- ADAS penetration in global car shipments will reach 78.7% by 2024 as new players help drive the ADAS chip market.

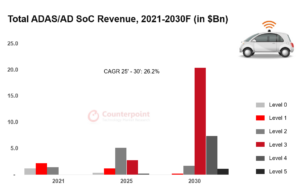

- Level 2 category will have a revenue market share of 44.4% in 2022 and 60% in 2024 due to higher safety criteria and lower component prices.

- The share of Level 4 SoCs in revenue will reach 24% in 2030. These SoCs will be used in luxury automobiles and robotaxis since they have a higher entrance barrier and cost more than Level 3 SoCs.

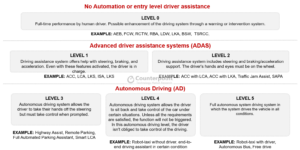

Semiconductors are becoming more important for automobiles as electrification and intelligence continue to advance. Among these, the level of intelligence has emerged as an essential factor that customers consider when buying a vehicle. The accuracy and efficiency of autonomous driving are determined by the computational capabilities and manufacturing process of the chip. Therefore, the increase in demand for autonomous driving is pushing the demand for advanced processes and will significantly increase the market size of advanced driver assistance systems (ADAS)/Autonomous driving (AD) chips. The computational capability of ADAS/AD processors must meet the requirements of the corresponding autonomous driving level. The Society of Automotive Engineers (SAE) defines the various levels of autonomous driving as follows:

The TOPS (trillion operations per second) of Level 2 ADAS/AD chips is typically between 10 and 100, but the TOPS of Level 3 is between 150 and 200 and the TOPS of Level 4/Level 5 is more than 400 and will reach 1000+. Each level is divided further based on functionality. Basic Level 2 features include only adaptive cruise control (ACC) and lane-keeping system (LKS), and can be achieved by an SoC with only 10 TOPS. However, advanced Level 2 may require up to 75 TOPS to achieve advanced ACC, which can maintain the lane center and pre-control the speed at upcoming curves.

The global ADAS/AD SoC market is expected to reach $30 billion by 2030 with a CAGR of 26.3% between 2022 and 2027. SoCs in the Level 2 category will have a revenue market share of 44.4% in 2022, which will reach a record high of 60% in 2024 due to an increase in safety requirements and a decrease in component prices. Level 3 AD systems will take a few years to gain the public’s trust, but by 2027, they will replace Level 2 as the standard. Compared to Level 3 SoCs, Level 4 SoCs have greater computational capability and bandwidth to process more high-resolution images and make a quick response. As a result, the entry barrier and cost of Level 4 SoCs are much higher than those of Level 3 SoCs, hence they will mostly be utilized in luxury vehicles and robotaxis.

The entry barrier to Level 1 and Level 2 ADAS SoC is low. Therefore, ADAS penetration can increase significantly when the cost of ADAS sensors, such as cameras and radars, continues to decline. Counterpoint expects that the global penetration of ADAS in car shipments will reach 78.7% by 2024. At the same time, multiple new players will enter the ADAS chip market. These startups are capable of AI chip design and mass production, and their solutions can swiftly fulfill localized requirements, such as local language and localization algorithms, at competitive prices. Therefore, emerging car OEMs will favor these new solutions. However, traditional automotive chips, such as Renesas and NXP, are also providing solutions. Level 3 employs more sensors and more efficient computing units than Level 2. The most significant difference between Level 3 and Level 4 is the improvement in artificial intelligence, as Level 4 autonomous vehicles must be able to take rapid decisions.

On the other hand, the development of autonomous driving (AD) chips is primarily driven by established consumer electronics giants such as NVIDIA and Intel (Mobileye). The R&D expenditures and entry barriers for AD chips are significantly greater than those for ADAS. In addition to the core AI chip, AD solutions should also incorporate connectivity, sensing systems, image training models, ADAS map development, route planning, vehicle control, driver monitoring systems (DMS), natural language processing (NLP) and intelligent cockpit solutions. Moreover, the AD chip must be able to deliver tailored and region-specific algorithms. This must be accomplished through the collaboration of automotive OEMs and AD chip companies. All of these factors make it challenging to create a good AD chip and the payback time is also lengthy.

Advantages, Disadvantages Faced by 3 Primary ADAS/AD Chip Vendors

In the past, there used to be a distinct division of labor between car OEMs, Tier 1 suppliers and chip vendors (Tier 2). The chip vendors might be either fabless firms or IDMs, and both would place orders to the foundry. Since the demand for semiconductors in the automotive industry was modest and all semiconductors used in automobiles were manufactured with mature processes, the foundry was less important. However, the performance and features in future automotive processors will play a crucial role in migrating to autonomous driving and electrification. Consequently, the ecosystem of collaboration between OEMs, Tier 1 suppliers and chip manufacturers is beginning to shift. Chip providers which were once Tier 2 are beginning to collaborate directly with OEMs. In addition, these three types of companies may engage directly with foundries to secure chip sources.

Competitor landscape

Mobileye is the leading Level 1 and 2 supplier due to its early entry. However, because of a lack of flexibility and superior alternatives, Chinese automakers want to replace Mobileye with NVIDIA or Horizon robots. Additionally, its solution has less computational power than those of its competitors. To keep up with other companies, Mobileye also introduced at CES 2022 its EyeQUltra, EyeQ6 Light and EyeQ6 High SoCs for L4, L2 and L1/L autonomous driving, respectively.

NVIDIA has aggressively entered the automobile autonomous driving market with its expertise in GPUs for the AI business. The benefits of NVIDIA’s AD processors include high computational power, extensive software tools and a complete environment allowing clients to create their own algorithms. In terms of clientele, NVIDIA works with the majority of automakers and Tier 1 suppliers worldwide. Atlan, the most recent AD chip from NVIDIA, has been released in 2022 with 1000 TOPS of computational capacity and is expected to enter mass production by 2025, aiming at L4/L5 autonomous driving solutions.

Qualcomm is a pioneer in smart cockpits but a follower in autonomous driving technology. Qualcomm’s Snapdragon Ride, a high-performance, low-power autonomous driving solution that supports L1-L5 degrees of autonomy, is aimed at the mid-to-high-end autonomous driving market.

Horizon Robotics, one of the few autonomous driving chip solution vendors in China, will likely supply to Chinese automakers in the coming years. Horizon has positioned itself as a competitor to Mobileye and NVIDIA. A new participant in the industry, it has introduced many products that correspond to Mobileye’s solution. In contrast to NVIDIA’s general-purpose processors, Horizon’s AD SoCs are ASICs, which consume less power and are more efficient than general-purpose CPUs. However, they are less flexible and may experience the same difficulty when moving to Level 3 and beyond.

Related Posts and Reports

- Global Automotive Semiconductor Forecast by the Level of Autonomy, 2021-2030F

- Global Autonomous Passenger Vehicle Market 2019-2030

- Automotive LiDAR Market Trend and Implications 2022

- Qualcomm in Driver’s Seat To Shape The Future of Mobility

- Connected Vehicle 2022 Summit: From ADAS to Autonomous Mobility, Here are Some Key Takeaways

- One in Two Cars Sold Will Have Electric Powertrain by 2030

- HERE Maintains the Location Platform Leadership, Ahead of Google, and TomTom in 2021