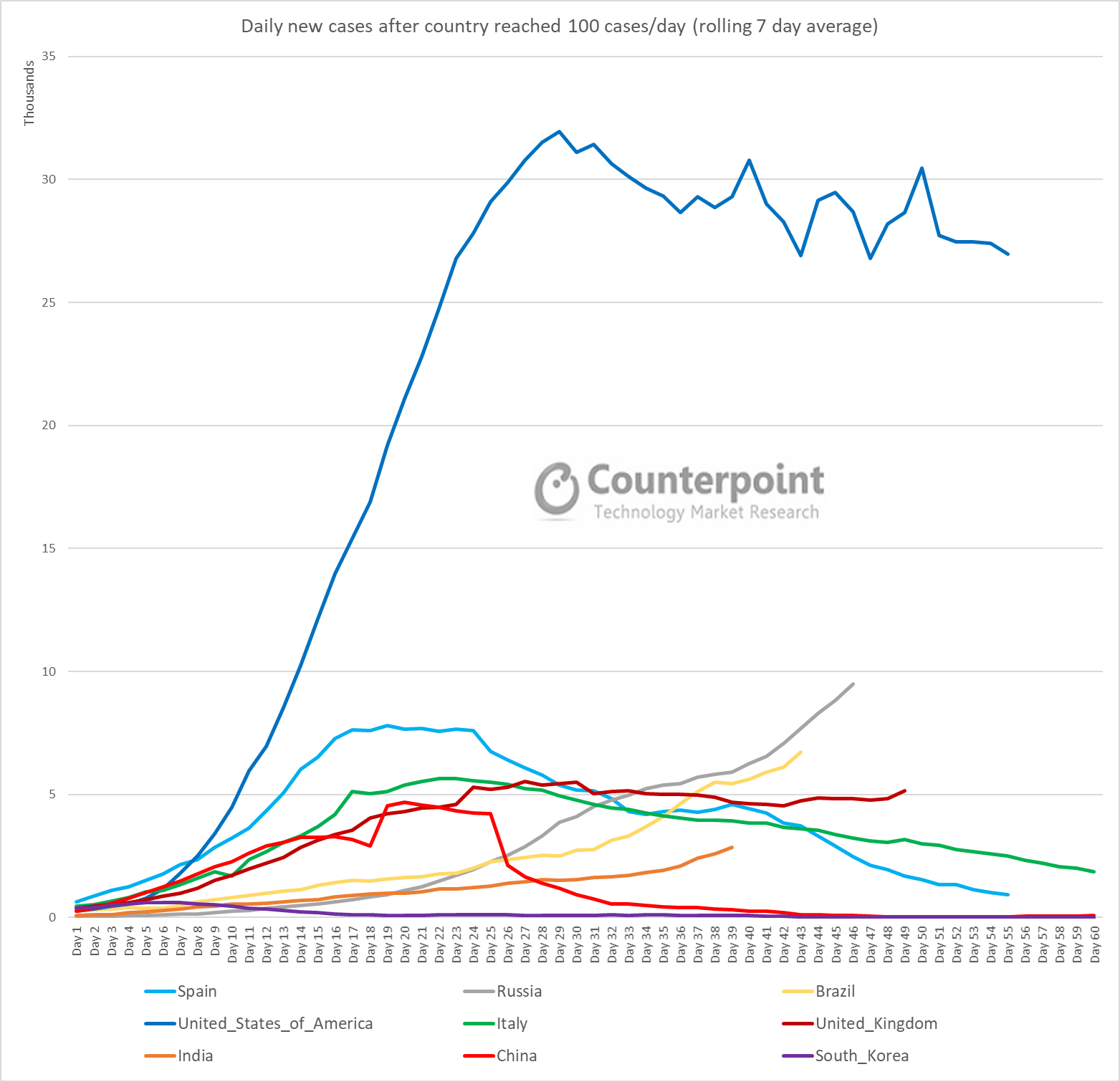

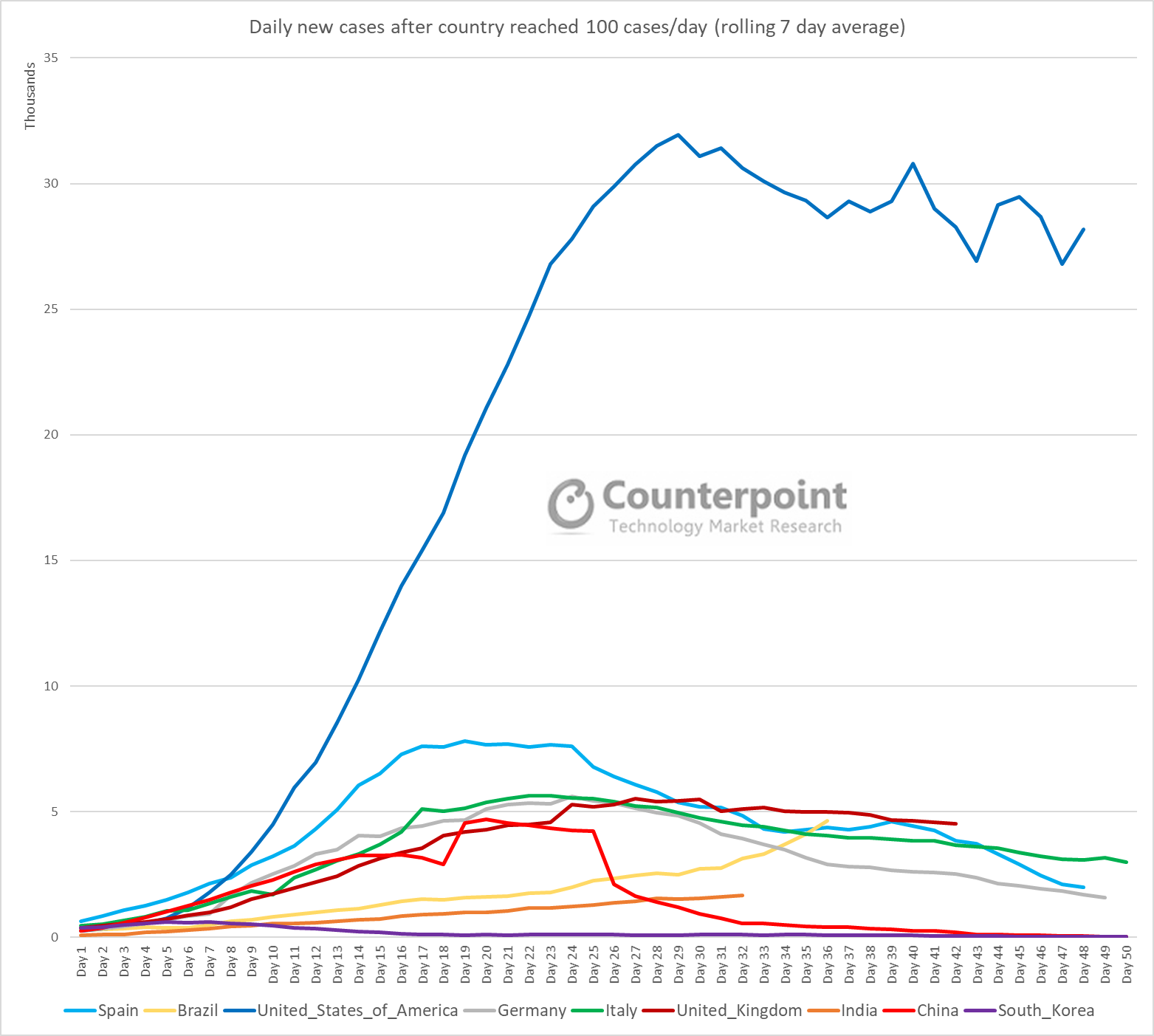

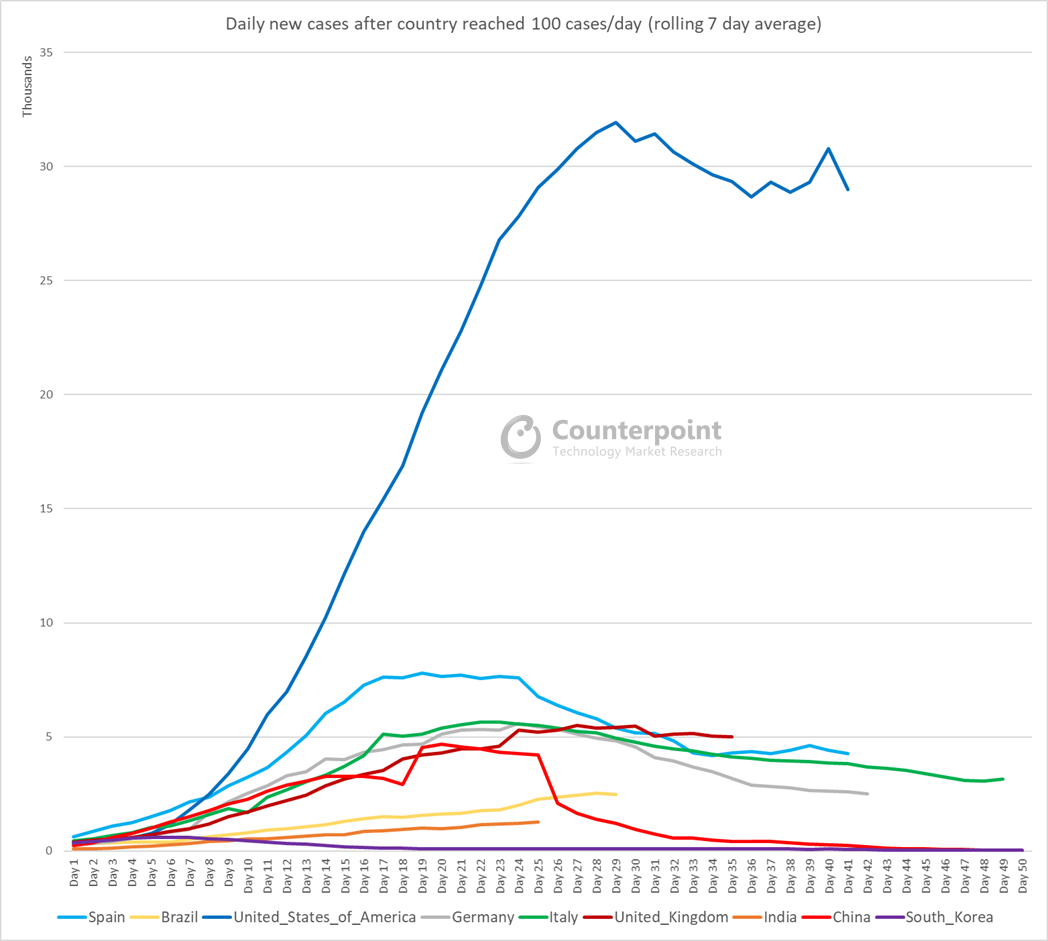

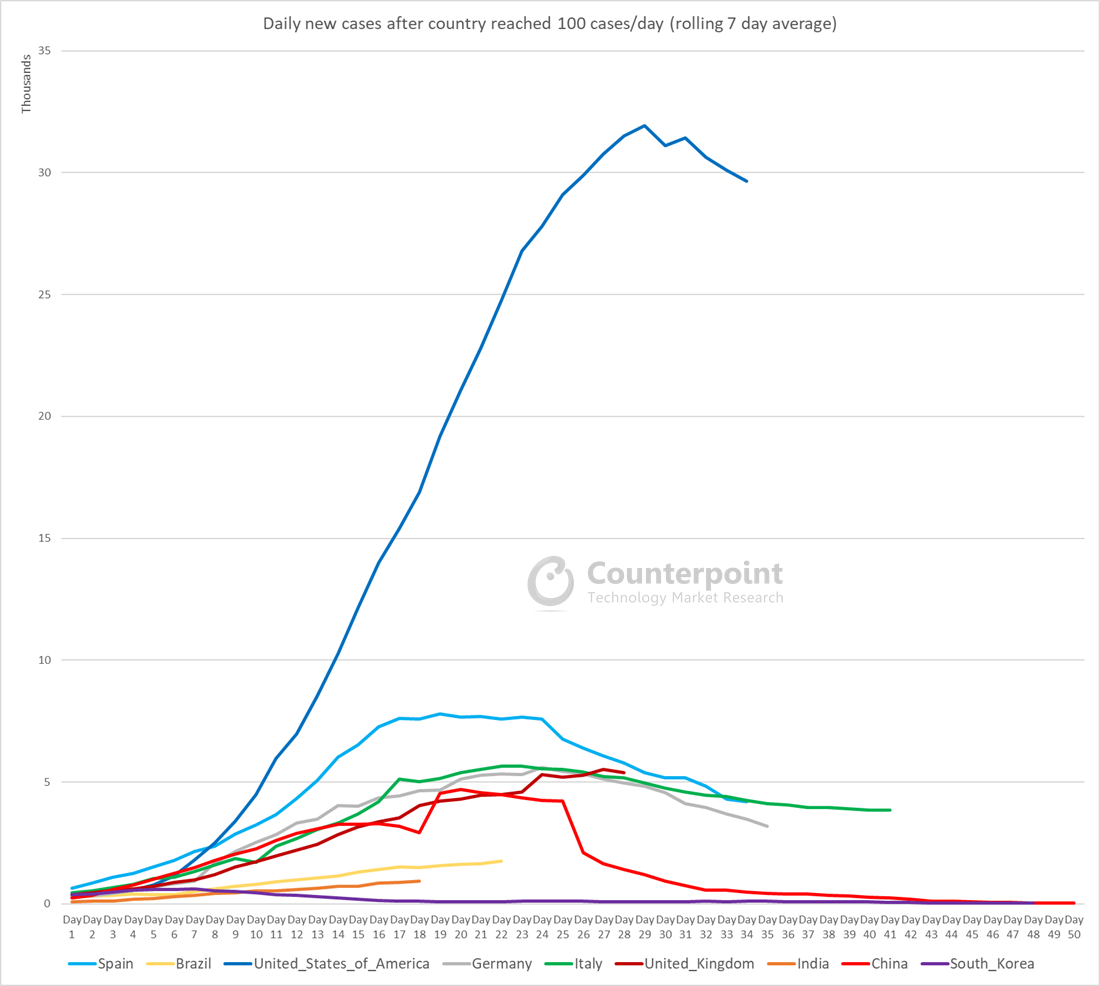

As we write this last instalment of our weekly coverage of the COVID-19 pandemic (we will continue to cover it elsewhere, particularly its impact on the tech industry), we are reminded of the situation same time last year. The virus was rapidly spreading in different parts of the world. India had overtaken Russia to become the country with the world’s third-highest number of COVID-19 cases, with the US and Brazil taking the first and second spots, respectively. US top infectious diseases expert Anthony Fauci was warning his country that it was still “knee-deep” in its first wave of infections and the number of cases was yet to reach a satisfactory baseline. The weakness in the global economy due to the pandemic was being expected to reflect in the Q2 numbers even as the companies catering to the work-from-home (WFH) economy were looking at a windfall.

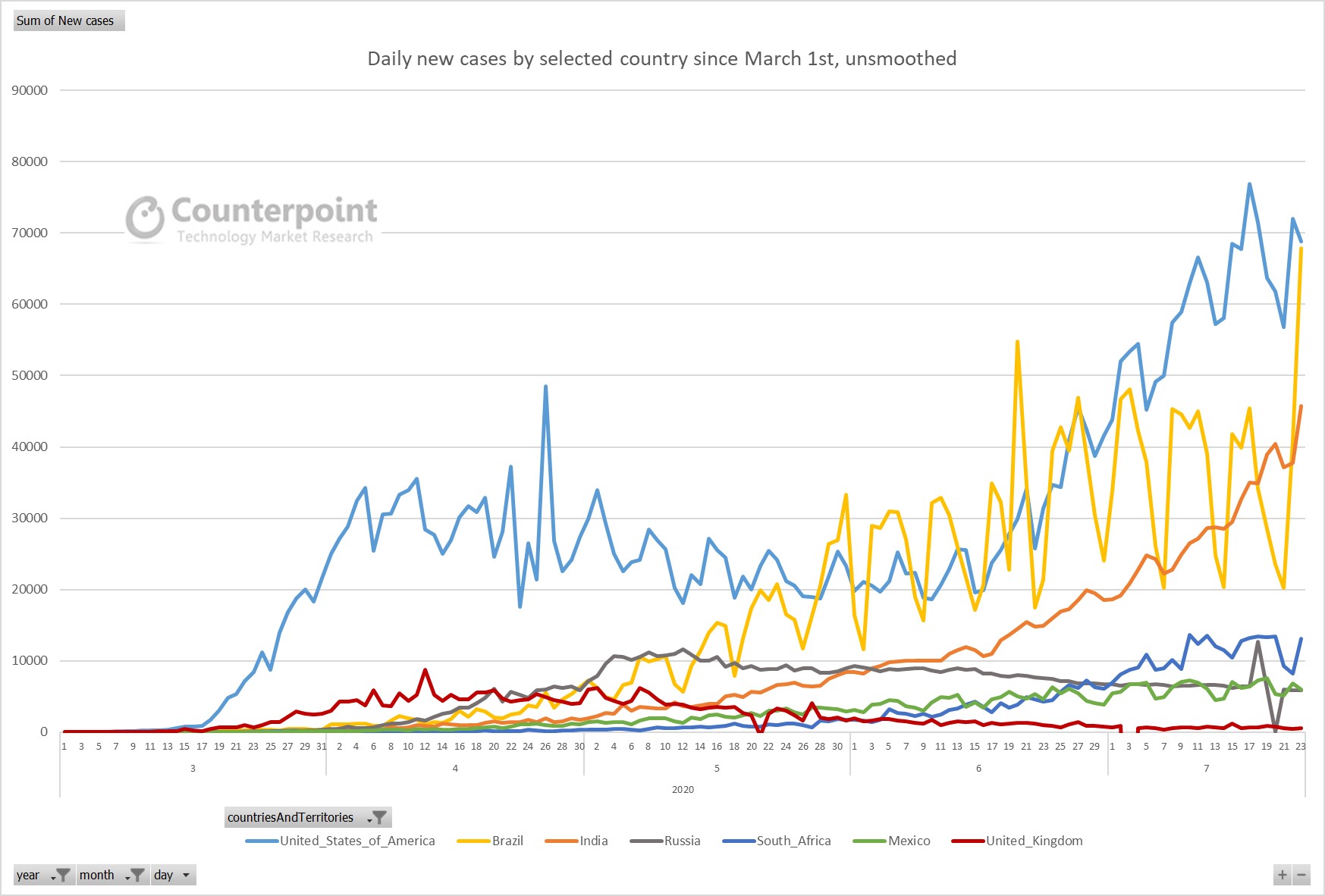

Coming back to today, the situation has hardly improved. The original virus may have moved out of focus, but it has left behind more virulent variants. Now, the most dangerous Delta variant is present in about 100 countries, according to the World Health Organisation (WHO). After ravaging India, this variant is now resulting in fresh waves in countries like Indonesia, UK, Russia, Iran, Colombia and South Africa. USA, India and Brazil continue to top the world in the total number of cases, though most daily new cases are now coming from Brazil, India and Indonesia. Fauci is now imploring Americans to get vaccinated to avoid another wave, triggered by the Delta variant this time. While the global economy as a whole has recovered, the recovery has been patchy, with the developing nations staring at weak annual numbers. Meanwhile, the companies catering to the WFH economy continue to report robust numbers.

