Intel enters a year where Moore’s law has considerably slowed, supply chains are constantly under pressure from various macro and micro factors, PC demand corrects from the pandemic induced highs and growth rally momentum comes from mostly Cloud, Automotive and 5G.

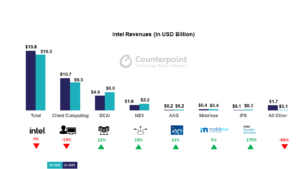

- Intel reported revenue of $18.4B, a decrease of 7% YoY, gross margin was down 4.8% YoY to 50.4%

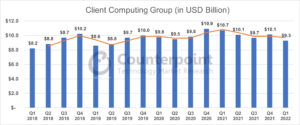

- Client Computing Group (Notebooks and Desktop) was down 13% with Notebook Revenue declining significantly by 14%

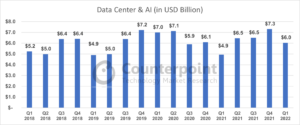

- Datacenter & AI Group remained the key growth segment for revenues for company with 22% YoY growth in revenues supported by Network and Edge Group with 23% YoY growth, Accelerated Computing & Systems with 21% YoY increase and Intel Foundry Services up by 175%

- Foundry capacity and Equipment to remain tightened till 2024

Segment Reports:

Client Computing: Consumer and Apple headwinds chip away $1.4B from the Client Group

The desktop revenues stood at $2.6B and notebook revenues were at $6.0B indicating a decline of 5% and 14% YoY respectively. The decline was majorly attributed to inventory digestion cycle and demand waning due to Covid-driven situations. Ramp down on Apple CPU and modem business in addition to muted demand from education market segment contributed to the significant decline in revenues.

The only offset came from increased ASP pricing across segments with 32% increase in Notebooks and 7% increase in Desktop segment.

- The Client computing group will see muted demand for the year because of the inflationary environment, supply chain constraints and inventory realignment by OEMs to reflect the intrinsic demand minus the Covid induced spike.

- Gaming and Enterprise Tech Refresh are the two trends that will help the group revenues to surf and stabilise.

- The product roadmap in later half of year will see intensive competition due to Raptor Lake and AMD Ryzen 7 hitting the markets.

Datacenter and AI (DCAI) proves to be The Revenue Guard for year 2022

DCAI revenue was up $1.1B or 22% at $6.0B due to continued demand from Hyperscalars and Enterprises. Hyperscalars are continuing to invest in DC infrastructures to enable their Metaverse ambitions whilst Enterprises are expanding and upgrading their infrastructure to sustain the data generation and providing analytics that is fast becoming a necessity from consumers.

Intel FPGA based IPUs also contributed to the growth where volume adoption is present at the major cloud players and the demand continues from peripheries including Networking and Automotive DCs.

A 3% ASP decrease was observed in segment and 26% volume increase due to product and customer mix indicating majority of sales from Intel Xeon Silver/Bronze.

We think that majority of sales went to enable the ‘Edge’ infrastructure.

- This is the year of Datacenters and Cloud as reinforced by every chip and cloud company in their revenue forecasts. The demand will be coming from Hyperscalars, and Enterprises expansion accelerated by the supercomputing efforts from the companies, SaaS adoption and cloudification of consumer services.

- Company’s Edge to Cloud chip portfolio offerings will help capturing the demand coming from the Edge and Networking market as 5G network deployments and MEC becomes more widespread

- With the acquisition of Granulate (SaaS service that improves performance in cloud costs with its autonomous dynamic optimization service to unmodified customer workloads) – the company’s SW stack combined with HW would provide additional revenue streams

Network and Edge (NEX) segment rolls due to the ’Edge’ Expansion

NEX revenue was $2.2B up 22% YoY. Demand drivers for the segment came from cloud networking hardware and software tools.

- The networking segment will strengthen as company has focused on launching silicon for software defined infrastructure – vRAN and ORAN for Network and Edge capturing the upcoming high-volume deployments from operators

- Upcoming Sapphire Rapids can prove to be a breakthrough for Intel to establish its leadership as it claims to deliver up to two times capacity gains for vRAN and support advanced capabilities like high-cell density for 64T64R Massive MIMO

Accelerated Computing Systems and Graphics (AXG) revenue is at $219M

Intel marked its foray into Discrete Graphics with its Intel A series of mobile GPU which was launched in Spring this year. The Desktop GPU are expected to be launched in Market this summer. Company is expecting to do $1B+ business this year as it scales the range at Data Centre level with Ponte Vecchio.

- Intel is entering highly competitive market where Nvidia reigns supreme. The company has launched only one Variant – Intel ARC for Mobile so far with 50+ design wins. The variant has performed well but it will take more time for Intel to get the mind share and the wallet share it is expecting! The other variants would be launching this summer and we sincerely hope that Intel promises on the momentum it has indicated for its AXG business.

- The launch of Blockchain accelerator would help in capturing the peripheral accelerator business which is dominated by mostly DIYs or Nvidia

- The resonance of synergies from having its own CPU+GPU+I/O and in-house foundry coupled with its proprietary SW technologies – Evo & XeSS would help Intel to produce inspiring performances from devices because of component efficiencies in the long run.

Mobileye logs record revenues at $394M

Mobileye grew 17% YoY to have its best quarter in earnings. The company has successfully demoed L4 robotaxi in Jerusalem and grew its number of testing sites to 10 cities across 3 continents with addition of Miami and Stuttgart. The commercial robotaxi services will commence at the end of 2022 in Munich and Tel Aviv.

- The much-awaited IPO might debut later this year but Intel has so far kept to its delivery and promise schedule regarding Mobileye products

- The revenue would probably see a considerable spike later this and early next year as the consumer and commercial L4 vehicles enter mass production

Intel Foundry Services (IFS) is on a promising start with $5B in deal value across nodes

The revenue of IFS was $283M. The team has 10 opportunities for its process and package offerings representing over $5B in deal value. The team has over 30 test chips for Intel 16 and is expecting Intel 3 and Intel 18a customer test chips to tape out later in 2022.

From foundry perspective the progress looks very optimistic considering on Intel 4, Meteor Lake has successfully booted and pre-production wafers have commenced on Intel 3.

The company also commented that it has enough substrate and Fab supply to meet customer’s demand.

- The behemoth task of delivering 5 nodes in 4 years remains the crucial aspect to Intel for its every business. So far it looks like everything is going good for them but as the tape-outs occur for Intel 7 we would have better visibility on the yields.

- Considering the past, we are cautiously optimistic on the outcome on the node delivery as the Wafer Equipment manufacturers have started flagging the delivery timelines.

ESG Commitment Updates: Intel announced initiatives to reduce its greenhouse gas emissions and develop more sustainable technology solutions by identifying greener chemicals, new abatement equipments, including using 100% renewable energy across their global operations by 2030 by investing $300M to achieve 4B KWh of energy savings and achieving net-zero greenhouse gas emissions in their global operations by 2040.

Outlook for Q2 2022

Company is expecting $18B for Q2 2022, a 3% decrease YoY as the inventory burns happen and the company readies itself for inventory reversals due to launch of Raptor Lake and Sapphire lake. But for Q2 the client computing will remain muted due to the macro factors heavily influencing consumer sentiments.