What has changed is the availability of vaccines. But even here the developed world has benefited the most, thanks to the resources at its command. A big part of the world won’t get access to any vaccine till late 2022 or early 2023. The pandemic has exposed the weaknesses in supply chains, not just for vaccines but also for sectors as diverse as semiconductors and chemicals. Already, many countries have started taking measures to mitigate the risks on this front. The focus is on a reduction in dependence on other countries for critical supplies.

The pandemic has changed many things permanently and for the better. The issue of climate change is now taken more seriously. The lockdowns showed that nature can quickly heal itself under the right conditions. International cooperation is another beneficiary. The pandemic has taught the world that international problems require international cooperation.

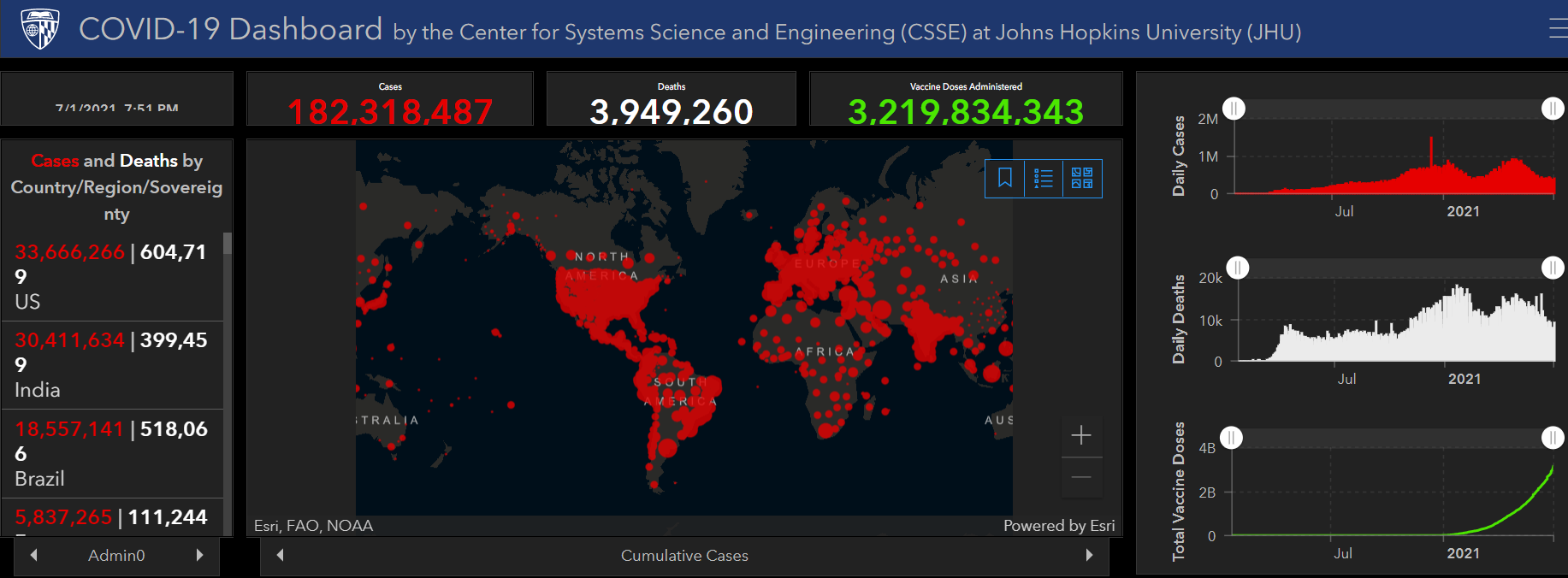

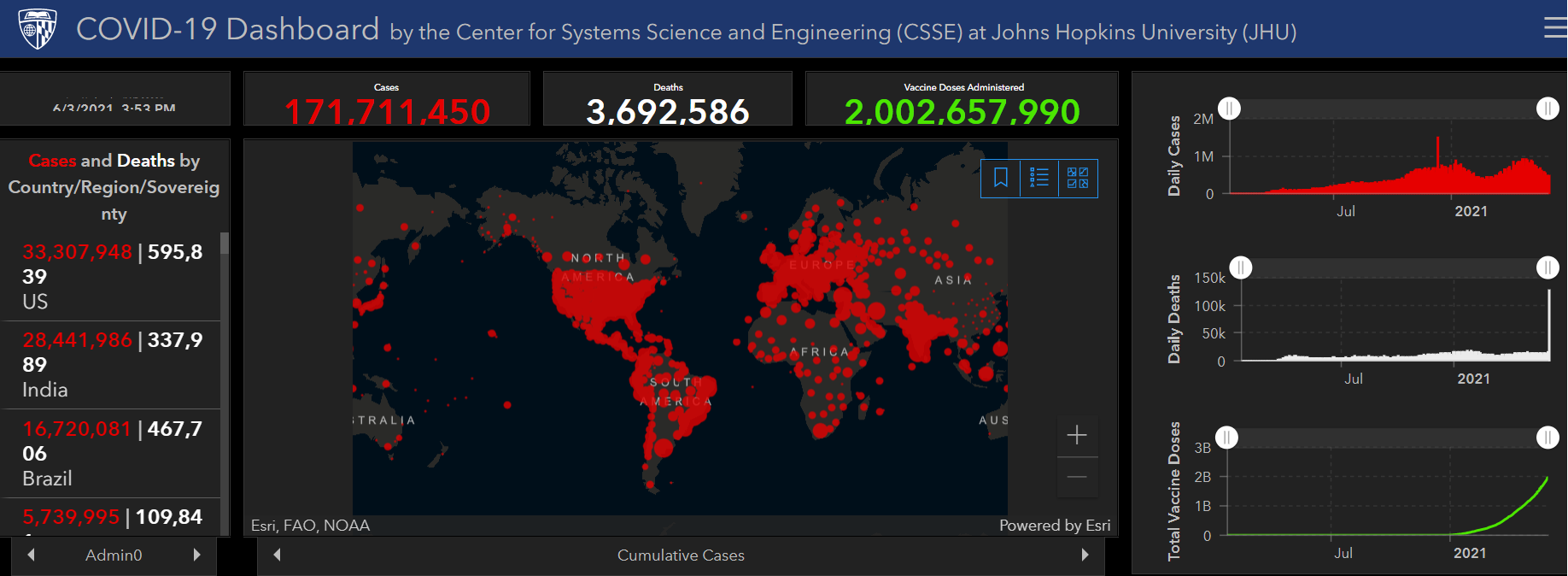

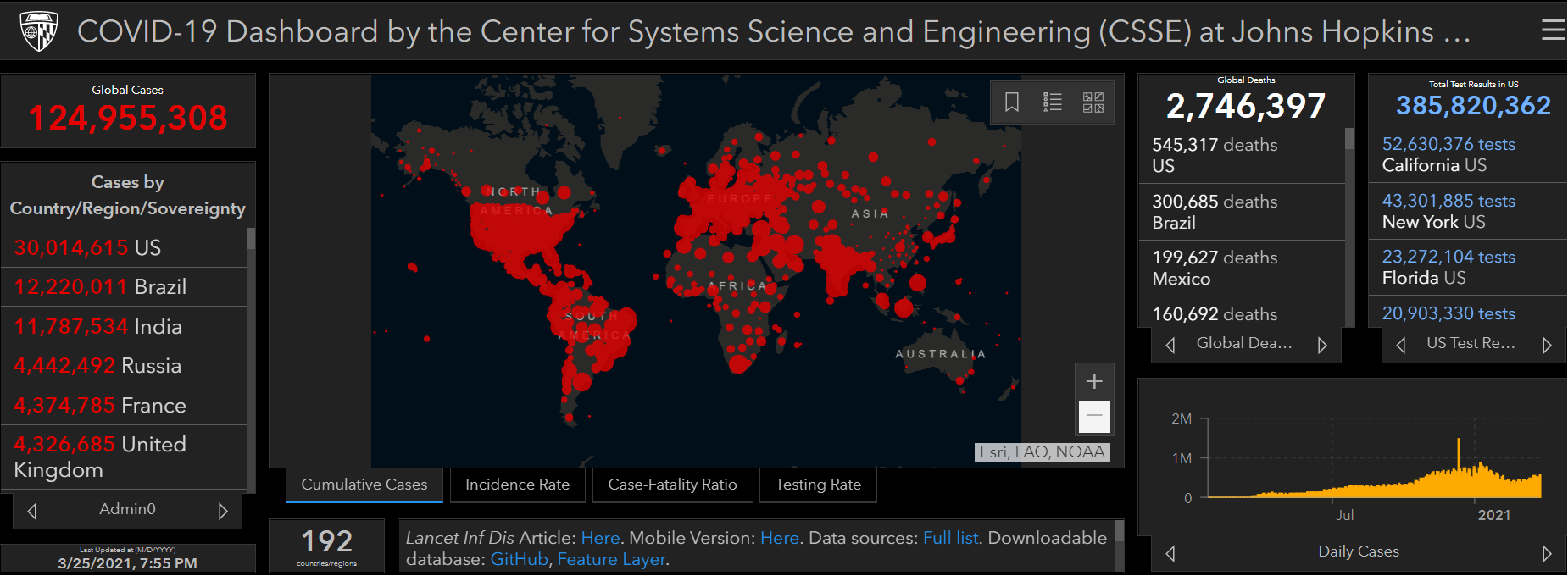

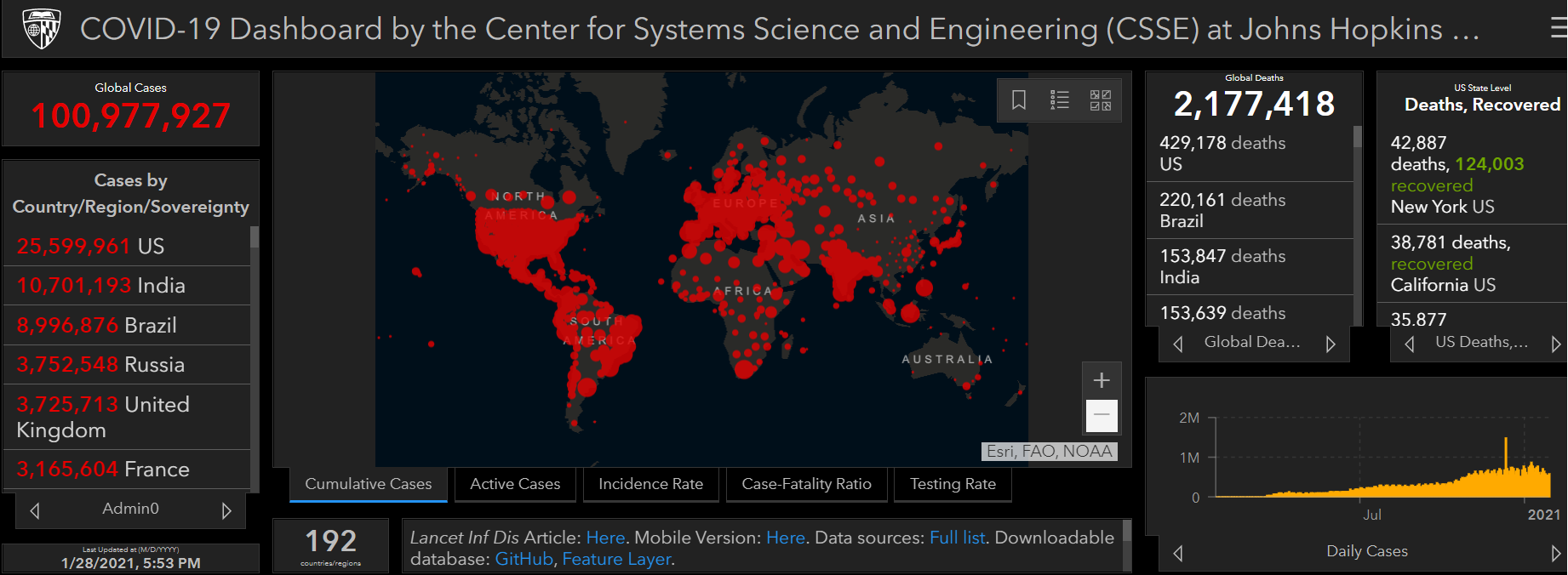

COVID-19 Week 79 Update

Israel is the most vaccinated major country currently, with over 55% of its 9.3 million population having received both doses of the Pfizer-BioNTech vaccine. In May, the eligibility to get vaccinated was extended to the 12-15 age group. But the response from this age group has been lukewarm, a big cause for worry as the most virulent Delta variant of COVID-19 marks its entry into the country. On Thursday, the country’s health ministry reported 307 daily new cases on Wednesday, the highest since April. The ministry reportedly expects this number to jump in the coming days. However, the death rate is firmly in check, perhaps due to the high vaccination rate. According to the ministry, only one person died during the past two weeks.

Confident that the worst was over, Israel had relaxed most of the COVID-related curbs over the last few months. But the Delta variant has now forced the authorities to make an about-turn. The rule requiring wearing of masks indoors has been brought back even as the government rushes to vaccinate children. A “coronavirus commissioner” has been appointed for the first time to monitor arrivals at Israel’s main international airport. The interior minister says the airport will be shut if the situation worsens. The government has already postponed the planned reopening of the country to vaccinated tourists.

Meanwhile, the World Health Organization (WHO) says COVID-19 cases are rising again in Europe after two months of decline. A WHO official said the number of cases rose by 10% last week, warning a fresh wave would come “unless we remain disciplined”. The European Union’s (EU) disease control agency, European Centre for Disease Prevention and Control, estimates that the Delta variant will account for 90% of new cases in the EU region by August end.

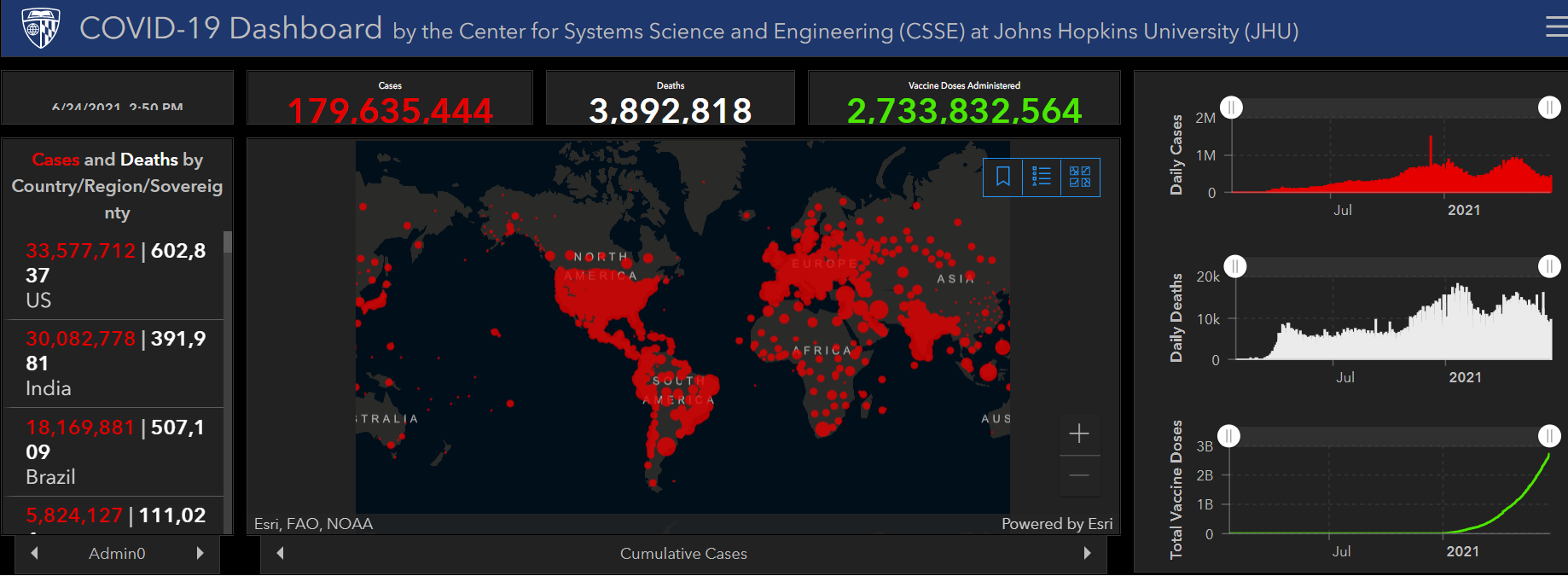

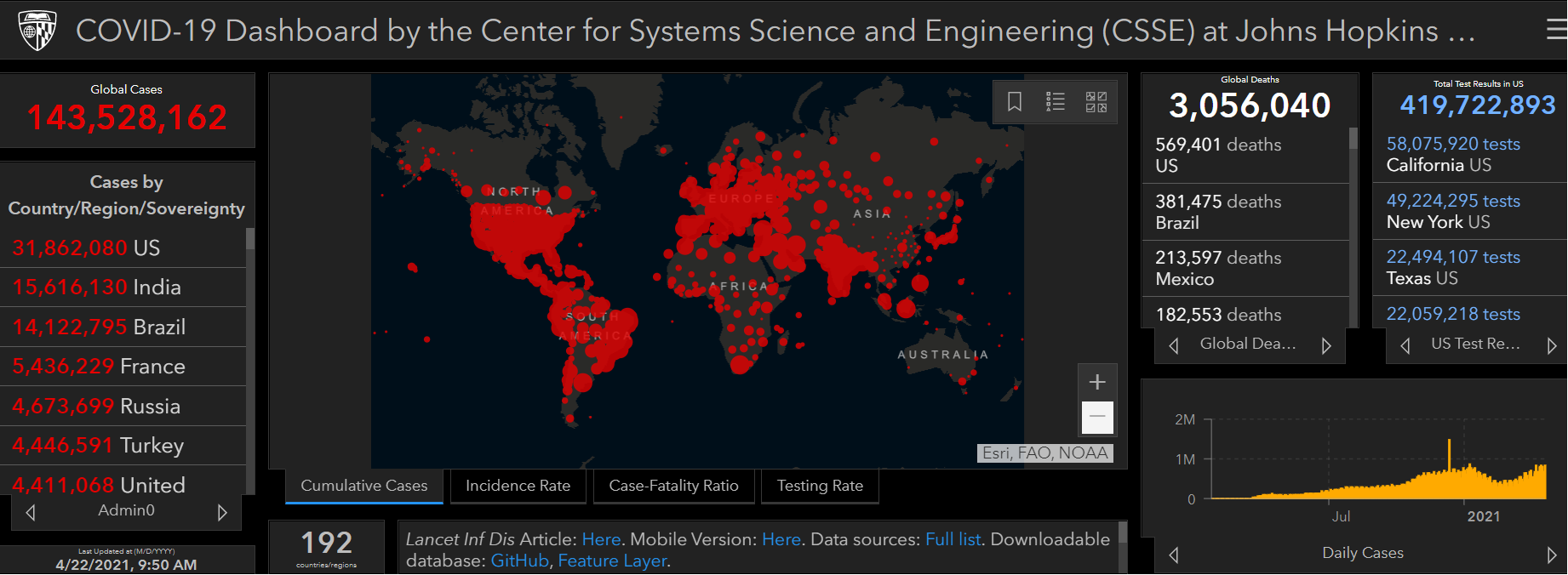

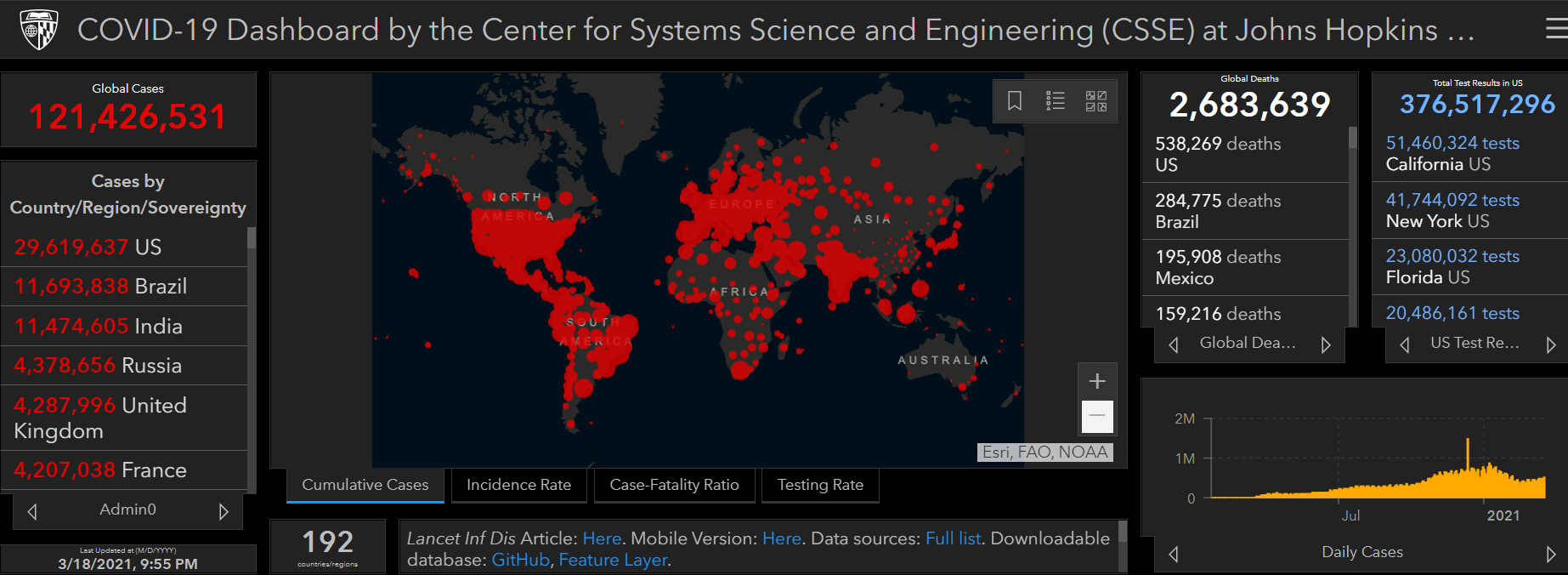

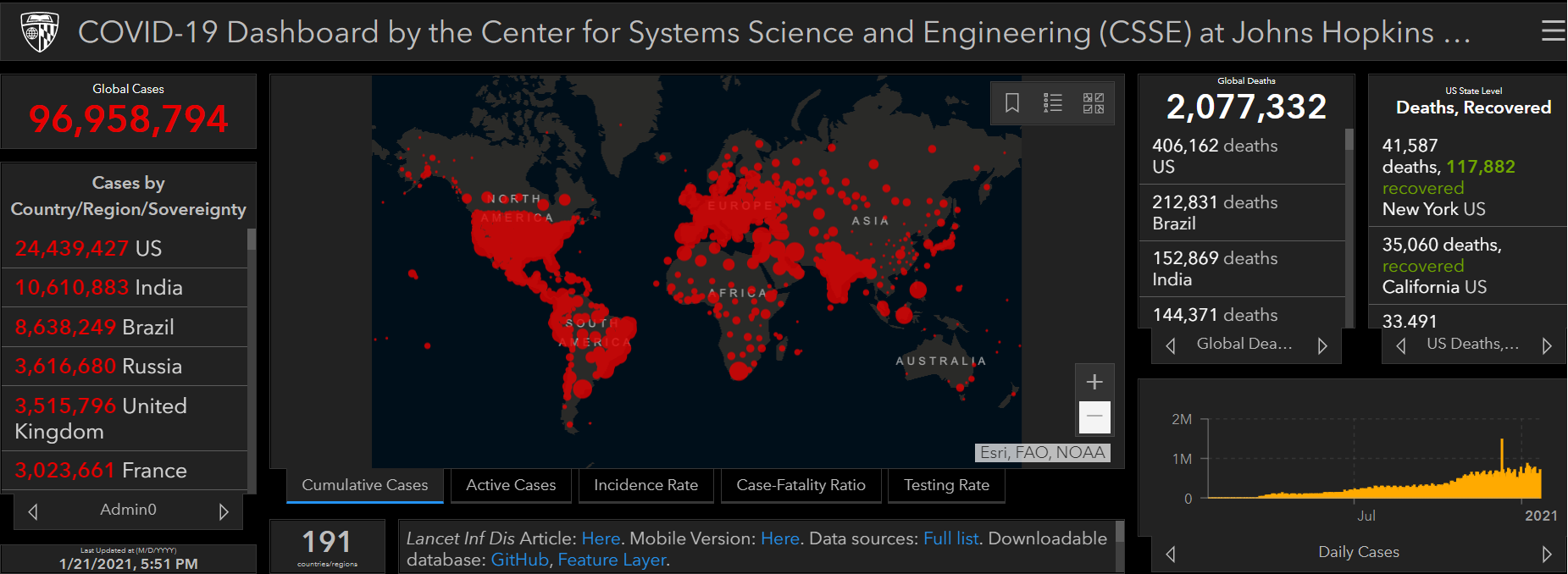

COVID-19 Week 78 Update

The Delta variant of COVID-19 has spawned a deadlier variant, called Delta Plus. India, which has so far detected over 40 cases of Delta Plus, has already declared it as a “variant of concern”. The country reported its first death due to this variant on Wednesday. Ten other countries, including the US, UK and Russia, have also reported Delta Plus cases.

The Delta Plus variant has the spike protein mutation K417N, also found in the Beta variant first detected in South Africa. While studies are on to test the effectiveness of available vaccines against the latest variant, experts say it is resistant to monoclonal antibodies cocktail. On the chances of another COVID-19 wave, they say it could happen if people fail to follow COVID-appropriate behaviour.

Meanwhile, chief medical advisor to US president Anthony Fauci has described the Delta variant as the “greatest threat” in the country’s fight against the pandemic as it is more transmissible. According to Fauci, the Delta variant now makes up over 20% of new cases in the US, compared to 10% two weeks ago.

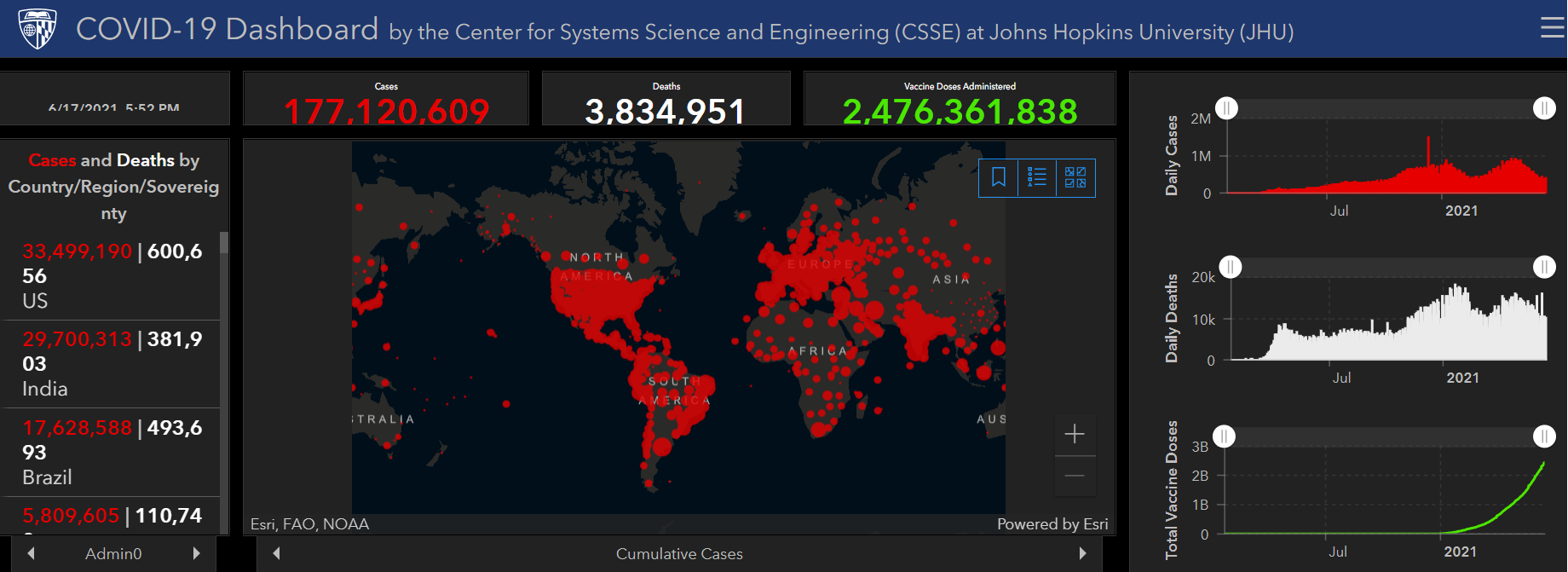

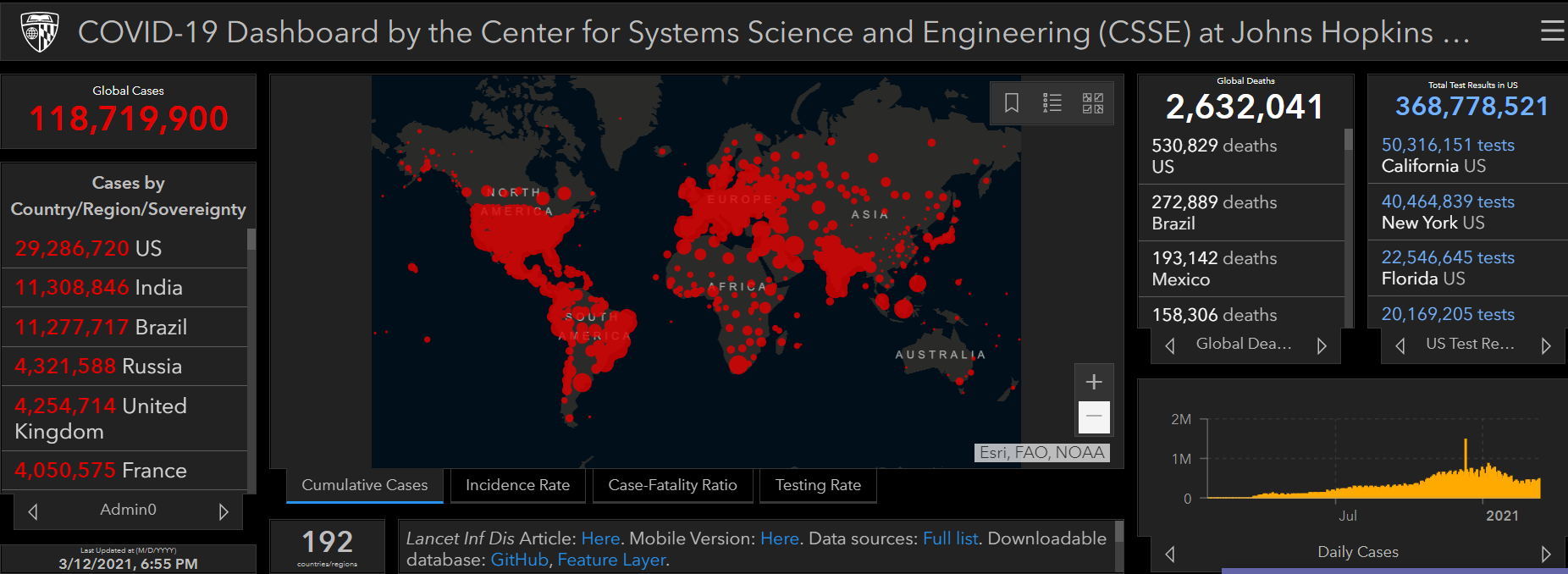

COVID-19 Week 77 Update

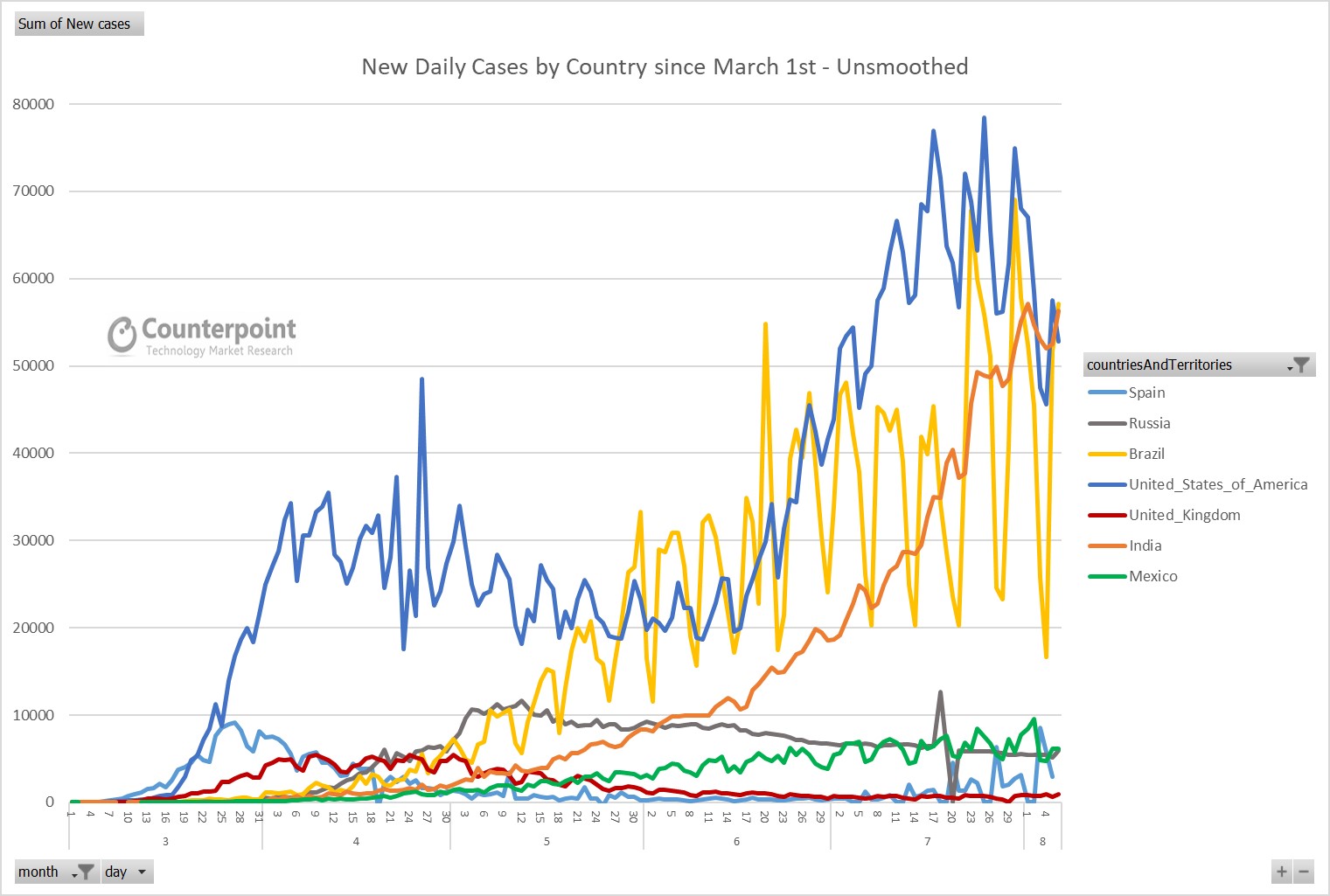

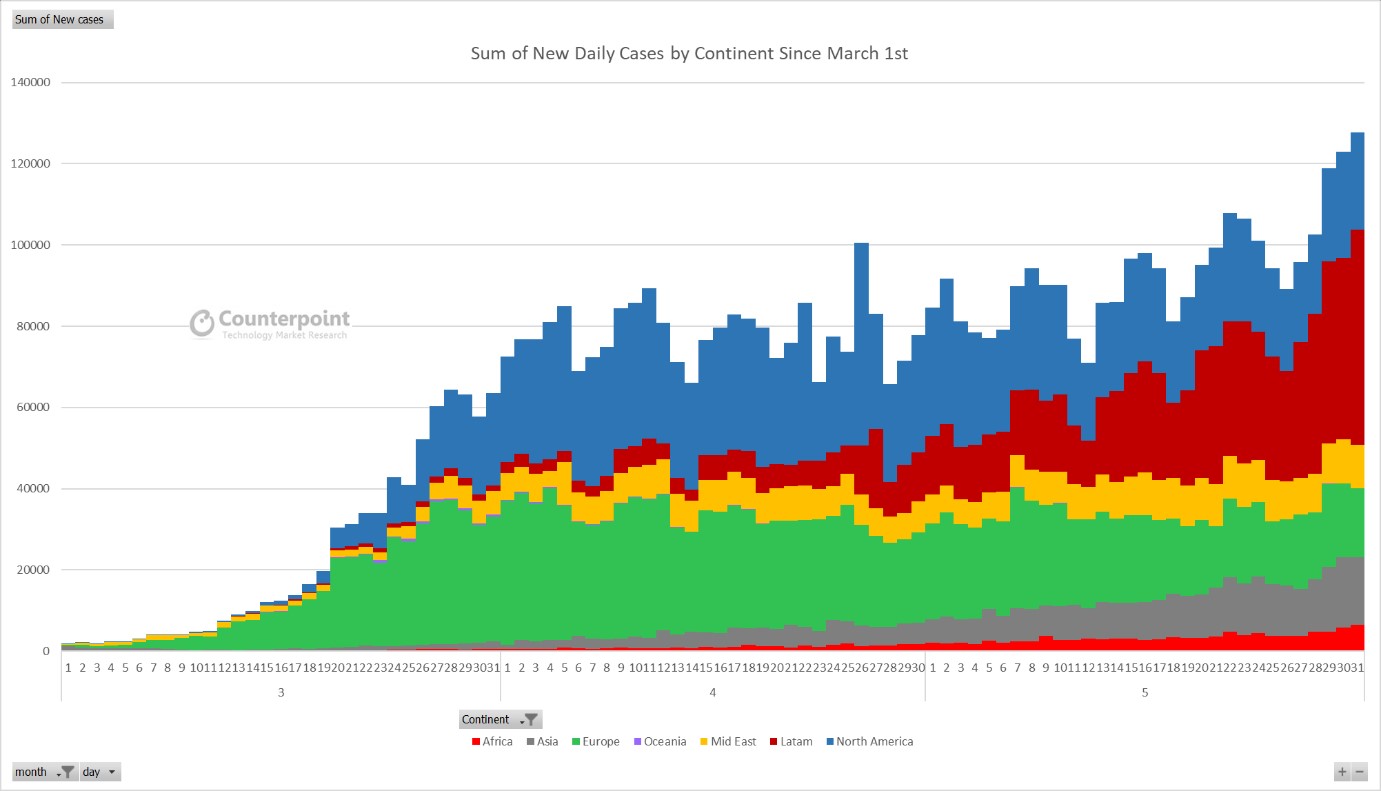

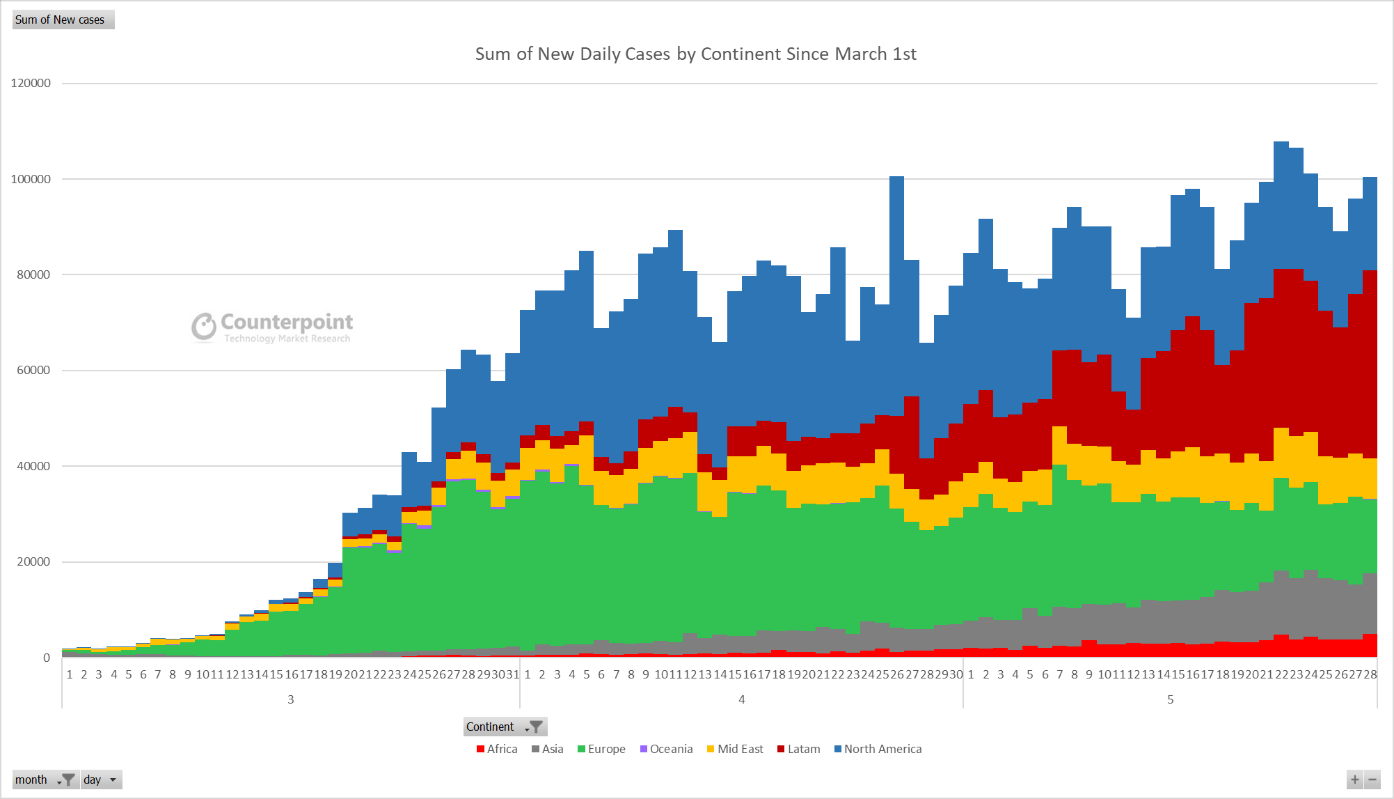

While the daily new COVID-19 cases globally have come down to mid-March levels, the pandemic continues to rage in many countries in South America, Asia and Africa. Among the Top 10 countries in terms of daily new cases (listed below), as many as six are seeing fresh spikes in cases due to the different COVID-19 variants in circulation:

- Brazil (↑): With only around 10% of its population receiving the first vaccine dose, Brazil still went ahead with organizing the Copa America football tournament. More than 30 players and officials have already tested positive.

- India (↓): Even as cases go down, the country is in the midst of a debate triggered by a statement from three officials of a key panel that there was no agreement among the panel members when the decision to double the gap between two AstraZeneca vaccine doses to up to 16 weeks was taken.

- Colombia (↑): The country is going through its worst COVID wave so far. ICUs in many cities are reporting full capacities. Quarantine measures taken in April-May have been undone by the large protests across the country which added to the increase in cases.

- Argentina (↓): Officials have cited the decreasing levels of cases to justify the resumption of in-person classes for more than 3 million children in the Buenos Aires province after a two-month suspension.

- USA (↓): The country has inked a deal with Moderna to buy 200 million more doses of its vaccine for primary vaccination as well as for a booster shot for those fully vaccinated if the need arises.

- Russia (↑): The country may be promoting its Sputnik vaccine globally, but only 10% of the citizens have been fully vaccinated so far, thanks to some hesitancy and skepticism. As a result, all Moscow city workers with public-facing roles have been ordered to get vaccinated.

- South Africa (↑): With a fresh spike in cases, the country has reimposed curbs on public gatherings and alcohol sales. President Cyril Ramaphosa says the fresh wave has put the country’s health system under pressure, with COVID-related hospital admissions rising by 59% in many areas.

- Iran (↓): The country has approved emergency use of its first homegrown vaccine after failing to procure sufficient vaccines from abroad. Iranians will vote on Friday to elect a new president. Projections are putting the voter turnout at a historic low.

- Indonesia (↑): Reports say quoting officials that more than 350 doctors and medical workers have caught the virus despite taking the Sinovac vaccine. Indonesia is projecting the current wave of infections to peak in July, with the Delta variant of COVID-19 becoming more dominant.

- UK (↑): A study led by Imperial College, London, says that the Delta variant of COVID-19 was responsible for a 50% rise in infections in the country since May. The fresh numbers came after Prime Minister Boris Johnson’s announcement to delay the lifting of pandemic-related restrictions to July 19 due to the rising cases of the Delta variant.

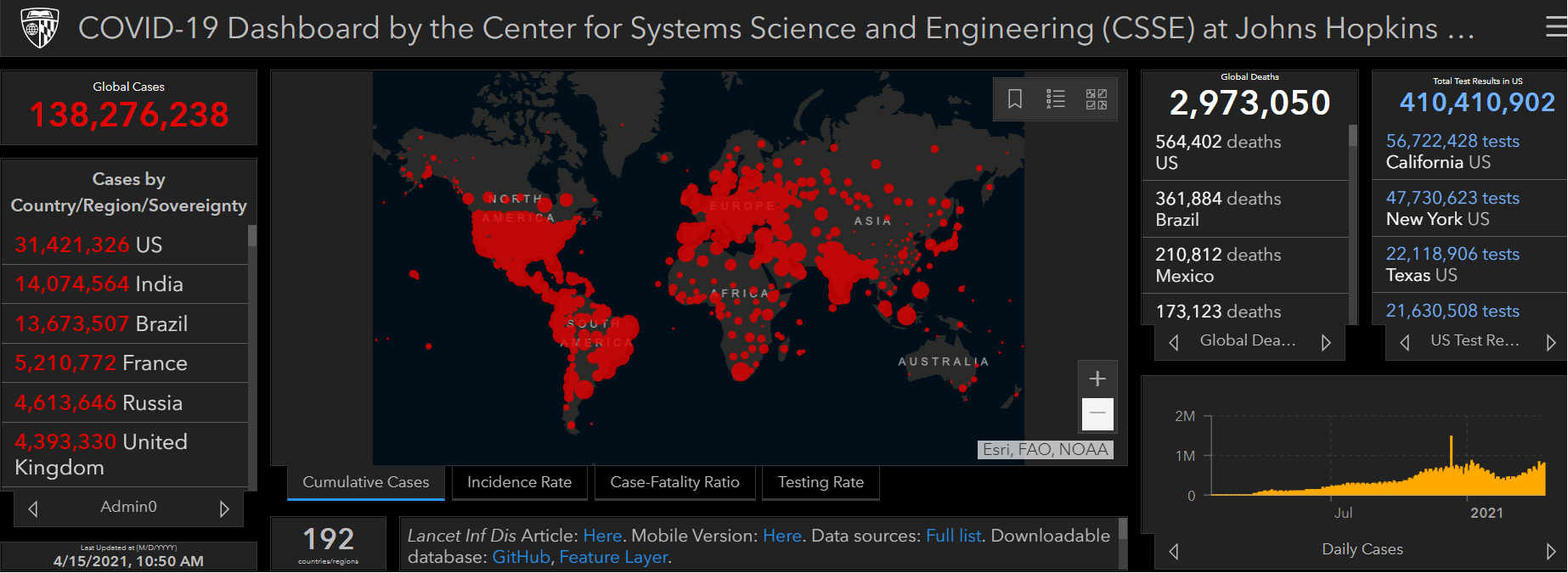

COVID-19 Week 76 Update

After ravaging India, the B.1.617.2 COVID-19 variant, which was first detected in the country and is now dubbed the ‘Delta variant’ by the World Health Organization, is spreading to the rest of the world. It is now present in as many as 60 countries and rapidly expanding there. Health officials the world over, including in countries with comparatively high vaccination rates, are alarmed. The Delta variant is estimated to be 50% more transmissible than the B.1.1.7 variant, first detected in the UK and now called the Alpha variant. The Delta variant can even affect those who have already had the infection. Public Health England data shows the Pfizer and AstraZeneca vaccines were only about 33% effective against the Delta variant after one dose, compared to 50% in the case of the Alpha variant. However, after two doses, the efficacy against the Delta variant increased to 88% and 60% for the Pfizer and AstraZeneca vaccines, respectively.

Clearly, vaccination remains important across variants. But thanks to the huge demand-supply gap, a major part of the world will have to bear the brunt of the Delta variant. Even in countries like the UK and US, where more than 40% of the population has been fully vaccinated, authorities are concerned over the Delta variant. In the UK, this variant has now overtaken the Alpha variant to contribute to more than 75% of the coronavirus cases. There has also been a noticeable increase in daily new cases and hospitalizations, so much so that the government has been forced to reconsider the plan to completely lift COVID-19 restrictions from June 21. Some experts are even warning of a third wave, though with fewer deaths thanks to vaccination. In the US, President Joe Biden and National Institute of Allergy and Infectious Diseases director Anthony Fauci have appealed to the country’s youths to get vaccinated to avoid a UK-like situation where the Delta variant is spreading more among those in the 12-20 age group.

COVID-19 Week 75 Update

The pandemic-triggered global chip shortage continues to hold strong with industry leaders hinting at a long haul. Some developments on this front during this week:

- Intel CEO Pat Gelsinger says the global semiconductor shortage could take several years to resolve. He feels it could take “a couple of years” to meet the shortfall on the foundry capacity side.

- Logitech CEO Bracken Darrell sees the shortage lasting 3-6 months, with some industry segments experiencing it for up to a year. The computer peripherals manufacturer is relying on new suppliers to meet its demand after facing shortages at its existing suppliers.

- Dell CFO Thomas Sweet said during a post-earnings call that the component supply situation remained constrained even as the rising chip prices were affecting the company’s operating income.

- HP, a leading global PC vendor, says the shortage will continue to affect its capability to meet the demand for its personal computers and printers till at least the end of this year.

- Lenovo chairman Yang Yuanqing says the shortage will last at least 3-4 quarters more. However, Yang feels his company has managed the situation well to benefit from the strong demand for its products.

- Tesla CEO Elon Musk says the prices of the company’s vehicles are increasing due to the challenges faced in procuring raw materials.

- TSMC has started construction for a chip factory in Arizona. TSMC CEO CC Wei says the project remains on track to start production in 2024 using the company’s 5-nanometer production technology.

- Japan has entered a tie-up with TSMC to develop chip technology in the country. Around 20 Japanese companies will work with the Taiwanese chip giant for the project.

- Honchos from South Korea’s biggest conglomerates have asked the country’s president to pardon jailed Samsung Electronics vice-chairman Jay Y Lee to safeguard South Korea’s lead in the chip industry amid global shortages.

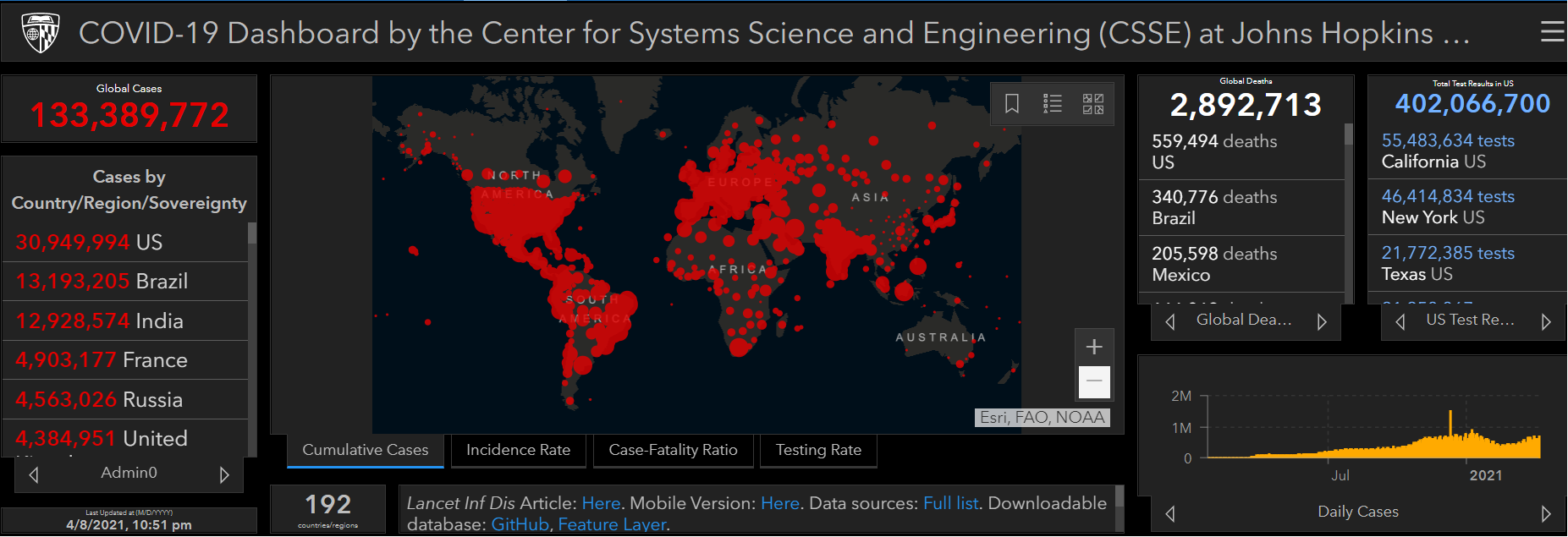

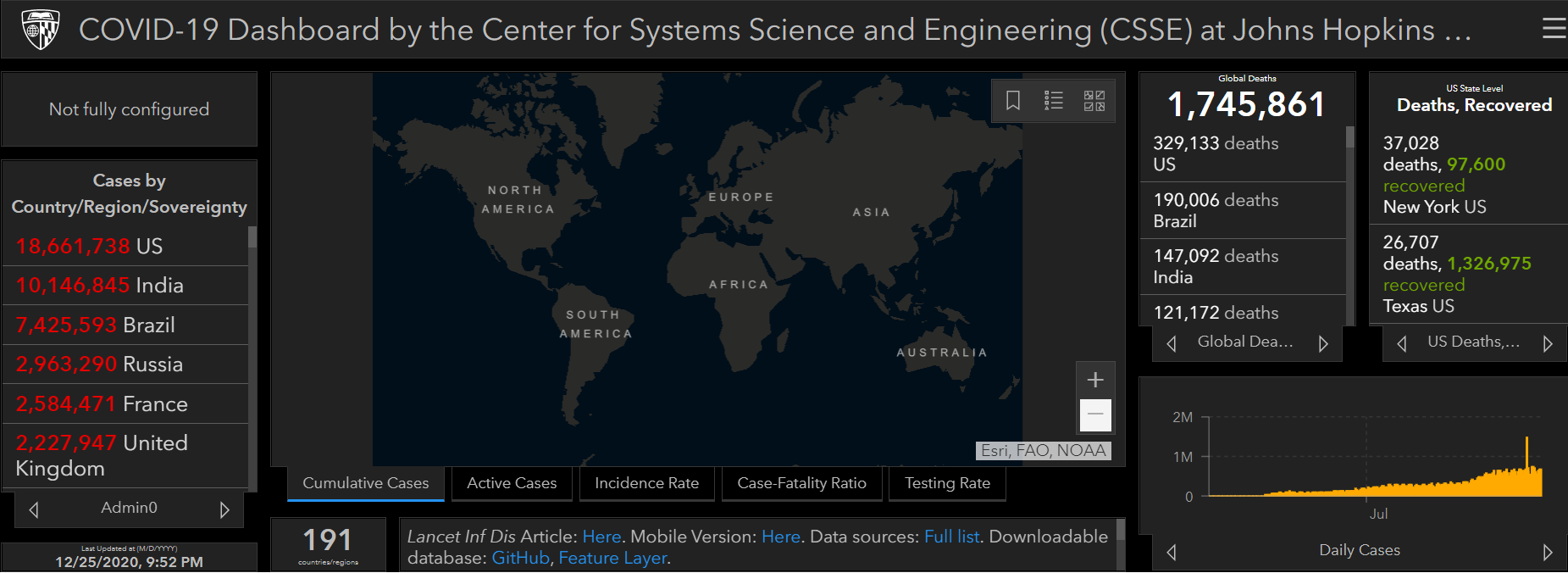

COVID-19 Week 74 Update

Counting the number of dead and infected due to COVID-19 has been a challenge ever since the pandemic started. According to the World Health Organization (WHO), the official numbers released by the governments the world over are a “significant undercount”. The UN agency’s estimates put the real number of deaths at 2-3 times higher than the reported figures. It calculates that the total number of deaths due to COVID-19 in 2020 was at least 3 million, compared to the 1.8 million reported officially. With the death toll going up more in Latin America and Asia now, it would be more about relying on estimates than the official numbers as the two continents largely lack proper reporting infrastructure. However, the WHO points out that even in the developed world, where the reporting systems are more reliable, undercounts are likely. For Europe, it puts the number of deaths in 2020 at almost double the 600,000 figure reported officially. Apart from the reporting infrastructure, the WHO says, people dying before getting tested for the virus are also responsible for some part of the variance between estimates and official numbers.

Nowhere is this difference between official and unofficial numbers more glaring than in India, which has recorded the highest official daily death toll for any country during the COVID-19 pandemic. According to the New York Times, even this record number is an undercount. After consulting more than a dozen experts, the newspaper has come out with three possible scenarios. As against the 26.9 million infections and 307,231 deaths announced officially till May 24, the newspaper’s “conservative scenario” puts the infections at 404.2 million and deaths at 600,000, while “a more likely scenario” puts the infections at 539.0 million and deaths at 1.6 million. “A worse scenario” puts the infections at 700.7 million and deaths at 4.2 million.

All these numbers point to the need for boosting efforts for vaccination. The International Monetary Fund (IMF) has proposed a $50-billion plan to end the pandemic by vaccinating at least 60% of the world’s population by the first half of 2022. The international financial institution estimates that doing so will inject around $9 trillion into the global economy by 2025 due to an early revival of economic activities. With rich nations likely to benefit more from this economic revival, there is a good incentive for them to be contributing towards this plan, feels IMF. Under the plan, the IMF is proposing widespread testing, lowering of restrictions on cross-border movement of vaccines and raw materials needed to manufacture them, donation of vaccines, upfront financing, investments to increase vaccine production, creation of sufficient infrastructure for vaccine deployment, and research into dose-stretching strategies.

COVID-19 Week 73 Update

The latest COVID-19 wave in India is showing signs of ebbing in the country’s urban areas, though not at the levels the government would like you to believe. On the other hand, the eastward movement of the wave continues, with some devastating scenes and figures which have only been recorded by the media to some extent. Lack of testing and shoddy data collection in these rural and backward areas ensure that we would never be able to understand the real scale of the pandemic there. Steps taken by different administrations to improve the situation have proven to be too little, too late.

To add to the woes, hospitals are reporting rising cases of black fungus, a disease that can lead to breathing problems, blurred vision, blackening of the nose, chest pain, blood in cough and even death if not treated in time. COVID-19 patients with comorbidities, particularly diabetes, and even doctors treating them are at risk here. Steroids used for treating COVID-19 can worsen diabetes in a patient.

Elsewhere, many East Asian countries are reporting daily records. Most of Thailand’s cases are coming from its prisons. Singapore has decided to shut its schools after finding that new variants, like the one found in India, are impacting more children than the previous strains. Indonesian authorities are anticipating a spurt in cases following celebrations marking the end of the holy month of Ramadan. In neighbouring Malaysia, a record 6,075 new cases were reported on Wednesday. In Vietnam, the fresh wave has resulted in temporary shutdowns in its industrial parks while Taiwan’s companies, including chip manufacturers, have announced measures to prevent the virus from affecting their employees. Japan has extended its third state of emergency till May 31 in Tokyo and other prefectures. Questions are being raised over the government’s decision to go ahead with the hosting of Olympics in July.

In Latin America, Brazil and Colombia are showing signs of plateauing of cases even as Argentina and Uruguay report doubling of daily cases. One distinguishing feature of the current wave in Latin America is that more young people are dying here compared to other regions.

COVID-19 Week 72 Update

If you thought COVID patients dying outside hospitals begging for oxygen and dead bodies lined up at crematoriums were the most horrifying scenes thrown up by the pandemic in India, then you are wrong. In scenes representative more of a different era from history, around 100 bodies were found floating on the river Ganges this week in two states in the country’s north. While the officials are yet to establish whether these bodies are of COVID victims, media reports talk of villagers immersing bodies of victims in the absence of wood needed for cremations. Even as India’s cities report a slight decrease in daily new cases, the countryside is facing the brunt of the second wave with poor healthcare infrastructure. This is also the area not properly covered by India’s much-criticized official COVID data.

According to the World Health Organization (WHO), India now accounts for 30% of COVID deaths globally. The UN agency has now declared the B.1.617 variant of COVID-19, first detected in India in October, as a “variant of global concern” following some studies indicating it spreads more easily than the original virus. There are three other variants in this category – first found in the UK, South Africa and Brazil. The WHO says the B.1.617 variant has been detected in as many as 44 countries so far. After India, the maximum number of cases of this variant have been found in the UK.

Even as India and other developing countries grapple with a huge vaccine shortage, a piece of disturbing news has come from Seychelles, a small island country in the Indian Ocean. Seychelles is the most vaccinated country in the world, with around 60% of the population having taken two doses of either Sinopharm or AstraZeneca vaccine. But last week, according to the country’s health ministry, more than one-third of those testing positive had both doses. The WHO maintains that vaccinations alone can’t stop transmission of the virus.

COVID-19 Week 71 Update

India continues to report record COVID numbers. On Thursday, the country reported record daily new cases of 412,262 and record daily deaths of 3,980. Even in Nepal, which shares a long porous border with India, record numbers are being reported (daily new cases 8,605 and daily deaths 58 on Wednesday). According to the International Federation of Red Cross and Red Crescent Societies, Nepal is recording 57 times more cases than this time last month, with the towns bordering India “unable to cope with the growing number of people needing medical treatment”. The Himalayan country was forced to suspend its vaccination programme last month in the absence of supplies from India and China.

In India, the second wave is now spreading eastwards, a region with poor health infrastructure compared to the rest of the country, even as other regions continue to report record numbers. Experts say the second wave will hit its peak around May 15. At the same time, a top government expert says a third wave is inevitable, and it will require modifications in the vaccines to make them effective.

On the vaccination front, the US has finally decided to back the demand for a global waiver on intellectual property rights for COVID-19 vaccines. India and other countries have been lobbying at the World Trade Organization (WTO) for the waiver. World Health Organization chief Tedros Adhanom Ghebreyesus described the US move as a “monumental moment in the fight against COVID-19”. However, it would take months before this move translates into action on the ground, as WTO decision-making is based on consensus between its 164 members. Besides, the pharmaceutical industry has expressed its unhappiness over the US decision, saying it would affect its response to the pandemic.

COVID-19 Week 70 Update

The COVID-19 situation in India has now completely spiralled out of control. The official data, which has been repeatedly slammed by experts for underreporting numbers, on Wednesday registered record daily new cases and deaths of 3,79,257 and 3,645 respectively. Total deaths crossed the 200,000 mark on Tuesday. According to the World Health Organization (WHO), India now accounts for 38% of the total cases recorded globally. The multilateral body’s calculations show that the B1617 variant (or the double mutant variant) of the virus detected in India has a higher growth rate compared to other variants found in the country. The double mutant variant has so far been detected in 17 countries, including India, US, UK and Singapore.

The global community has moved fast to send emergency aid to India. The US, UK, Russia and many other countries are sending hundreds of oxygen cylinders, oxygen concentrators, ventilators, masks and other medical equipment badly needed by India. Besides, the US has promised to send a part of its vaccine surplus to India, in addition to raw materials required to produce vaccines. It will take some time before we start seeing the impact of all this aid on the ground. Right now, it’s apocalypse written all over India’s cities and towns. Dead bodies are lining up outside crematoriums and graveyards that have run out of space. Public parks and parking lots are being taken over to accommodate the dead. The poor are begging for oxygen outside the hospitals while the rich are doing the same on social media.

The Indian government is in war mode to stem the tide but all efforts seem to be falling short. On Wednesday, when the registrations opened for vaccination for those aged 18-45, the government website meant for the purpose crashed. Many are questioning the government’s rationale in not imposing a lockdown. “At this point lives are so much more important than livelihoods,” tweeted Bhramar Mukherjee, noted epidemiologist from the University of Michigan.

COVID-19 Week 69 Update

India’s hospitals are currently witnessing the kind of apocalyptic scenes that were seen by the hospitals in the US, Italy and other countries last year. Staff, beds, medicines, oxygen, ventilators, all are in short supply even as crematoriums and graveyards work non-stop to tackle the surge in dead bodies reaching their doors. Official statistics for Wednesday put the daily new cases at 295,041 and daily deaths at 2,023, both being the highest ever. But as was the case in the first wave, in the current wave too the experts are sceptical about the official data. They are projecting an as much as ten-fold difference between the official and unofficial numbers for daily new cases and a three-fold difference for daily deaths. Media reports seem to tally with the expert assessments. They talk about crematoriums receiving many more bodies for COVID protocol funerals than those that left the local hospitals the same day. Witness accounts mention how the metal parts of crematorium furnaces have started melting with round-the-clock use, something which was not visible during the first wave.

The Indian government has announced some steps to tackle the fresh wave, while saying another national lockdown is not possible as it would disrupt economic activities. The governments of the affected states have announced partial lockdowns (usually for night hours). On the vaccination front, India has reduced the minimum age for vaccination from 45 to 18. Vaccine manufacturers have been allowed to sell a part of their production in the open market. But the question remains, where is the vaccine stock to meet these requirements? The country, which till some weeks ago was the world’s biggest vaccine exporter, is now grappling with a huge shortfall. The Serum Institute of India, which is the world’s largest vaccine maker and meets 90% of India’s COVID vaccine demand, produces around 65 million doses per month currently. But taking the current daily vaccination average of 3.5 million doses per day, India needs 105 million doses per month. Add to this around 600 million people in the 18-45 age bracket who will become eligible for vaccination on May 1. The government has announced funding for the vaccine manufacturers to expand capacity but that is expected to come not before July.

In extraordinary situations like these, governments the world over face allegations of being tardy in their response (a local court has slammed the Indian government for “not waking up to reality”). While such accusations are not totally unfounded, what is more important is to learn from these never-seen-before situations and avoid a repeat. The coming days will put to test the combined wisdom of the human race on this count, as a fresh and more virulent COVID wave looms in many more countries.

COVID-19 Week 68 Update

The world is now in the grip of a much stronger second wave of COVID-19 and fast approaching the peak of 845,412 daily new cases that was hit on January 8, 2021. India, followed by the US, Brazil, Turkey and France, is the biggest contributor here. On Wednesday, the South Asian country hit a fresh all-time peak of 199,569 daily new cases, with daily deaths also rising proportionately. While the US is showing a plateauing graph of daily new cases, Brazil is witnessing a fresh surge.

This second wave is being attributed to the various variants of the virus that are now in circulation globally, besides the people and governments dropping their guard. Not all of these variants can be tackled by the vaccines currently available. India, for instance, has reported a ‘double mutant’ variant (two mutations in the same virus) that has already resulted in a few cases of reinfection post-vaccination, according to local media reports. Similarly, an Israeli study has concluded that a South African variant can “break through” the Pfizer-BioNTech vaccine to some extent.

This is not to say that vaccination is entirely ineffective. What these examples highlight is the dead heat we find ourselves in. To find whether the virus(es) will beat all vaccination efforts or vice versa, we will have to probably wait till the yearend or early next year. An overwhelming majority has no hopes of getting vaccinated within the next six months, and these are the very people facing the brunt of all kinds of variants in circulation. The longer they remain unvaccinated, the higher the chances are of deadly variants reaching countries with high vaccination rates and reinfecting them.

Whenever pushed to drop profit motive for a humanitarian cause, companies globally are usually evasive. Therefore, it didn’t come as a surprise when the vaccine companies failed to positively respond to the appeals made to them last year by many NGOs and multilateral bodies to share their formulas with generic manufacturers. In a fresh move, more than 160 former heads of state and Nobel laureates, including Joseph Stiglitz, Gordon Brown and Francois Hollande, have asked US President Joe Biden to push for an intellectual property waiver for COVID-19 vaccines. Let us hope for the best.

COVID-19 Week 67 Update

India is headed towards a COVID crisis of gargantuan proportions. This week, the country crossed its peak of daily new cases that it hit in September during the first wave. Not only this, the second wave is showing a steeper climb. From 103,793 new cases on April 4 to 126,315 new cases on April 7, the number has risen by 21.7% in just four days. Experts are blaming the fresh spurt on people and politicians dropping their guard and participating in large gatherings. While the central government has so far not indicated imposing another lockdown, some state governments have imposed night curfews in affected cities, besides shutting malls and places of worship.

India, which is the world’s largest vaccine manufacturer, has so far administered 94 million doses, placing it behind the US and China. All Indian residents above the age of 45 are eligible for vaccination. In a meeting with state chief ministers on Thursday, Prime Minister Narendra Modi rejected calls for lowering this age, saying the poor and elderly need to be prioritized. Many states have complained of vaccine shortages. But India’s health minister maintains that there are sufficient shots. India has already reduced the exports of the AstraZeneca vaccine, which meets 90% of its demand, to cater to the domestic requirement. In addition to laying stress on testing, the prime minister called for a “vaccine festival” from April 11 to 14 to vaccinate as many people as possible.

Meanwhile, AstraZeneca’s tale of woe continues. The UK now wants those under 30 to avoid taking the vaccine in case an alternative is available, as evidence has emerged that it may cause a rare type of blood clot in the brain. This comes after many countries in Europe recommending such a minimum age. Australia, South Korea and the Philippines have also put the vaccine on restricted use while the African Union has dropped plans to buy it. The world, developing countries in particular, is banking heavily on this vaccine due to the scale of its production and ease of storage.

COVID-19 Week 66 Update

The pandemic-triggered semiconductor chip shortage has spurred action on different fronts even as short-term prospects worsen. While governments are focusing on augmenting domestic capacity, chipmakers are busy in firefighting (literally in one case) and planning for the long term, besides dealing with takeover overtures. Some key developments on the chip front from the week gone by:

- Japanese chipmaker Renesas Electronics, which controls around one-third of the global market for microcontroller chips used in automobiles, has said it would take at least 100 days to regain normalcy in production after a fire damaged 23 machines at its plant on March 19. Meanwhile, the Japanese government has asked Taiwanese companies to assist in alternative production.

- Samsung says the production at its chip plant in Texas, which remained affected for over a month due to bad weather on February 16, has now reached near-normal levels.

- TSMC says it will invest $100 billion over the next three years to increase production capacity at its chip plants. This move follows Intel’s recent announcement to invest $20 billion in expanding its advanced chip-making capacity.

- India’s government is offering more than $1 billion in cash to each semiconductor company that sets up production units in the country, according to a Reuters report.

- Hyundai has decided to suspend production at one of its plants in South Korea from April 7 to 14 following a shortage of chips.

- China’s Wise Road Capital and its partners have entered a $1.4-billion deal to acquire South Korea’s Magnachip Semiconductor Corp, a display and power chip maker.

- Micron Technology Inc and Western Digital Corp are in a potential race to buy Japanese semiconductor firm Kioxia Holdings Corp, the world’s second-biggest manufacturer of flash memory chips, says a Wall Street Journal report quoting sources. The deal could value the Bain Capital-controlled firm at around $30 billion, the report adds.

- US-based chip equipment manufacturer Applied Materials has announced that its $2.2-billion deal to acquire Japan’s Kokusai Electric Corp from KKR has been terminated in the absence of any positive indication on Chinese regulatory approval.

COVID-19 Week 65 Update

With the US, UK and some other countries showing a declining graph for daily new COVID-19 cases against the backdrop of increasing vaccination rates there, Brazil and India are now the new pandemic epicentres. A fresh wave of infections is spreading fast in the two countries, with Brazil reporting new peaks in daily cases and India’s cases touching five-month highs.

The surge in India has particularly alarmed the world. This is because India is also a vaccine manufacturing hub. In normal times, it caters to over 60% of the vaccine demand from developing countries. In the present pandemic, India has emerged as the biggest exporter of the AstraZeneca vaccine through a local firm, the Serum Institute of India (SII), which is also the world’s biggest vaccine maker.

However, following the emergence of the second wave, India decided to restrict the COVID vaccine exports, besides lowering the minimum age for vaccination from 60 and above earlier to 45 and above from April 1. While India is doing the right thing in prioritizing its population over other countries, what has compounded the situation is the country’s heavy reliance on the AstraZeneca vaccine, one of the only two vaccines cleared for use in the country.

India has committed to supply 200 million doses to low-income countries under the Covax programme of the Global Alliance for Vaccines and Immunisation (GAVI) and the World Health Organization (WHO). SII has a manufacturing capacity of around 60 million doses per month. GAVI says Covax has already notified participating countries that deliveries from SII will be delayed in March and April.

COVID-19 has brought to the fore weaknesses in global supply chains, from vaccines to semiconductors. Time for governments, multilateral bodies and businesses to get their act together.

COVID-19 Week 64 Update

Among the top 10 countries which reported the highest number of daily new COVID-19 cases on Wednesday, as many as six were from Europe. With the continent in the grip of a third wave of the virus, the less-than-projected supplies of various COVID-19 vaccines have triggered a blame game among the region’s countries. The European Union (EU) has threatened to ban exports of the vaccines to the UK over delay in deliveries of the AstraZeneca vaccine from there. The bloc says it is now thinking of linking the exports to the level of vaccination in a country, an allusion to the UK where more than 40 doses per 100 people have been administered so far compared to less than 20 per 100 in the remaining continent. The UK was quick to react, accusing the EU of brinkmanship and asking it to issue an explanation on its earlier assurances that already contracted exports would not be stopped. Further, on Thursday, the UK health secretary said the country would face vaccine shortages this month due to cuts from the Serum Institute of India, an AstraZeneca partner.

What has made the situation messy is some European countries’ decision to suspend the use of the AstraZeneca vaccine following cases of blood clot formation in the head of around three dozen recipients of the vaccine. The EU drug regulator says the vaccine is safe to use while the UK regulator says the incidence of blood clot formation was not more than what would have occurred naturally. Other countries, including Canada and India, too have announced to continue to use the vaccine. The World Health Organization (WHO), which cleared the AstraZeneca vaccine for emergency use last month, says the benefits of the vaccine far outweigh its risks.

COVID-19 Week 63 Update

Entering the second year of the COVID-19 pandemic, the virus continues to enjoy the upper hand in its battle with all efforts meant to contain it. More than our failure in quickly coming out with an effective vaccine or medicine, it is our failure to coordinate efforts towards a common goal that has hit the fight against the virus the most. According to Bloomberg, more than 334 million vaccine doses had been administered till Friday across 121 countries. The number is indeed impressive but what it fails to convey is the lopsided nature of the biggest vaccination programme ever. On one end of the scale are the developed countries from Europe and North America which have used their economic and political influence to procure vaccine supplies, including from plants located in developing countries. On the other end are countries from regions like Africa which have only the World Health Organization’s (WHO’s) sluggish vaccine distribution to look forward to. The following events from this week show all is not well on the vaccination front:

- Europe is a divided house on AstraZeneca’s vaccine. While as many as nine countries have suspended its use following safety concerns, countries including France and Germany have ignored these concerns. A WHO panel is looking into the matter but the global body says “there is no reason not to use it”.

- In another negative news on the AstraZeneca vaccine, the company has cut its target for supplies to the European Union to around 30 million doses in the first quarter, a third of its contractual obligations, according to a Reuters report. However, there is hope from Johnson & Johnson whose single-dose vaccine was cleared by the EU on Thursday.

- According to a report in the New York Times, the US is sitting on tens of millions of vaccine doses from AstraZeneca even as many countries are desperately looking for supplies. These doses can’t be used in the US as they are still awaiting the clinical trial results. Trials conducted in many other countries have already cleared the vaccine.

- Over 40 African charities blasted rich nations on Thursday for refusing to waive patents for COVID-19 vaccines, which would have helped bring down vaccine prices along with increasing their availability. This will only prolong the pandemic in poor nations, the charities said.

- Unicef has asked countries for around $1 billion more to fund poor nations’ vaccination drives.

COVID-19 Week 62 Update

Many countries have been reporting a spurt in daily new COVID-19 cases for the past week or so. Experts are attributing this rise to new strains of the virus and the authorities and people becoming lax in following precautionary measures. In the US, President Joe Biden has come down heavily on some states’ move to end compulsory wearing of masks, describing such decisions as “Neanderthal thinking”. The World Health Organization (WHO) is alarmed too. “This virus will rebound if we let it,” warned WHO expert Maria Van Kerkhove at a briefing. In fact, the WHO projects that many countries in Europe will see a resurgence in cases in the coming days.

When the vaccines first came last year, the predominant view, including among experts, was that these will be effective in containing the virus spread. But since then, new variants of COVID-19 have cropped up which are not only resistant to the vaccines developed so far but can also evade the immunity developed by already infected people. As a result, experts have revised their forecast and are now talking about COVID-19’s impact lasting for “years to come”. This is not to say that the vaccines are completely ineffective. Experts acknowledge that even with the new variants, the current vaccines seem to prevent deaths and hospitalizations. Besides, companies will come out with updated vaccines to fight the new variants.

It is, therefore, important that the vaccination drive is stepped up, especially in the developing countries, which have been lagging so far. A part of the problem, as the WHO has been pointing out, is the hoarding of vaccine doses by rich nations. COVAX, the WHO-supported programme to provide vaccines to poor countries, is already feeling the heat from countries getting into bilateral deals with vaccine companies. The programme, which aims to send 237 million doses of the AstraZeneca vaccine to 142 countries by May-end, has seen a slow start, with Ghana and Ivory Coast becoming its first beneficiaries last week. “We can’t beat COVID without vaccine equity. Our world will not recover fast enough without vaccine equity, this is clear,” WHO Director-General Tedros Adhanom Ghebreyesus told a briefing.

COVID-19 Week 61 Update

There is no sign of any let-up in the Covid-triggered semiconductor shortage being faced by the automotive sector since last year. The US sanctions against China’s chip factories and just-in-time supply schedule of a typical automobile factory have only added to the problem. Chipmakers too are focused on meeting the spurt in demand from consumer electronics firms, which buy high-end and high-margin chips. As a result, auto companies are lobbying their respective governments to promote creation of chip manufacturing facilities at the domestic level. On the other hand, some governments have approached Taiwan to resolve the crisis. Some key developments on the chip shortage front this week:

- US President Joe Biden on Wednesday announced a $37-billion plan to push chip manufacturing in the country. The US chip industry and auto manufacturers have been asking the government to take action on this front. Biden has also signed an executive order kicking off a review of supply chains for semiconductor chips, large electric vehicle batteries, pharmaceuticals and rare earth minerals.

- Tesla has reportedly halted the production of the Model 3 at its California plant from February 22 to March 7. Tesla said in January it expected a temporary impact from the chip shortage.

- Ford says it may have to cut its production by 20% in Q1 due to the shortage. General Motors says it has cut production at its plants in the US, Canada and Mexico.

- Japanese auto companies’ global production dropped around 4.5% in January from last year due to production cuts after the chip shortage.

- Renault said on Friday the chip shortage and other effects of COVID-19 could result in a volatile year for the French carmaker which reported a $9.7-billion loss for 2020.

- Infineon, the world’s leading supplier of chips to the automotive sector, is expanding its capacity to meet the demand in the long term. It is also planning to open a new chip plant in Austria this year. Currently, Infineon and other such specialist chipmakers outsource some of their production to contract manufacturers like Taiwan Semiconductor Manufacturing Co Ltd (TSMC).

- According to auto parts supplier Visteon, the chip shortage may bring down the global auto production in H1 2021 by 10% to 15%.

- Taiwan’s economy minister said on Saturday her country’s chipmakers were doing “what they should” to address the problem.

- Taiwan is facing a drought, pushing the island’s chipmakers to buy truckloads of water to ensure chip production continues.

- Foxconn chairman sees only “limited impact” from the chip shortage as most of the company’s customers “have proper precautionary planning”.

COVID-19 Week 60 Update

Even as COVID-19 cases show a steady decline globally, the Ebola virus has reared its head again in some African countries. Guinea and the Democratic Republic of Congo have reported fresh cases of the virus which saw its worst outbreak during 2013-2016 in West Africa and killed around 11,000 people. The World Health Organization (WHO) has asked six neighbouring countries to remain alert for a possible outbreak, while helping Guinea arrange 11,000 Ebola vaccine units. Compared to COVID-19, Ebola fares better in terms of vaccines and treatments, thanks to the lessons learnt in the previous outbreak.

All this brings us to the question which is becoming louder with the waning COVID-19 pandemic: How likely are we to see another pandemic of this size in coming years? Most experts say it is very likely. As we are already seeing in countries including the UK, South Africa and Brazil, a virus has a tendency to mutate into different variants, some of them more dangerous than the original. And the more the number of people it infects, the more the number of chances it gets to mutate. Each body a virus infects is a Petri dish for it to grow and change. Besides, a virus or its mutant can stay dormant for years.

So, what can the people and governments do to avoid, delay, or limit another pandemic? Reducing our interaction with nature by opting for sustainable habits is certainly in. The way we react to a pandemic at an international level is also important. Many of the problems faced in the current pandemic could have been easily avoided with a united global response. Already, the clamour for a global mechanism to deal with such a calamity is growing. UK prime minister Boris Johnson wants an international treaty on pandemics to ensure countries share the relevant data and also have an early warning system in place. European Council president Charles Michel has supported Johnson’s call.

COVID-19 Week 59 Update

The vaccine developed by AstraZeneca and the University of Oxford has been dogged by delays and uncertainties both before and after its release. In the latest instance, a study in South Africa says the vaccine has little impact on a COVID-19 variant spreading fast in the country. Following the study, the South African government announced suspension of the programme to roll out one million doses of the vaccine. However, later it said it was considering a “stepped” rollout of the vaccine to monitor its efficacy. In the meantime, it has decided to use the one-shot Johnson & Johnson vaccine.

Experts around the world, including from the World Health Organization (WHO), were quick to jump to the defence of the AstraZeneca-Oxford vaccine. They were unanimous that it was too early to dismiss the vaccine as being ineffective. Some experts even raised questions on the South African study, saying it was conducted on a small scale and after testing the vaccine at an interval of four weeks between the first and second doses, even as evidence suggested that the vaccine was more effective at a longer interval between the two doses. Britain, where the vaccine is being used extensively, pointed out that it was effective in fighting the COVID-19 variant there. France said the vaccine worked well with “nearly all the variants”. The WHO said benefits of the vaccine outweighed any risks and the shot could be taken by all, including by those aged 65 and above.

Among the vaccines approved for use by different governments and international bodies, the AstraZeneca-Oxford one is the most crucial internationally, thanks to the geographical spread of its trials and production. While the wealthier nations are relying more on Pfizer and Moderna vaccines, developing countries, in particular, are betting heavily on the AstraZeneca-Oxford vaccine’s success. The COVAX scheme of the WHO and the GAVI vaccine alliance, which aims to deliver 1.8 billion doses to 92 poor countries in 2021, is relying heavily on the AstraZeneca-Oxford vaccine to make the programme successful.

Any inability of the leading vaccines to tackle any COVID-19 variant would put a big question mark on the global recovery from the pandemic.

COVID-19 Week 58 Update

COVID-19 has brought windfall profits to technology companies, as we have been reporting here. But at the same time, the unexpected surge in demand for products and services related to work-from-home and study-from-home has stretched the global supply chains like never before. The shortage of semiconductor chips which was noticed last year has now spread to the automotive sector. The following developments from this week convey the enormity of the issues being faced by automobile companies on this score:

- General Motors has decided to cut production next week at four of its assembly plants in the US, South Korea and Mexico.

- Nissan Motor has been forced to partially suspend truck production at its Mississippi plant in the US.

- Volkswagen is considering entering direct contractual relationships with chip manufacturers, according to a Reuters report.

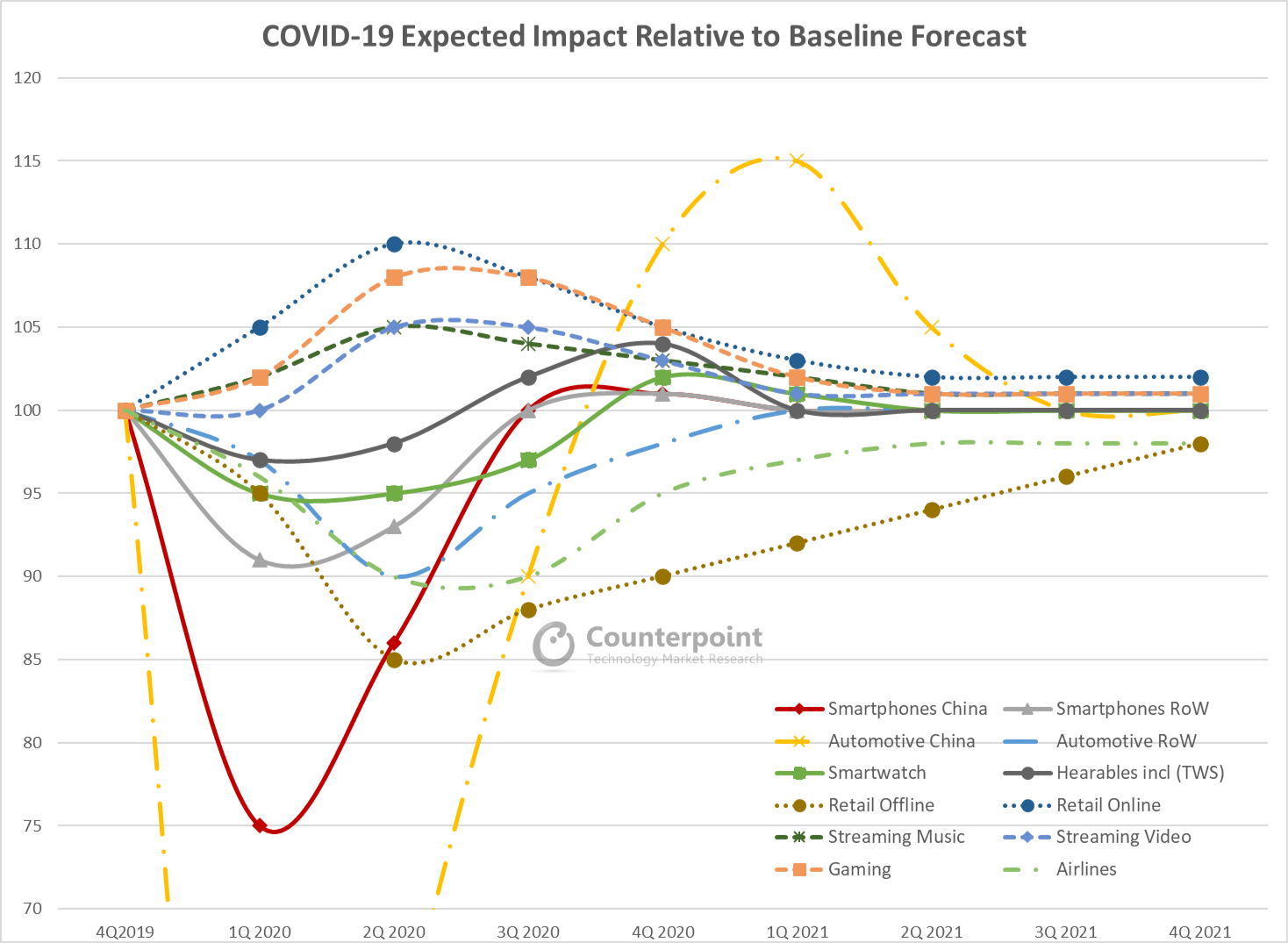

To be fair, besides the pandemic, there are other reasons contributing to this shortage, like under-investment in chip capacity over the recent years, geopolitical tensions and emergence of new products like electric vehicles. According to a Counterpoint analysis, this shortage is unlikely to end before H2 2021. However, the analysis predicts that beginning this year, leading foundries will enter a cycle of massive production capacity expansion that will continue till 2023. And far from triggering a glut, this expansion will still fall short of meeting the entire demand.

COVID-19 Week 57 Update

All the top 10 countries ranked by their total number of COVID-19 cases – US, India, Brazil, Russia, UK, France, Spain, Italy, Turkey and Germany – are now showing a declining graph in varying degrees when it comes to daily new cases. Globally, the total number of cases crossed the 100-million mark on Wednesday. Total deaths now stand at over 2 million. India’s government said on Thursday that out of its 718 districts, 146 had reported no new case during the last seven days. The government has decided to relax curbs on public swimming pools and cinema halls from February 1. Russia has also lifted a travel ban for India, Finland, Vietnam and Qatar that was announced last year.

Apple on Wednesday announced financial results for its fiscal 2021 Q1 ended December 26, 2020. Riding high on the new 5G-capable iPhone series, along with the pandemic-triggered demand for its laptops and tablets, the company posted a record revenue of $111.4 billion, up 21% YoY. International sales accounted for 64% of the quarter’s revenue, according to an Apple release. Research from Counterpoint’s Market Monitor service confirms this stellar show by Apple – for October-December 2020, Apple captured the top spot in global smartphone shipments, growing 8% YoY and 96% QoQ.

Microsoft on Tuesday reported a 17% increase in its revenue at $43.1 billion for the quarter ended December 31. Its revenue from Azure cloud computing service grew 50%. LinkedIn revenue increased 23% while Xbox content and services revenue increased 40%, according to a company release. Microsoft’s revenue from the productivity and business processes segment was $13.4 billion during the quarter and increased 13%. The mobile version of Teams has 60 million daily users now.

The pandemic has also popularized newsletters. Realizing their potential, Twitter has acquired an e-mail newsletter start-up, Revue, for an undisclosed sum to attract users who want to earn revenue from their followers. Twitter said it would bring down the paid newsletter fee to help authors retain more revenue from subscriptions.

COVID-19 Week 56 Update

After remaining below the global average for a major part of 2020, Africa’s COVID-19 death rate now stands at 2.5%, compared to 2.2% in the rest of the world. Africa Centres for Disease Control and Prevention director John Nkengasong says the second wave of the pandemic is more aggressive, with as many as 21 countries in the continent reporting a death rate above 3%.

Africa’s plight also brings into focus the efforts being made by multilateral bodies and countries for a timely delivery of vaccines to poor countries. Sadly, the pace here has been frustratingly slow. Under the COVAX scheme of the World Health Organization (WHO) and the GAVI vaccine alliance, 1.8 billion doses are targeted to be delivered to poor countries in 2021. But thanks to a shortage of funds, the scheme is yet to secure sufficient shots. According to GAVI, the 1.8 billion doses will be sufficient to cover 27% of the population in the 92 countries eligible under the scheme.

Some poor countries lack the regulatory infrastructure needed to clear vaccines for use and, therefore, rely on the WHO for clearances. The global body is planning to clear several vaccines for their rapid deployment in poor countries starting February.

The regime change in the US has come as a big relief in the efforts to combat the pandemic, not only in the country but also the world. On January 21, US’ chief medical adviser Anthony Fauci told the WHO that the US government under President Joe Biden was willing to join the COVAX scheme to help poor countries.

COVID-19 Week 55 Update

The COVID-19 situation will get worse before it gets better. With the vaccination drive seeing a slow start globally, many countries are coming in the grip of a fresh wave of infections. Sweden, which had been avoiding putting curbs on the movement of its citizens in contrast to other European countries, has now brought in tougher rules for social distancing at shopping complexes, private gatherings and gyms. The country will close businesses if the situation worsens.

China has registered its biggest jump in cases in over 10 months as infections surge in the Heilongjiang province. This comes just before a national holiday when millions of people usually travel. A paper by Chinese researchers published in the PLOS Neglected Tropical Diseases journal on Thursday said the number of people infected with COVID-19 in Wuhan could be three times the official figure. This conclusion was reached after analysing the blood samples of more than 60,000 people. Meanwhile, a World Health Organization (WHO)-led delegation arrived in Wuhan on Thursday to investigate the origins of COVID-19.

The Japanese government says it has detected a new variant of the virus in some travellers from Brazil. The variant has as many as 12 mutations.

The WHO hopes to launch COVID-19 vaccines in poor countries in February via its COVAX programme. It has asked countries to avoid striking bilateral deals with manufacturers so that poor countries can get access to the vaccines.

COVID-19 Week 54 Update

A fresh wave of the COVID-19 pandemic has gripped the world, whether due to a new strain of the virus or otherwise. In terms of daily new cases, the US (260,973 on Wednesday) is now followed by Brazil (62,532), UK (62,322), Germany (26,651) and France (25,379).

China on Thursday registered its biggest rise in daily cases in more than five months. The epicentre this time is Shijiazhuang, the capital of Hebei province, near Beijing. Over 200 cases have been confirmed in the city so far. Reports say the authorities are planning to test over 10 million people. On Wednesday, China said it was making arrangements for a visit by a World Health Organization (WHO) team looking into the origins of the virus. The statement came after the WHO expressed its concern over the delay in authorization for the visit.

Japan on Thursday declared a one-month emergency for Tokyo and three neighbouring prefectures after daily new cases hit a record in the capital. The government has avoided imposing wider restrictions due to their potential to cause economic hardships. According to Counterpoint’s Japan handset tracker, Japan’s smartphone sales plummeted 24% YoY in Q2 2020 but went up 10% YoY in the following quarter, supported by the government’s pro-economy stance in tackling the virus.

With the vaccine distribution campaigns still in their initial phases the world over, the fresh wave of infections will continue to inflict damage in the weeks to come. Stricter lockdowns like the latest one in the UK may have to be brought back.

COVID-19 Week 53 Update

There is no doubt the year 2020 will count among those which left an indelible mark on the course of history. Hardly any sphere of life has remained untouched from the COVID-19 pandemic. Many things have changed for the better and a few for the worse. Some of these changes will be permanent while others will depend on how early we are able to control the pandemic.

Climate change: Before the pandemic started, climate change was struggling to take prominence in human discourse. But COVID-19 has taught a valuable lesson — nature can quickly heal itself under the right conditions. With lockdowns in force globally, we saw pollution levels hitting multi-year lows and flora and fauna regaining some of the lost vitality. As soon as these lockdowns were lifted, we were back to square one. Expect policymakers to discuss effective mitigation of climate change more seriously in the coming year and beyond.

International cooperation: The pandemic has taught the world that global problems require global solutions. International cooperation was found wanting during the pandemic, whether in detection of the virus or development of vaccines. The post-pandemic world also requires a coordinated action on the economic and social fronts. Hopefully, the governments will get it right this time. There is an urgent need to give more teeth to multilateral institutions like the United Nations and World Health Organization.

Human behaviour: COVID-19 has imposed many restrictions on our normal behaviour, whether it is social distancing or wearing of masks. We have also “discovered” that work-from-home, study-from-home and shop-from-home are workable concepts.

Remote work: Before the pandemic, work-from-home as a concept was still taking baby steps. The CEOs were mostly sceptical about it. But COVID-19 has demonstrated that it is not only workable but also brings benefits to the employers in the form of cost savings on office maintenance. At the same time, it has also divided the employees among haves and have-nots. It is not possible for many to work from home as the nature of their work requires physical presence at the office.

E-commerce: Lockdowns meant no visits to markets and malls. As a result, e-commerce portals witnessed record traffic. Going forward, a big chunk of this increased traffic will become permanent. Same holds true for fintech.

Public transport: With the social distancing norms in force, public transport has taken a major hit. If the pandemic prolongs, there is a risk of people permanently shifting to personal vehicles and, therefore, increasing pollution and traffic congestion.

Real estate: With work-from-home taking roots, both residential and office property values in big cities will fall. Companies will opt for smaller offices while employees will prefer suburbs and small towns where property prices are lower.

COVID-19 Week 52 Update

Even as the COVID-19 vaccine distribution drive gathers steam in different parts of the world, a new ‘super-spreader’ strain of the virus has been detected in the UK. According to the country’s government, this new strain is up to 70% more infectious but there is no evidence to suggest that it is more deadly. Following the UK government’s statement, several countries stepped up testing of air passengers arriving from the UK and have already detected a few cases of the new strain.

A study by the Centre for Mathematical Modelling of Infectious Diseases, London School of Hygiene and Tropical Medicine, says the new strain is 56% more transmissible than other strains. “Nevertheless, the increase in transmissibility is likely to lead to a large increase in incidence, with COVID-19 hospitalisations and deaths projected to reach higher levels in 2021 than were observed in 2020, even if regional tiered restrictions implemented before December 19 are maintained,” the study adds. The authors of the study further warn that measures like the national lockdown imposed in England in November are unlikely to reduce infections unless schools and universities are also closed. “We project that large resurgences of the virus are likely to occur following easing of control measures. It may be necessary to greatly accelerate vaccine rollout to have an appreciable impact in suppressing the resulting disease burden,” the authors add.

From the COVID economy this week, Counterpoint expects that the global laptop market will hit a high in 2020, increasing 9% YoY to reach 173 million units. With uncertainty persisting over COVID-19, work-from-home and study-from-home will likely continue into 2021 and some part of 2022. Therefore, we expect the global laptop shipments to continue to grow slightly in 2021 and 2022. After reaching its peak in 2011, the laptop market growth had slowed down with the rise of alternatives such as smartphones and tablets.

COVID-19 Week 51 Update

With the developed countries beginning to roll out COVID-19 vaccines, the focus has now shifted to the developing countries and the challenges faced by them in procuring and distributing vaccines. Consider this: In the US, Pfizer’s vaccine costs $19.5 per dose while Moderna’s vaccine is expected to come at $37 per dose. In addition, these vaccines require procurement of special storage boxes. For a developing country, these costs are unaffordable, something which multilateral bodies are now discussing to find a way out.

The World Health Organization (WHO), in alliance with GAVI, plans to provide vaccines and diagnostic kits to economically weak countries through the Access to COVID-19 Tools (ACT) Accelerator fund. However, there is a big funding gap of $28 billion that needs to be filled. The WHO is now considering financial instruments like concessional loans and catastrophe bonds to meet the urgent demand. At the same time, the WHO says it is in talks with Pfizer to make its vaccine a part of the multilateral body’s global rollout and bring down the price to match the budgets of poor countries.

In the meantime, a Reuters report says, the European Union (EU) is considering donating 5% of the COVID-19 vaccines it has secured to poorer nations.

The Asian Development Bank (ADB) has launched a $9-billion facility to help countries fund purchase and distribution of COVID-19 vaccines.

The Inter-American Development Bank (IDB) says it will mobilize $1 billion to help the Latin American and Caribbean countries acquire and distribute COVID-19 vaccines. This is in addition to around $1.2 billion already committed in 2020.

Among countries, Canada has promised to spend $380 million on COVID-19 tests, treatments and vaccines in low- and middle-income countries through the United Nations International Children’s Emergency Fund (UNICEF).

COVID-19 Week 50 Update

As nations begin rolling out mass vaccination drives to fight the COVID-19 pandemic, fresh issues are cropping up, highlighting the challenges associated with administering a vaccine at such a large scale.

The UK started its mass vaccination drive on Tuesday, and soon the country’s Medicines and Healthcare Products Regulatory Agency was forced to issue an advisory that those having a history of anaphylaxis (an extreme allergic reaction) to some medicines or food should not get Pfizer’s COVID-19 vaccine.

In the US, highlighting the supply chain challenges being faced by the vaccination drive, Pfizer has slashed its COVID-19 vaccine production target for this year by half to 50 million doses. The decision was taken after some batches of the vaccine raw material failed to meet the standards.

Transportation of a COVID-19 vaccine like the one from Pfizer, which needs to be stored at minus 70 degrees Celsius, means having sufficient supplies of dry ice. But reports say officials in the rural areas of the US are not sure about the country’s dry ice production capacity to meet this spurt in demand. One can easily imagine the situation in a developing country with poor infrastructure.

Hackers, too, seem to be having a field day if Pfizer and its German partner BioNTech are to be believed. In a statement on Wednesday, the two companies claimed that documents related to their COVID-19 vaccine had been “unlawfully accessed” in a cyberattack on the European Medicines Agency, the EU body which assesses medicines and vaccines.

From the Covid economy this week, food delivery company DoorDash debuted at the NYSE on Wednesday with a gain of 80%, taking its value to around $71 billion.

COVID-19 Week 49 Update

Britain has become the first country in the West to approve a COVID-19 vaccine shot. Announcing the approval for Pfizer’s vaccine on Wednesday, the government described it as a ray of hope amid the surrounding gloom. It has already ordered doses for 20 million people against the country’s total population of around 67 million. Care home staff and residents will be the first ones to get the vaccine, followed by healthcare workers and the elderly. People will be contacted directly when their turn to get vaccinated comes. The main challenge with rolling out the vaccine is the requirement to keep it at around -80 degrees centigrade. This requirement will make it difficult to use the vaccine in countries with poor logistics infrastructure. Meanwhile, the UK government has also asked the country’s regulator to assess AstraZeneca’s vaccine for rollout, even as experts raise doubts over the trial data.

The World Health Organization (WHO) said on Wednesday it was reviewing the Pfizer vaccine trial data for “possible listing for emergency use” so that other nations could authorize the vaccine for national use. Pfizer has also approached the EU for a regulatory clearance, which is expected to come this month itself. However, the WHO believes that the world will not have sufficient quantities of vaccines in the next three to six months to prevent a surge in infections.

From the Covid-triggered economy this week, Salesforce is buying workplace messaging app Slack for $27.7 billion, betting on work-from-home outlasting the pandemic and the company getting into a better position to take on Microsoft. Slack has not been able to make the most of the opportunity presented by the pandemic.

COVID-19 Week 48 Update

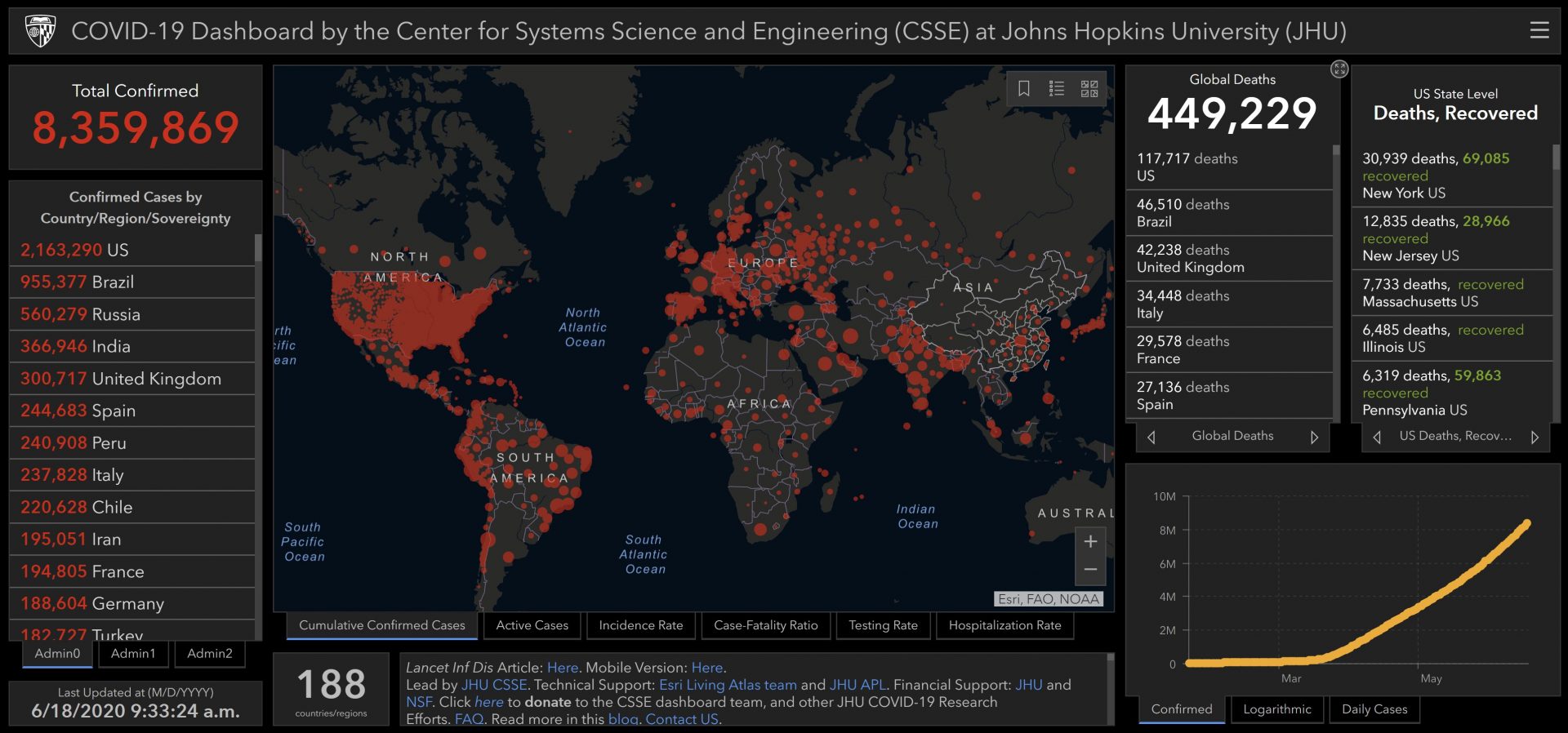

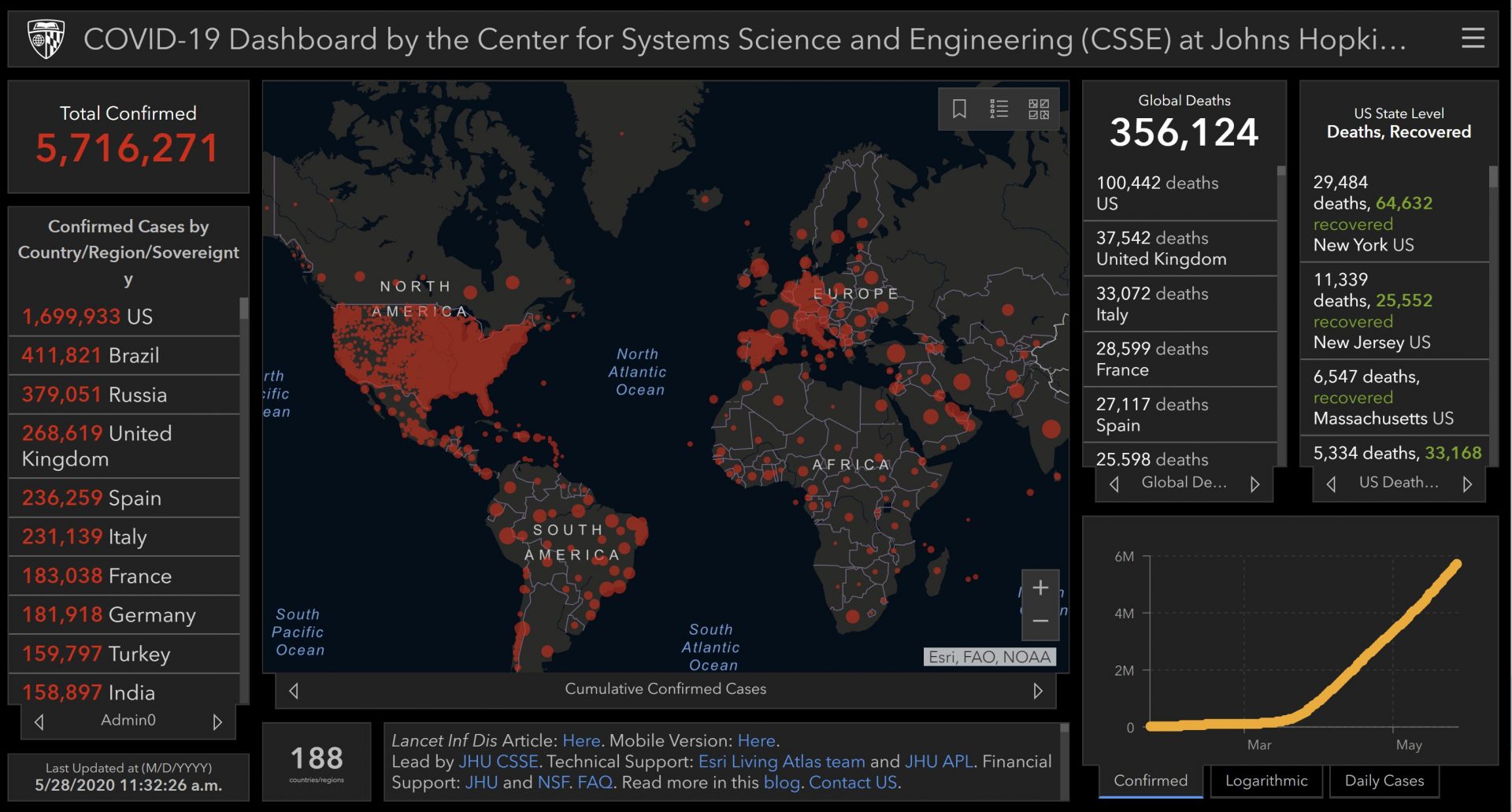

The total number of COVID-19 cases in the world crossed the 60 million mark on Wednesday with the US (13,138,204 cases), India (9,266,697) and Brazil (6,166,898) continuing to be the top three most affected countries. In terms of daily new cases, apart from these three countries, rest all in the global top 10 belong to Europe, with Italy (25,853 daily new cases), Russia (23,675) and Germany (20,825) taking the top three slots for the continent. When it comes to daily new deaths, the picture changes considerably. The US continues to top here with 2,304 deaths, but is followed by Mexico (813), Italy (722), UK (696) and Poland (674).

While the recent announcements by Pfizer, Moderna and AstraZeneca-Oxford on successful completion of their vaccine trials have raised hopes everywhere, it is the poor countries which run the risk of getting the vaccine horrendously late and thus suffering avoidable calamities. The World Health Organization (WHO) said on Monday that $4.3 billion more was needed for its global vaccine programme, which has raised $5 billion so far.

Dell continues to benefit from work-from-home and study-from-home with the soaring demand for its PCs and laptops giving the company a surprise 3% rise in Q3 revenue. Dell says it has not seen for over a decade the kind of demand it is seeing for its notebooks now.

Another sector that is emerging due to the pandemic is telemedicine. The sector is seeing an intense merger and acquisition activity, the latest being the merger of UpHealth Holdings Inc, Cloudbreak Health LLC and GigCapital2 Inc to create a $1.35-billion digital healthcare company.

COVID-19 Week 47 Update

The race for a COVID-19 vaccine is set to touch the finish line next month with the first batch of recipients getting the dose in December itself, thanks to the vaccine frontrunners starting production of their candidates before receiving the final approval.

Moderna announced on Monday that its vaccine candidate had been found to be 94.5% effective in preventing COVID-19 in a late-stage trial. Similarly, Pfizer said on Wednesday its candidate had been found to be 95% effective. The World Health Organization (WHO) demands at least 70% efficacy while the US Food and Drug Administration (USFDA) requires at least 50%.

If both Pfizer and Moderna get the emergency use authorization (EUA) from the US government, they will be in a position to supply around 60 million doses in the country in December this year. According to officials, US states are ready for the distribution at a 24-hour notice.

In a related development, USFDA said on Tuesday it had approved a COVID-19 self-testing kit that would provide the result within 30 minutes. The kit, produced by Lucira Health, has received the EUA for use by those aged 14 and above.

However, internationally, it is the vaccine candidate being developed by the University of Oxford and AstraZeneca that is inviting more attention due to its size and geographic spread. Here too, AstraZeneca says “billions of doses” of the candidate are already being produced with the late-stage trial data release expected by December.

The COVAX facility, set up by the WHO and the GAVI alliance, has managed to exceed the initial target of raising $2 billion to buy vaccine for poorer countries. The alliance said the collection would allow it to buy one billion doses for 92 countries.

COVID-19 Week 46 Update

With its rickety healthcare infrastructure and poor living conditions, Africa was being described as a COVID-19 disaster waiting to happen. But what has happened in reality is just the opposite. Even as the wealthier parts of the world grapple with their second or third waves of coronavirus, Africa has managed to retain the casualty numbers at the lowest levels among big continents. Against the World Health Organization’s (WHO’s) prediction in May that 190,000 people would die in the continent if measures to check the pandemic failed, in all 46,357 deaths had been reported till Wednesday. While experts have pointed out the low levels of testing in Africa as the likely cause of underreporting of deaths, reports from other quarters, including hospitals, have mentioned no unusual spurt in casualties.

There are many factors going in Africa’s favour here. The continent’s relative isolation means that many countries receive very few foreign visitors or send people abroad. A case in point is South Africa, which is among the African countries recording maximum interaction with the outside world, and also leads the table in total deaths related to COVID-19. Africa’s relative isolation also meant that the continent was hit by the virus late and countries got time to prepare themselves for the outbreak.

The other reason is the continent’s young population. According to the United Nations (UN), as much as three-quarters of Africa’s population is aged below 35. COVID-19 is known to have more adverse impact on older population and those with comorbidities.

The continent has also gone through other outbreaks like Ebola in the recent past to prepare for the current pandemic to some extent. Experts are also looking into whether a TB vaccine popular in the continent is helping impart immunity in this case also.

COVID-19 Week 45 Update

COVID-19 Week 45 Update

COVID-19 Week 45 Update

COVID-19 Week 45 UpdateEven as the world awaits the US presidential election result, the country on Thursday reported its highest ever daily new COVID-19 cases at 118,204. In Europe, Denmark has decided to cull around 17 million minks after discovering that a mutation of the coronavirus found in the animal had spread to humans. The country’s prime minister said this particular strain of the virus showed decreased sensitivity against antibodies, which could affect the efficacy of any future vaccine.

According to the latest research from Counterpoint’s Market Monitor Service, the global smartphone market grew 32% QoQ to reach 366 million units in Q3 2020. This recovery was driven by key markets like the US, India and Latin America returning slowly to normal due to eased lockdown conditions. The smartphone market has shown resilience to the ill effects of COVID-19 both from the supply and demand side. Samsung regained the top spot, shipping 79.8 million units to register 47% QoQ growth. This is the highest ever shipment by Samsung in the last three years.

PayPal continued to benefit from the surge in digital payments in Q3. However, the company, while beating estimates for Q3, forecast Q4 profit to be below expectations, mainly due to the uncertainty surrounding the pandemic and concerns over the US presidential election outcome. The US-based company processed $247-billion payments in Q3, an increase of 36% from the year-ago period, and added 15.2 million new active users.

Japan-based gaming company Nintendo has revised the forecast for its operating profit by 50% to $4.31 billion as it expects to sell 24 million Switch gaming consoles in the year ending March 2021, up from the previous forecast of 19 million.

COVID-19 Week 44 Update

With the second wave of COVID-19 strengthening its grip on Europe, Germany and France have ordered fresh lockdowns. Germany has decided to impose a month-long lockdown which will see closure of restaurants, theatres, pools and gyms from November 2. France has decided that from October 30, anyone leaving home will have to carry a document justifying the presence outside. On the other hand, the UK is resisting calls for imposing a nationwide lockdown, saying it brings economic hardships.

On the vaccine front, US’ top infectious diseases expert Anthony Fauci has said the country will get a vaccine only after January next year. Reports in the UK say the government there expects the results from the trials for Pfizer’s candidate would be available before those for AstraZeneca’s candidate, and that the Pfizer vaccine could be available for distribution before Christmas. An assessment by the European Union says the bloc will be able to administer a vaccine to all its inhabitants only by 2022 as the sufficient number of doses won’t be available till then.

From the COVID-triggered economy this week, Azure, Microsoft’s cloud computing business, has reported a 48% rise in its revenue for the latest quarter. Teams software continues to attract new users even as the demand for Windows for laptops and Xbox gaming services soars.

Sony has registered a record Q2 profit, convincing it to raise its outlook for the annual profit. The company’s gaming business continues to perform well before the launch of the PlayStation 5 (PS5) console next month.

Capgemini has reported an 18.4% increase in its Q3 revenue at $4.74 billion on good show by its digital and cloud offerings, which now bring more than half of the French company’s business.

COVID-19 Week 43 Update

Even as the total number of COVID-19 cases globally crossed the 41-million mark this week, with daily new cases hitting fresh peaks in Europe, the World Health Organization (WHO) came out with a study that said remdesivir, hydroxychloroquine, lopinavir and interferon were not effective in treating coronavirus. These are among the handful of drugs being used for the treatment. Interim trials by the WHO under its Solidarity Trial programme suggest these drugs are ineffective in reducing hospital stays and death risk. More than 11,000 adults with COVID-19 in around 30 countries participated in the trial. Reacting to the trial findings, Gilead, which produces remdesivir, said other studies had showed the efficacy of remdesivir. Besides, the US company said, there were differences in the way the WHO trial was conducted at different locations. Following the trial findings, the WHO announced that the Solidarity Trial would now cover monoclonal antibodies and other antiviral drugs.

On the vaccine front, Pfizer has said it could file for US authorization of its COVID-19 vaccine candidate in late November. This means there is a possibility of the company’s vaccine becoming available in the US this year itself. Pfizer is developing the vaccine with German partner BioNTech.

From the COVID economy this week, a World Economic Forum (WEF) study says that the pandemic has accelerated the shift towards automation in industries. Robots may end up destroying 85 million jobs over the next five years, the study warns.

Technology companies benefitting from work-from-home and study-from-home continue to report good numbers. US’ Verizon Communications beat third quarter profit estimates on Wednesday. Operating revenue fell 4.1% to $31.54 billion. Net income fell to $4.50 billion from $5.34 billion a year ago. The company has raised its adjusted EPS growth range guidance for 2020 from -2%–2% to 0%–2%.

Cyber security firm McAfee has raised $620 million in its US IPO. The IPO values the company at $8.6 billion. In 2016, TPG had bought a majority stake in McAfee from Intel in a deal that valued the company at $4.2 billion after including debt.

Taiwan Semiconductor Manufacturing Co (TSMC) has reported a record net profit of $4.8 billion in the July-September quarter, an increase of 36%. The company is betting big on the projected demand for the next two years. It has also raised its revenue forecast for 2020 from more than 20% increase to more than 30% jump now.

On the other hand, the boom triggered by the virus seems to be over for Netflix. On Tuesday, the company reported its weakest subscriber additions in four years, mainly due to lifting of pandemic restrictions during Q3. In the quarter, Netflix added 2.2 million paid subscribers, missing analysts’ and own forecasts.

COVID-19 Week 42 Update